7 Reports

7.1

Plan Change 79 -

operative in part

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

28

May 2026

|

|

Report

Author:

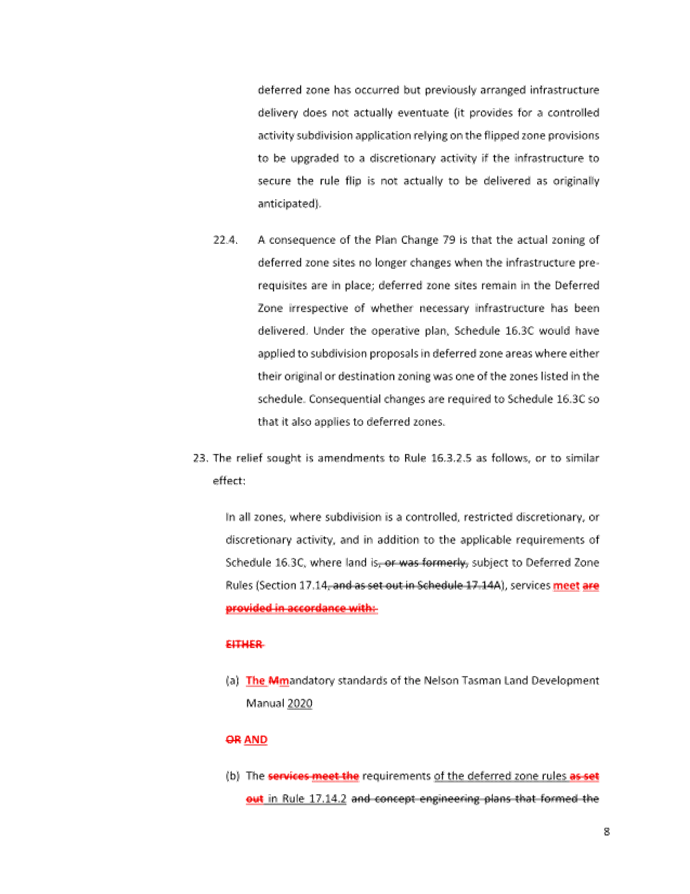

|

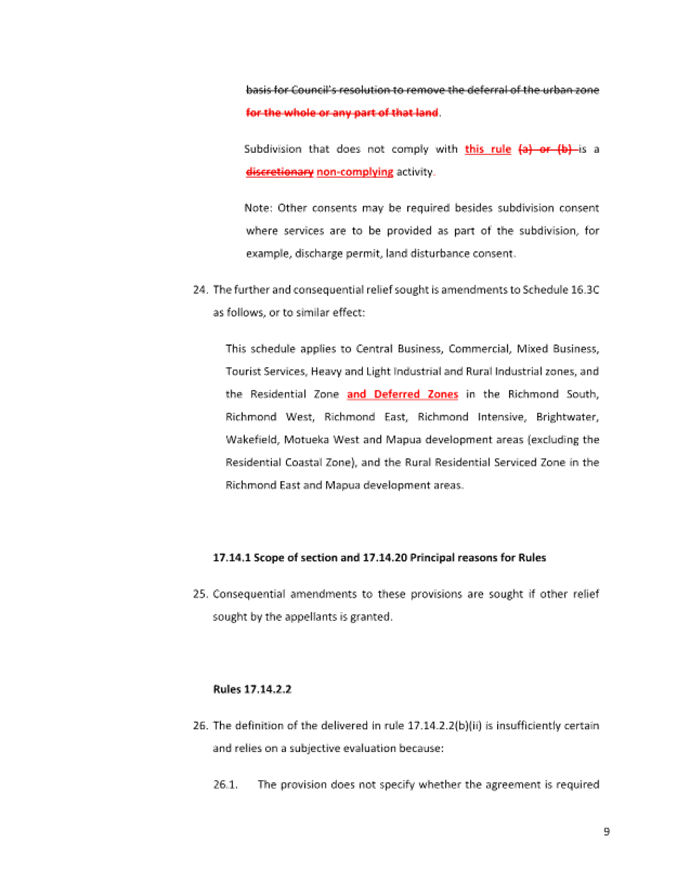

Jeremy

Butler, Team Leader - Urban and Rural Policy

|

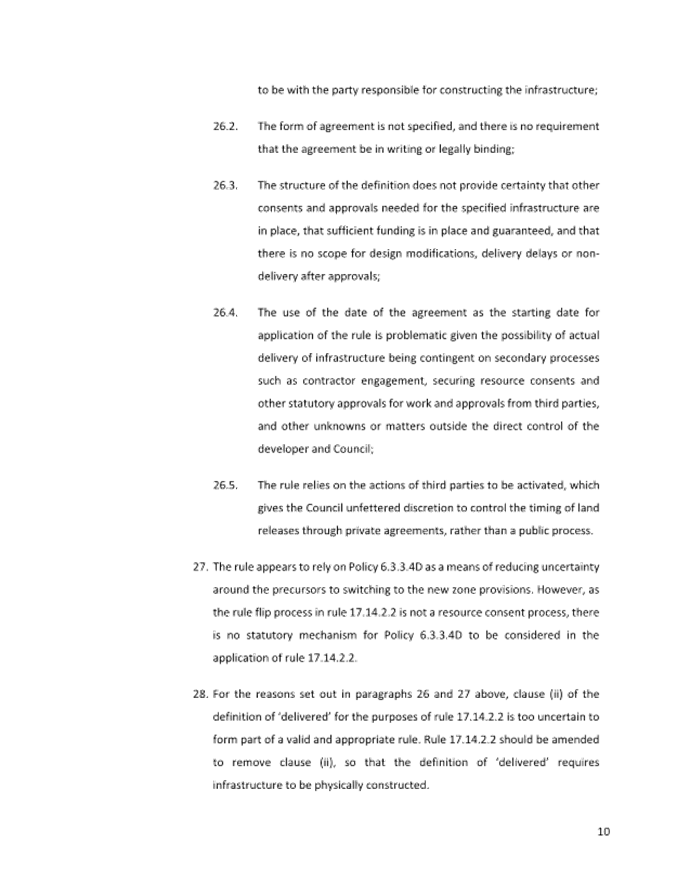

|

Report

Authorisers:

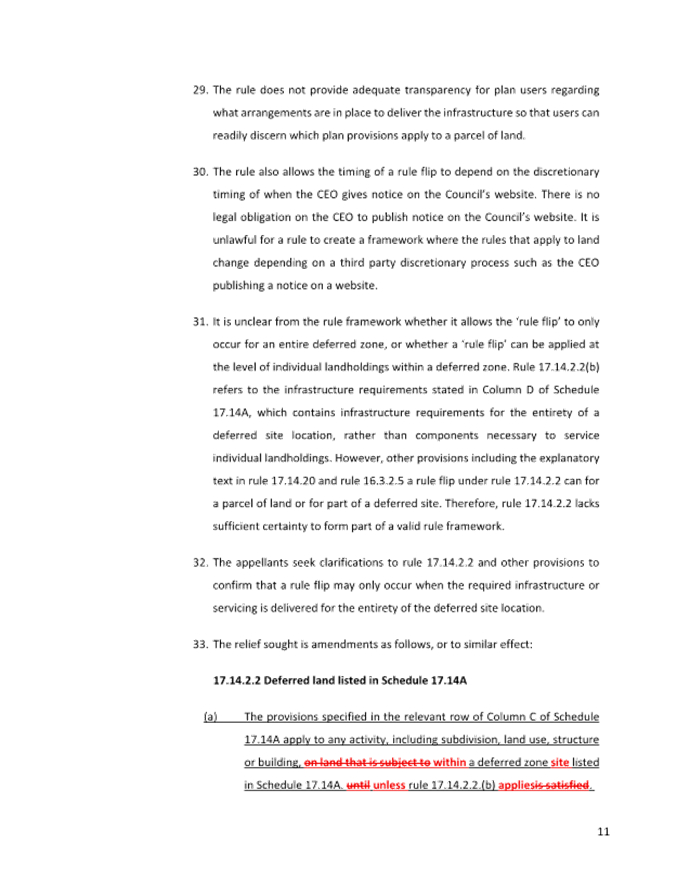

|

Barry

Johnson, Environmental Policy Manager

|

|

Report

Number:

|

RCN26-05-15

|

1. Purpose of the

Report / Te Take mō te Pūrongo

1.1 This report seeks that

Council approve Plan Change 79 in part, limited to those provisions that

are not subject to appeal, and to make that part of the plan change operative.

1.2 The report is procedural and

gives effect to Council’s existing decision in respect of zoning and

development‑enabling

provisions that have not been appealed, without prejudicing the Environment

Court’s consideration of the appeal.

2. Summary / Te

Tuhinga Whakarāpoto

2.1 Council adopted the

recommendation Plan Change 79 on 19 February 2026. An appeal

has since been lodged against specific provisions of the decision. The appeal

does not relate to all parts of the Plan Change. The zoning and development‑enabling

provisions proposed to be made operative are not subject to appeal and are

clearly severable from the matters before the Environment Court.

2.2 This report seeks Council

approval to make Plan Change 79 operative in part, limited to the

provisions that have not been appealed, in accordance with Cl 17(2) Schedule 1

of the RMA 1991.

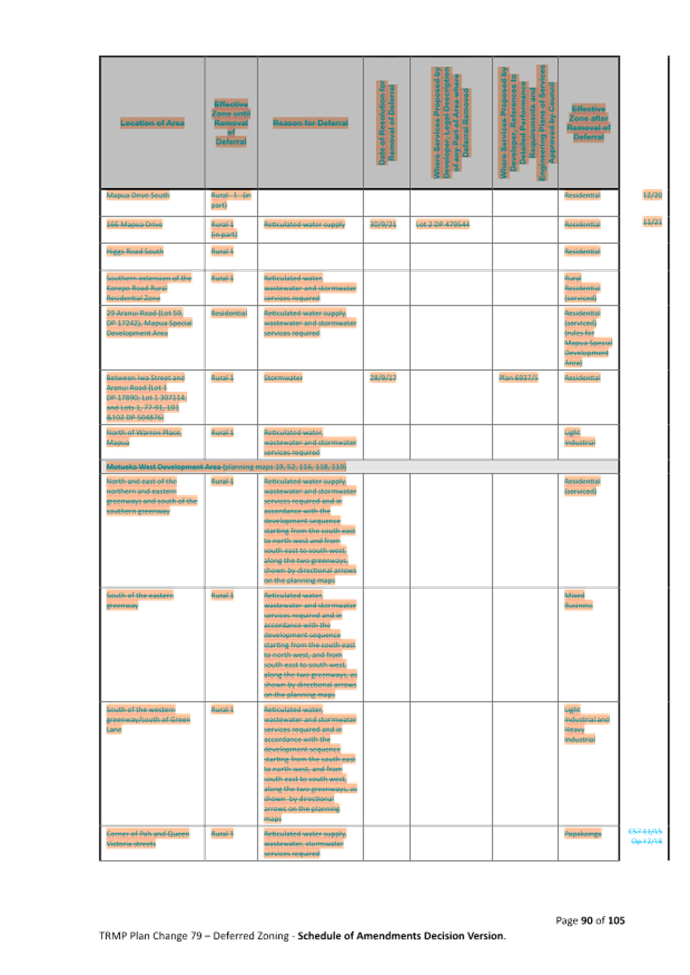

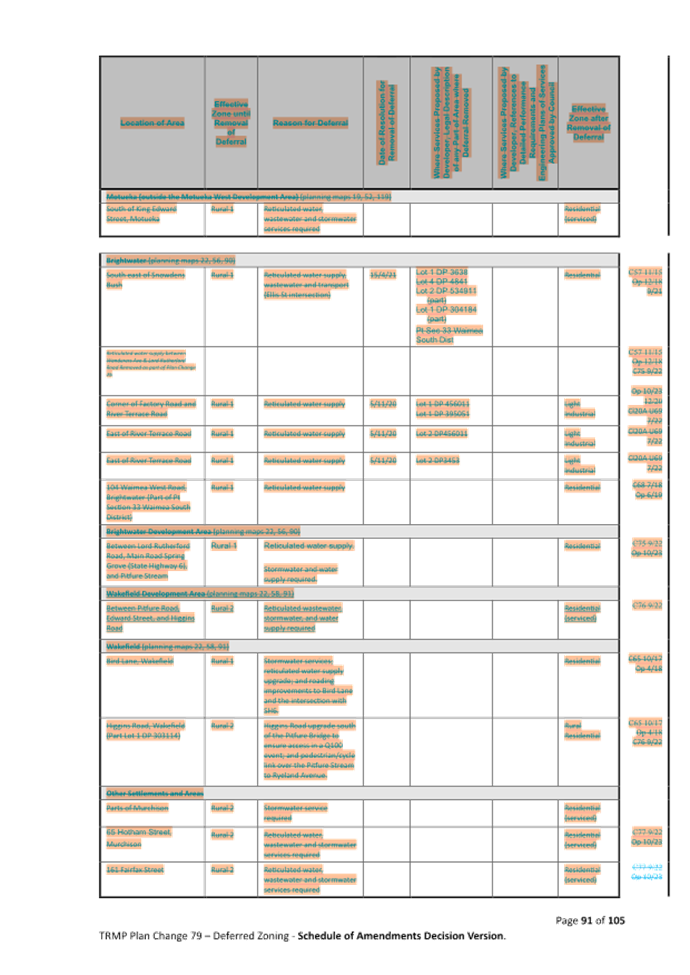

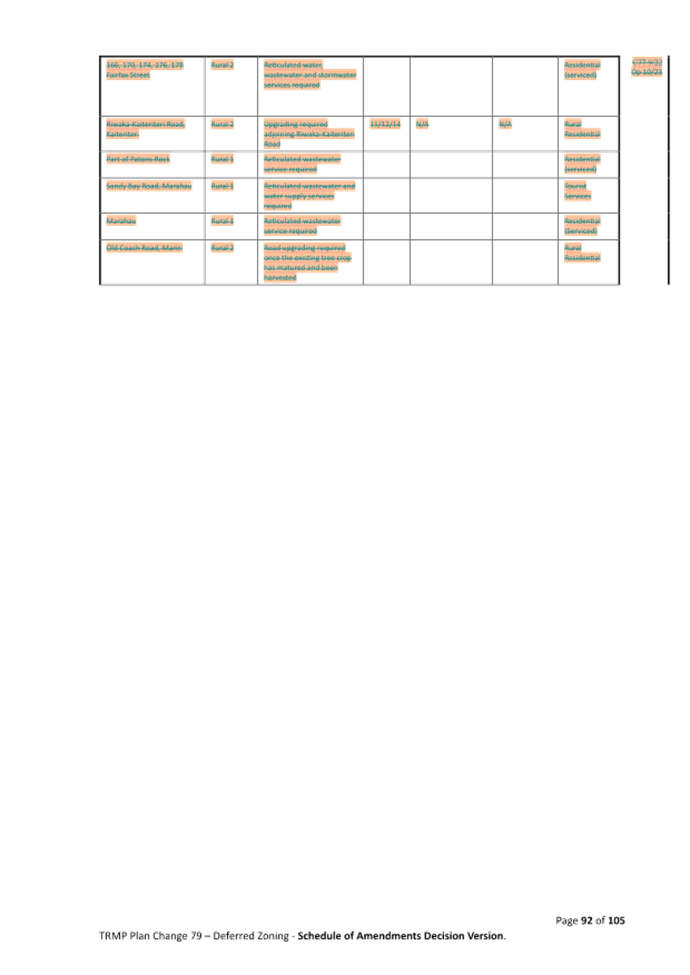

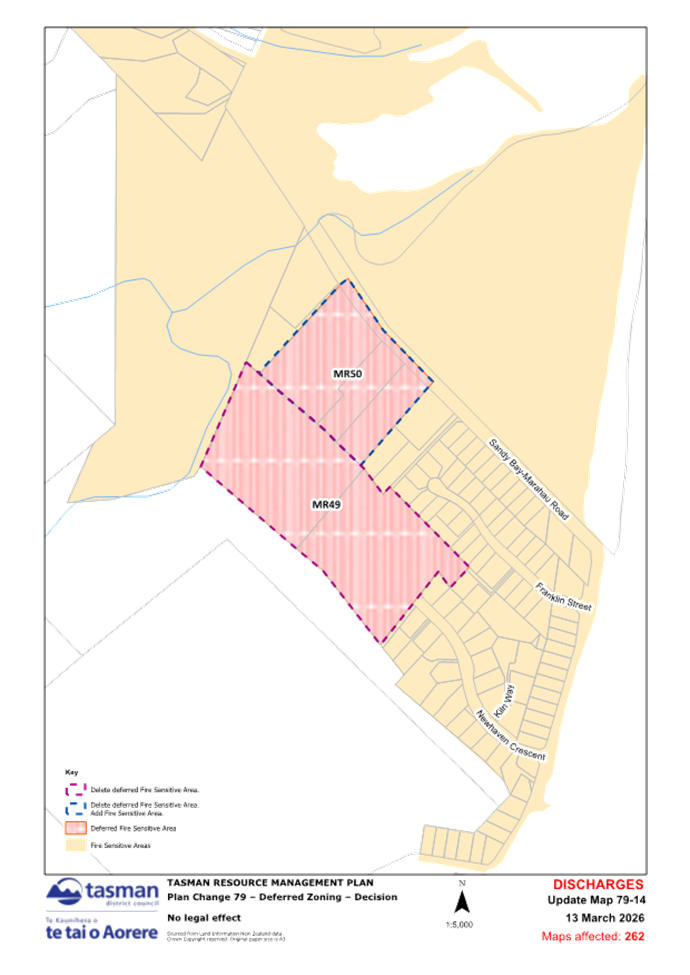

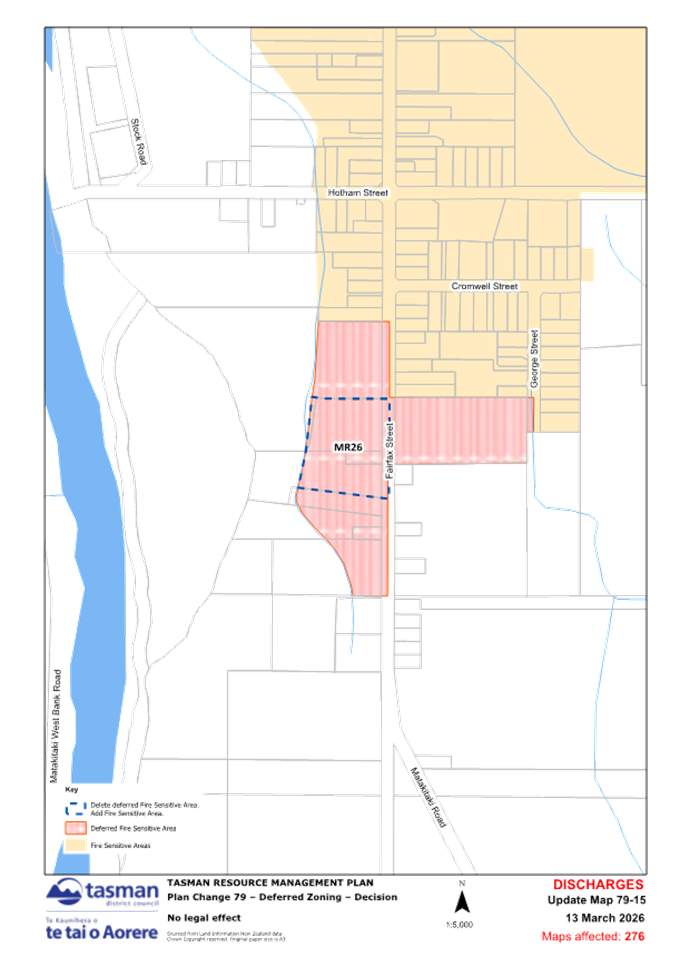

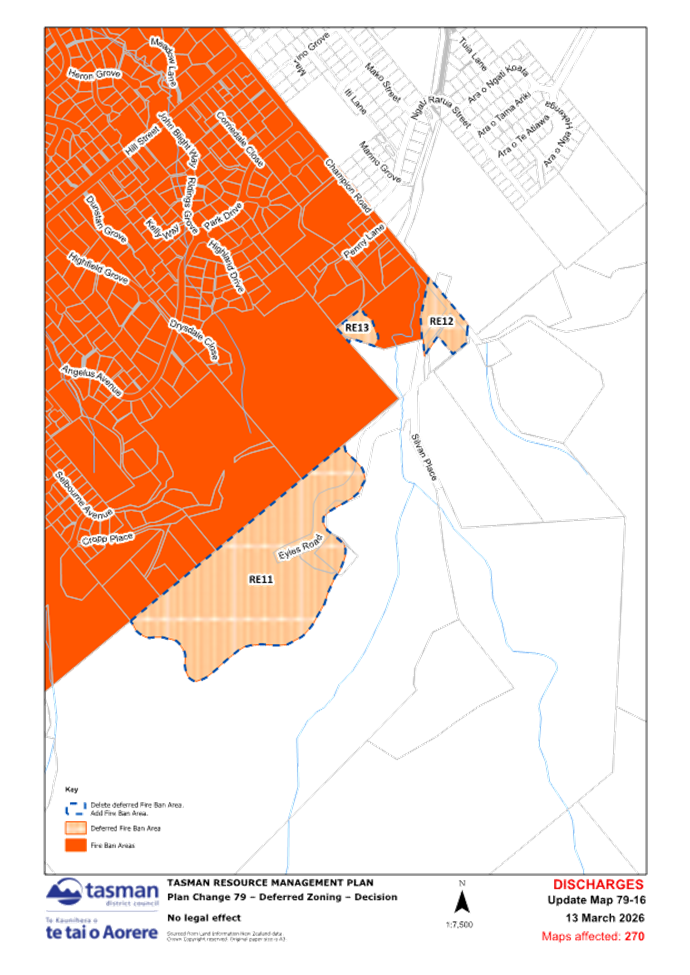

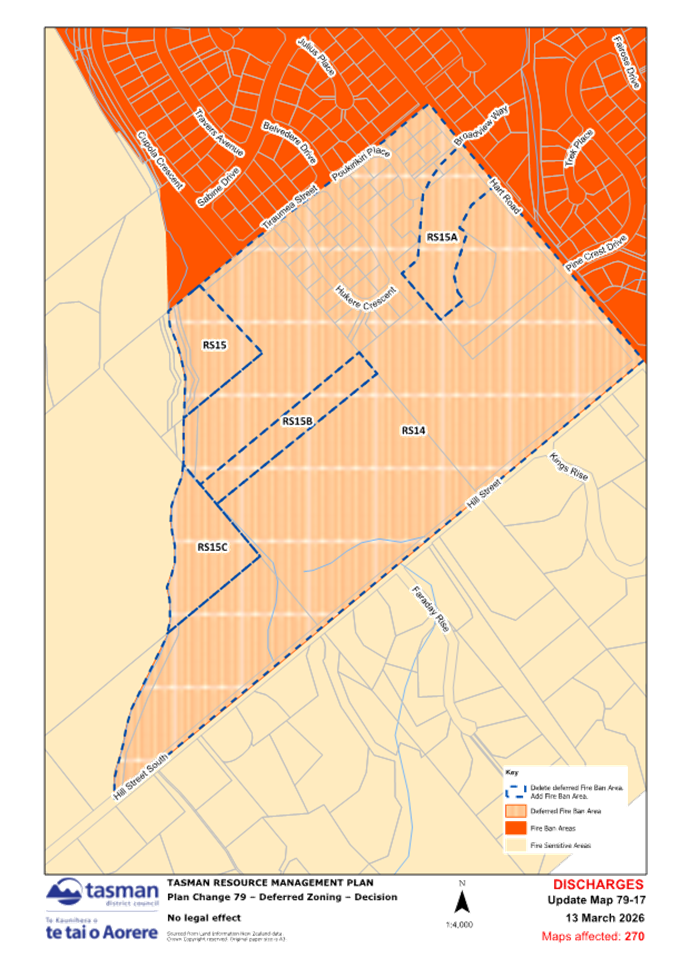

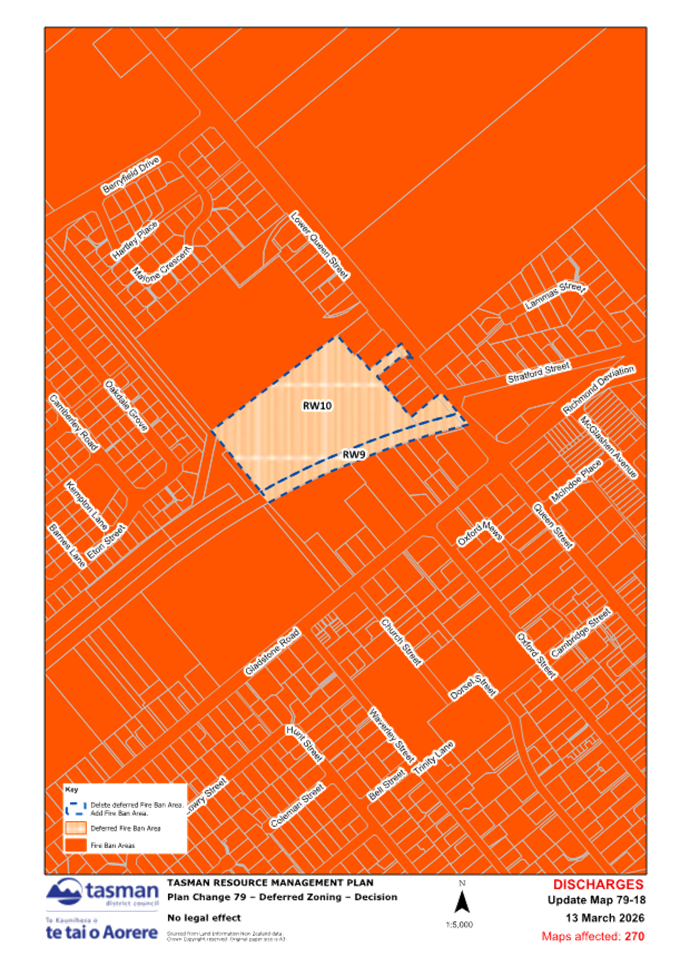

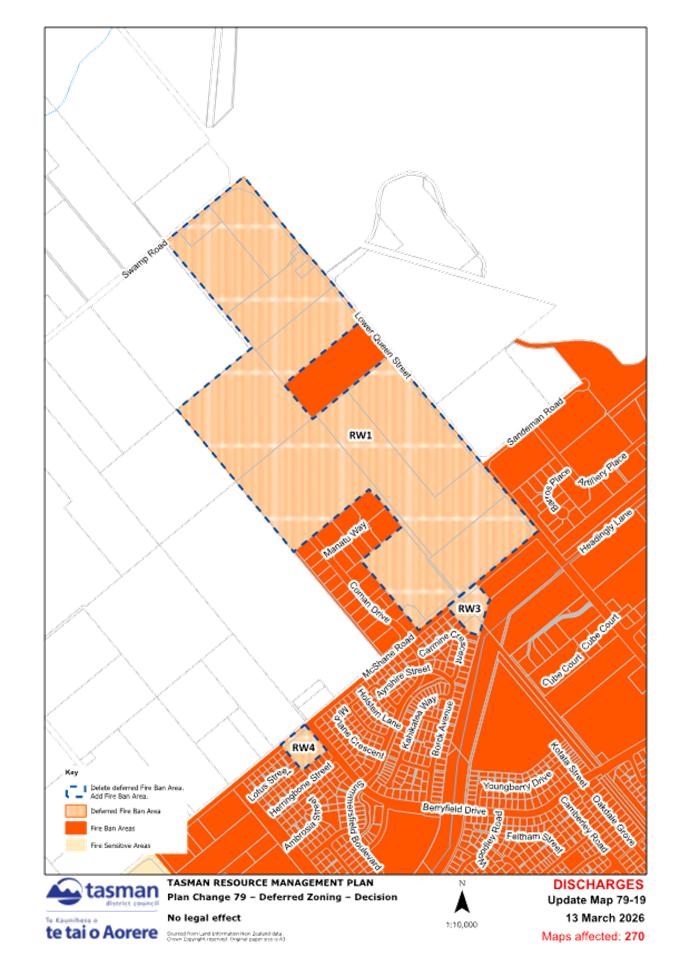

2.3 Attachment 1 shows

highlighted in orange all the amendments to

the TRMP which will NOT be approved and will not become operative. All

unhighlighted provisions in that document, as well as the zone, area and

discharge maps that formed part of the plan change, will be approved under this

resolution and will be made operative as soon as practicable.

2.4 All area, zone and discharge

maps are also attached and are to be approved and made operative.

3. Recommendation/s /

Ngā Tūtohunga

That the Tasman

District Council

1. Approves

Plan Change 79 – Deferred Zoning in part, being those parts of Plan

Change 79 that are not highlighted in orange in Attachment 1 to the agenda

report, and the zoning, area and discharge Decision maps. Also to recognise

that the provisions which are highlighted in orange in Attachment 1 are not

approved and remain subject to appeal; and

2. Approves

the affixing of the Tasman District Council seal to the approved provisions and

the public notification of their operative date.

4.1 Plan Change 79 –

Deferred Zoning (PC79) was publicly notified in November 2024 and progressed

through the Schedule 1 process under the Resource Management Act 1991. The

primary purpose of PC79 was to amend the Tasman Resource Management Plan (TRMP)

to introduce a revised and more robust deferred zone framework, and to give

effect to that framework by rezoning and managing a range of existing deferred

sites across the District.

4.2 In particular, PC79 sought

to:

· clarify how

deferred zones transition to their intended end‑use zones;

· link the release

of deferred land to clearly specified infrastructure requirements; and

· enable the

release, retention, or re‑zoning of existing deferred land where this was

considered appropriate following assessment through the plan change process.

4.3 Following notification, PC79

was the subject of submissions, further submissions, and a hearing before an

independent Hearing Panel. The Hearing Panel issued its recommendations to

Council, addressing the submissions received and recommending amendments to the

notified provisions.

4.4 On 19 February 2026, Council

considered the Hearing Panel’s recommendations and resolved to adopt

decisions on PC79. That decision accepted, accepted in part, or rejected

submissions and further submissions, and approved changes to the TRMP as set out

in the Council’s decision documentation and Schedule of Amendments.

4.5 The Council’s decision

on PC79 was released on 13 March 2026, in accordance with Schedule 1 of the

Resource Management Act. As a result, an appeal period commenced during which

appeals could be lodged with the Environment Court.

4.6 An appeal has since been

lodged against specific parts of the PC79 decision. The appeal does not

challenge the entirety of PC79. Instead, it is limited in scope to particular

objectives, policies and rules.

4.7 Under the Resource

Management Act, where a plan change decision is appealed in part, Council may

approve part, if all submissions or appeals relating to that part have been

disposed of; see cl 17 Schedule 1. While the drafting of cl 17 does not

explicitly address a situation where no appeal has been filed against certain

provisions (c.f. ‘disposed of’) the clause applies to these

circumstances because the submissions on those parts have been disposed of and

therefore Council may effectively treat them as unchallenged parts of PC79 and

approve them. The effect is that part of the plan change will become

operative, while preserving the Environment Court’s jurisdiction over the

appealed provisions.

4.8 This report addresses

whether, and to what extent, provisions of PC79 can be made operative at this

stage. It does not reconsider the merits of PC79 or the decisions made by

Council on 19 February 2026. Its purpose is solely to enable Council to make

those parts of the PC79 decision that are not under appeal operative.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

Status of Plan

Change 79

5.1 Council

adopted the recommendation on Plan Change 79 (PC79) on 19 February 2026, with

the decision released on 13 March 2026. At that point, PC79 moved to decision‑stage

under Schedule 1 of the Resource Management Act 1991 (RMA).

5.2 An

appeal has been lodged against specific provisions of the PC79 decision. The

appeal does not relate to all aspects of the plan change. As a consequence,

PC79 is now partially subject to the Environment Court’s jurisdiction,

which may result in changes to PC79.

Statutory

Authority to Make PC79 Operative in Part

5.3 Clause 17(2)

of Schedule 1 of the Resource Management Act 1991 provides that a local

authority may approve part of a plan, where all submissions or appeals relating

to that part have been disposed of. In this case, the appeal to Plan Change 79

is limited in scope, and the provisions proposed to be approved are not subject

to appeal.

5.4 Once approved in part under

Clause 17, Clause 20 of Schedule 1 provides for Council to

publicly notify the date on which those approved provisions become operative.

5.5 This

approach reflects established and accepted practice under Schedule 1, allowing

provisions that are not subject to further consideration, including Environment

Court litigation, to take effect without further delay.

Severability of

the Unappealed Provisions

5.6 The appeal to PC79 is

limited in scope and is directed at particular objectives, policies and rules

that relate to the deferral mechanism. The remaining provisions of PC79 have

not been appealed by any party and are discrete from those under appeal.

5.7 The

provisions not under appeal are capable of operating independently of the

appealed provisions and can be integrated into the operative TRMP without

affecting:

· the scope of the

appeal; or

· the Environment

Court’s ability to determine the appealed matters.

Why approve and

make operative in part now?

5.8 In

recommending that PC79 be made partially operative, it is important that the

appeal is confined to a discrete set of provisions relating to the deferred

zoning mechanism and does not extend to the site‑specific

rezoning outcomes or the provisions that enable development on land that has

been ‘up‑zoned’ (i.e. the zoning has been amended so it is no longer deferred).

5.9 One reason for proceeding to

make the provisions not under appeal operative at this stage improves the

clarity and usability of the TRMP. This is particularly relevant given the

imminent public notification of Plan Change 81. Maintaining a clean and up‑to‑date operative planning

framework will assist the public to understand the operative baseline from

which Plan Change 81 is proposed, and to make informed submissions, as well as

assisting with the usability of the Plan generally.

Advice to Council

5.10 This report does not reconsider the

merits of PC79. It is procedural in nature and is confined to implementing

Council’s earlier decision to the extent permitted by the RMA.

5.11 It is therefore lawful for Council to

approve and make PC79 operative in part, limited to those parts of PC79 where

the submissions on those parts have been disposed of. Put another way, it

can approve the PC79 provisions that are not subject (directly or indirectly)

to appeal.

5.12 Staff are confident that the identified

parts of PC79 can be approved and made operative because the provisions and

rezonings relate specifically to rezonings and site specific provisions,

whereas the appeal is focused on the deferral mechanism.

5.13 This approach gives effect to

Council’s decision of 19 February 2026, provides regulatory certainty

where possible, improves and assists with the readability and usability of the

Plan and preserves the appeal process for the provisions that remain before the

Environment Court.

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

6.1 The provisions of Plan

Change 79 that are not subject to appeal include those that implement

zoning changes and enable development to proceed on

sites identified for urban use. These provisions give effect to Council’s

decision to release specified locations from deferred zoning where

infrastructure is in place and the resulting urban zoning is no longer in

dispute. Enabling development on these locations will provide return on

investment for Council for the infrastructure it has installed.

6.2 The appealed provisions are

discrete and separable from the zoning and development‑enabling

provisions proposed to be made operative. Making the provisions not under

appeal operative at this stage will enable development to proceed on the up‑zoned

sites without prejudicing or constraining the Environment Court’s

consideration of the appeal.

6.3 Management of the appeal

– being a separate matter – will involve additional legal and staff

costs.

7.1 The options

are outlined in the following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Make Plan Change 79 operative in part

|

Gives effect

to Council’s decision of 19 February 2026 in respect of the

provisions that have been disposed of and are not under appeal.

Enables the

zoning changes and development‑enabling provisions for the up‑zoned

locations to take effect, providing certainty for landowners and consent

processing.

Approves

usability and readability of the Plan.

Is consistent

with Clause 17(2) of Schedule 1 of the Resource Management Act

1991 and established practice where only part of a plan change decision is

under appeal.

Preserves the

Environment Court’s jurisdiction over the appealed provisions.

|

None

identified. The appealed provisions remain unaffected and are excluded from

becoming operative at this time.

|

|

2.

|

Defer making any part of Plan Change 79 operative until

the appeal is resolved

|

Defers implementation of all provisions until the appeal

process is complete

|

Delays the

operation of zoning provisions not under appeal that are no longer in

dispute.

Defers

development enabled by the up‑zoned locations, contrary to

Council’s earlier decision.

Provides no practical benefit where severable provisions

can lawfully be made operative in part

|

7.2 Option 1 is

recommended.

8.1 A plan change must be

approved by Council before it is made operative by public notification under cl

20 Schedule 1 to the Resource Management Act 1991. This is an

administrative process rather than a substantive decision. There is a

quirk in the Resource Management Act 1991 as it states that rules become

operative once they are beyond challenge but then goes on to state in a later

clause that to make a plan or change operative requires approval by Council and

then it must affix its seal to the change.

8.2 Clause 17(2) of

Schedule 1 of the Resource Management Act 1991 provides that Council may

approve part of a plan where all submissions or appeals relating to that part

have been disposed of. In this case, the provisions proposed to be made operative

are not subject to appeal, therefore any submissions on those provisions have

been disposed of.

8.3 The appealed provisions of

Plan Change 79 remain subject to the jurisdiction of the Environment

Court and will not be approved under this process.

8.4 Once approved in part under

Clause 17, Clause 20 of Schedule 1 enables Council to

publicly notify the date on which the approved PC79 provisions become

operative.

9. Iwi

Engagement / Whakawhitiwhiti ā-Hapori Māori

9.1 Iwi were engaged through the

Schedule 1 process for Plan Change 79, including during pre‑notification

and formal consultation stages. That engagement informed Council’s

decision on the plan change adopted on 19 February 2026.

9.2 This report does not

introduce new policy content or alter the substance of the Plan Change. It is

procedural in nature and relates solely to the implementation of provisions of

the existing decision not under appeal. As such, no additional iwi engagement

is required for the matters addressed in this report.

10. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

10.1 The Council is not

required to undertake further consultation prior to making the decision sought

through this report.

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Low

|

Procedural step and

of little interest to general public

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Medium

|

Making the plan

change operative in part will release deferred zoned land that is serviced,

now and in the future for urban development. This will assist to satisfy the

residential, housing and business growth demands of the District.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Low

|

As for 2 above.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

No.

|

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

No.

|

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

No

|

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

No

|

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

No

|

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

No

|

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

No

|

|

11. Communication

/ Whakawhitiwhiti Kōrero

11.1 If Council resolves to make Plan

Change 79 operative in part, public notice will be given in accordance

with Schedule 1 of the Resource Management Act 1991. The operative

provisions will be incorporated into the Tasman Resource Management Plan, and

the appeal status of the remaining provisions will continue to be clearly

identified.

11.2 No additional consultation or targeted

communications are proposed, as this decision gives effect to Council’s

existing decision and does not introduce new policy content.

12.1 The primary risk associated with making

Plan Change 79 operative in part is the potential for confusion if

operative and non‑operative

provisions are not clearly distinguished. This risk will be managed through

clear public notice and plan administration, with appealed provisions remaining

expressly identified as subject to the Environment Court process.

12.2 There is no legal risk in making Plan

Change 79 operative in part where provisions not under appeal are

severable from the matters under appeal. This approach is expressly provided

for under Schedule 1 of the Resource Management Act 1991 and does not

prejudice the appeal.

12.3 Deferring implementation of provisions

not under appeal would create a risk of unnecessary delay in giving effect to

Council’s decision, including delayed uptake of zoning provisions

intended to enable development of up‑zoned

locations. It also increases the risk of confusion for people seeking to

make submissions on PC81 when it is notified due to difficulty in identifying

which provisions relate to which plan change.

13. Climate

Change Considerations / Whakaaro Whakaaweawe Āhuarangi

13.1 Climate change considerations,

including natural hazard and sea level rise risks where relevant, were

addressed through the Schedule 1 process for Plan Change 79 and

informed Council’s decision adopted on 19 February 2026.

13.2 This report does not propose any new

zoning, policies or rules, nor does it alter the substantive content of Plan

Change 79. It is procedural in nature and relates only to making

provisions not under appeal operative.

13.3 As such, there are no additional

climate change implications arising from the matters addressed in this report

beyond those already considered through the plan change process.

14. Alignment

with Policy and Strategic Plans / Te Hangai ki ngā aupapa Here me ngā

Mahere Rautaki Tūraru

14.1 PC79 contributes to implementing the

Nelson Tasman Future Development Strategy (FDS) and assists the Council in

meeting its obligations under the National Policy Statement for Urban

Development.

14.2 PC79 also enables development that is

consistent with the Infrastructure Strategy to ensure that infrastructure that

is built by the Council is well utilised.

15. Conclusion

/ Kupu Whakatepe

15.1 The appeal to Plan Change 79 is

limited in scope and does not relate to all provisions of the plan change. The

zoning and development‑enabling

provisions proposed to be made operative are not subject to appeal and are

clearly severable from the matters before the Environment Court.

15.2 Clause 17(2) of Schedule 1

of the Resource Management Act 1991 enables Council to approve part of a plan

where all submissions or appeals relating to that part have been disposed of.

Making Plan Change 79 operative in part gives effect to Council’s

decision of 19 February 2026 in respect of the provisions not under

appeal, without prejudicing the appeal.

16. Next Steps

and Timeline / Ngā Mahi Whai Ake

16.1 If Council resolves

to make Plan Change 79 operative in part:

· the

approved provisions not under appeal will be sealed in

accordance with Clause 17 of Schedule 1;

· public

notice of the operative provisions and operative date will be given in

accordance with Clause 20 of Schedule 1;

· the

operative provisions will be incorporated into the Tasman Resource Management

Plan and into Plan Change 81 which is due to be publicly notified soon; and

· the

appealed provisions will remain subject to the Environment Court process until

the appeal is resolved.

|

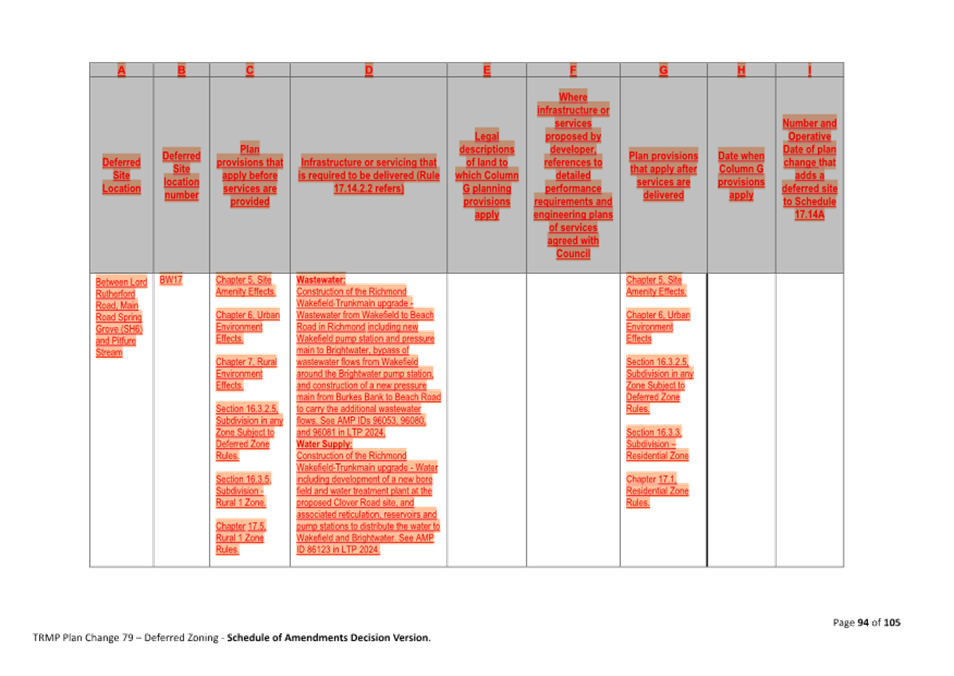

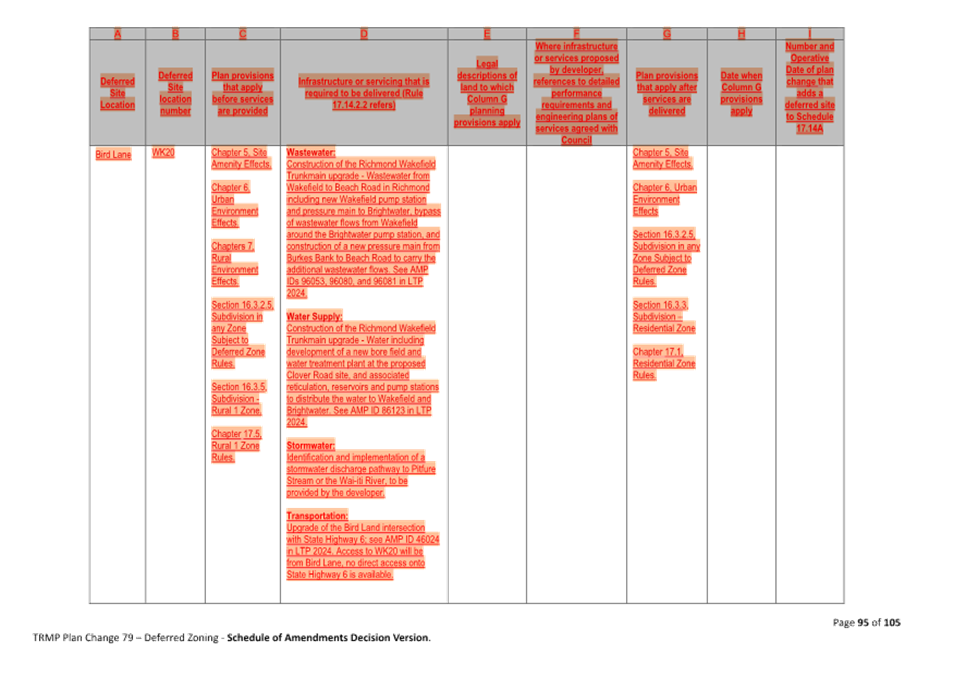

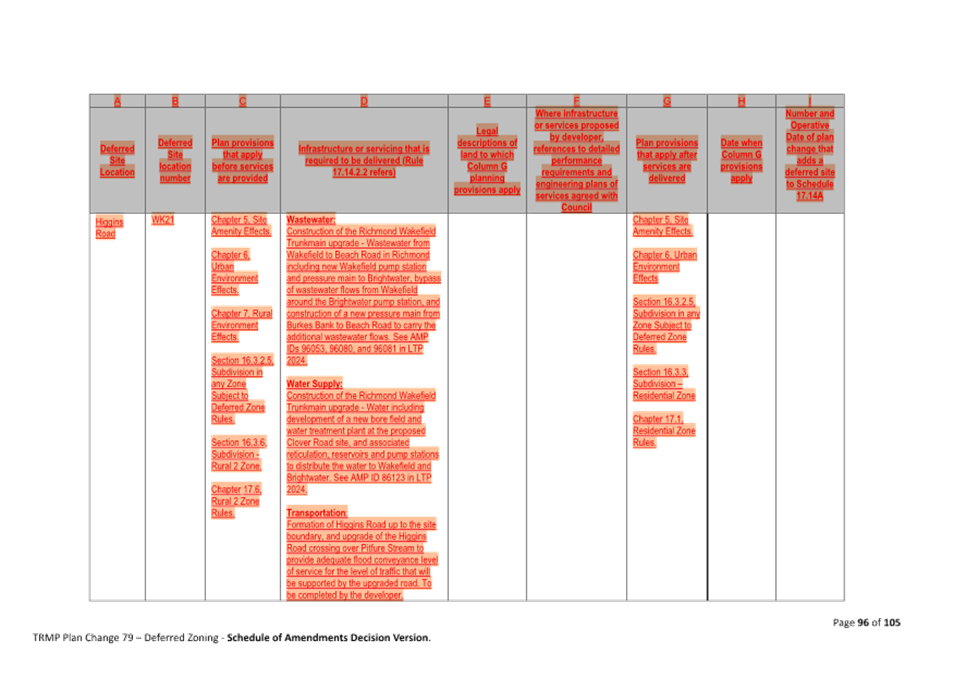

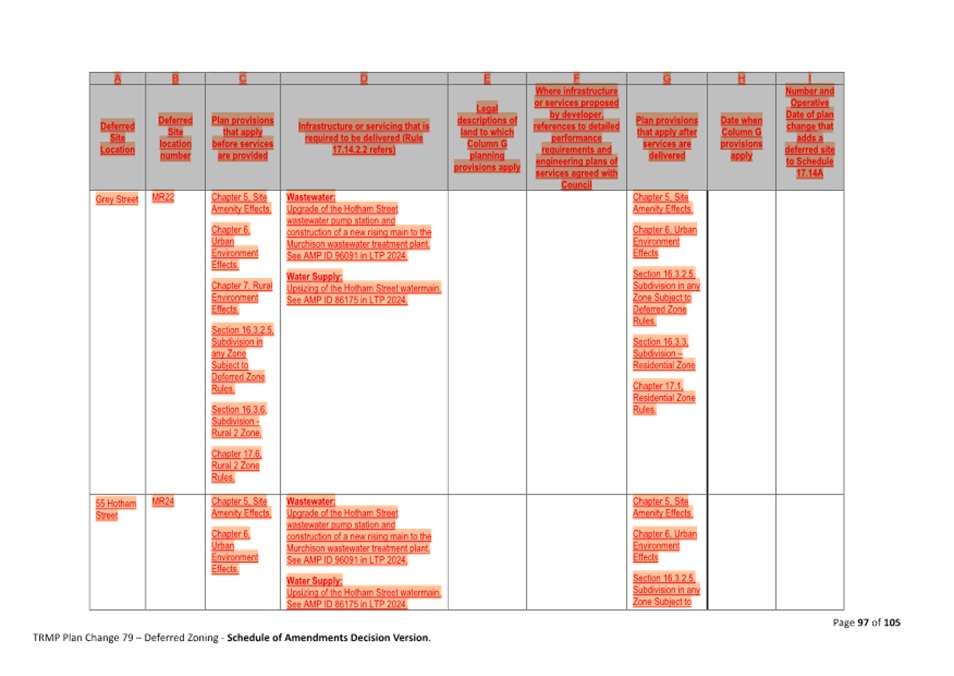

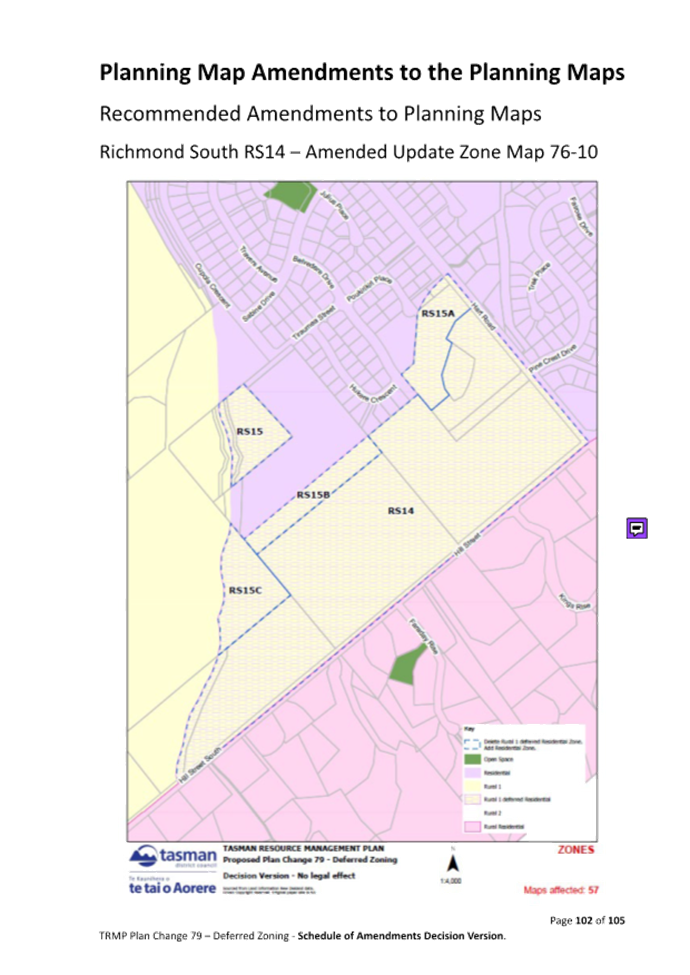

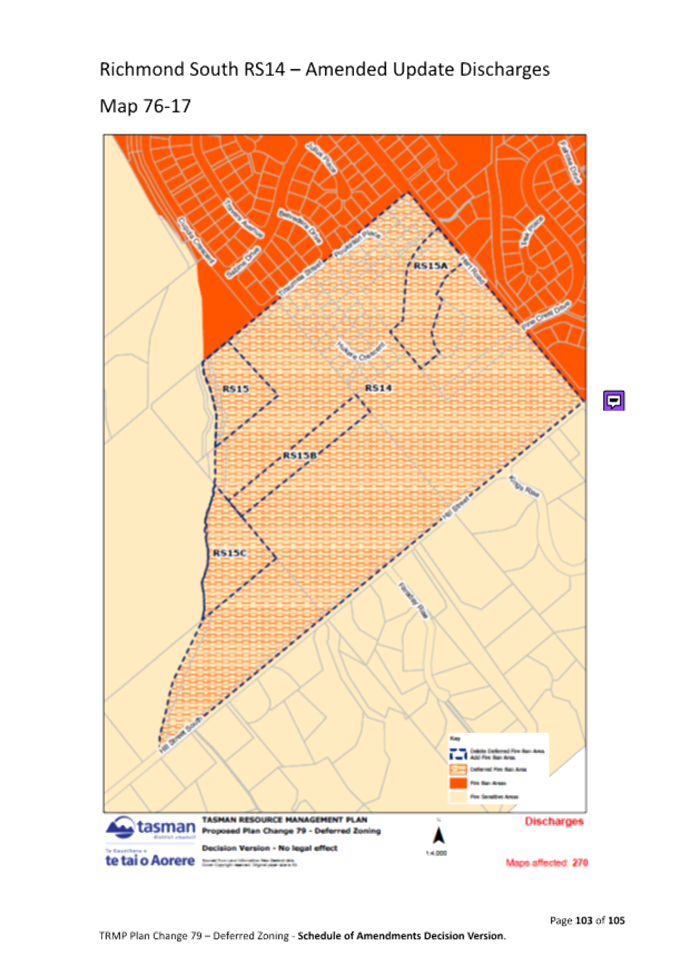

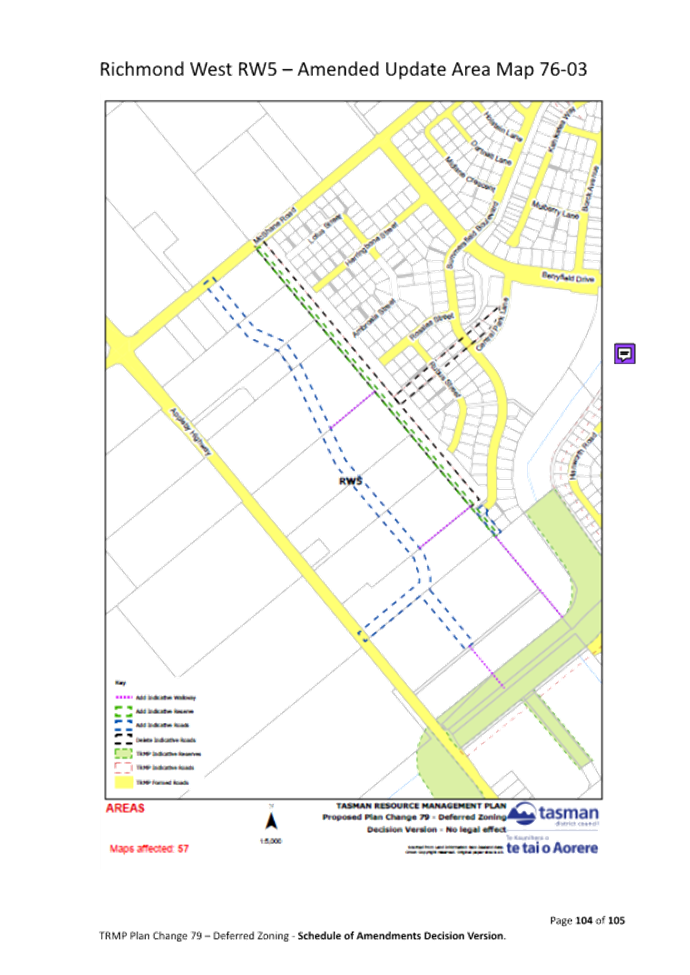

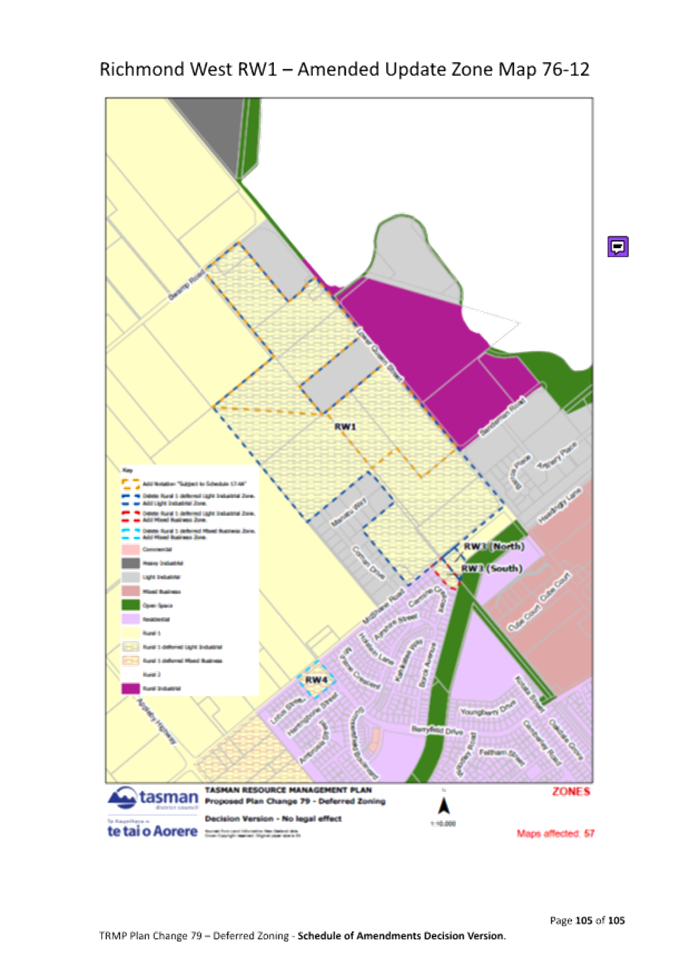

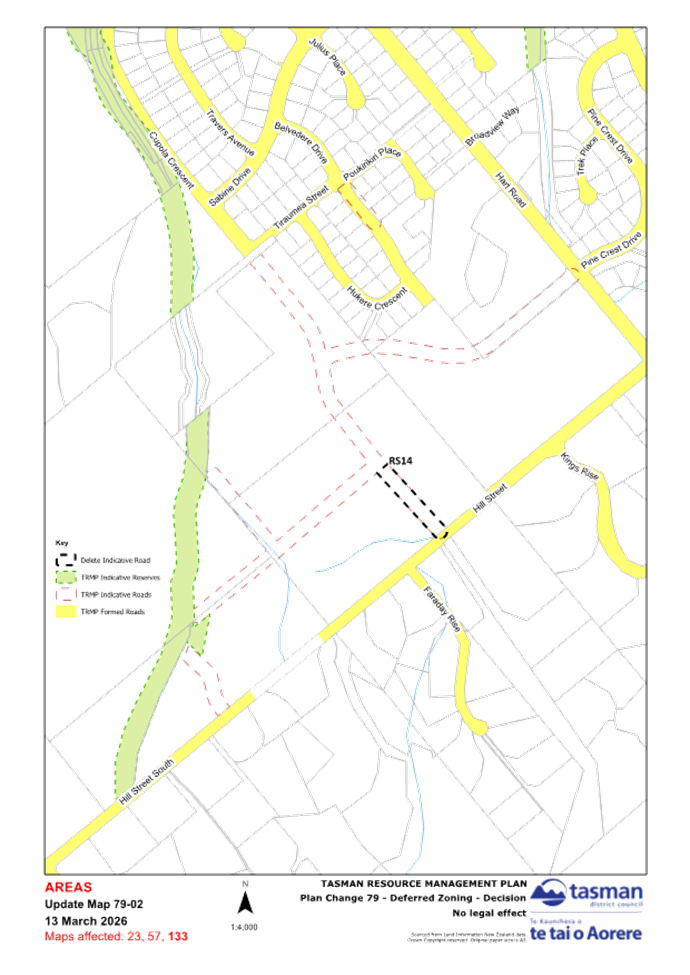

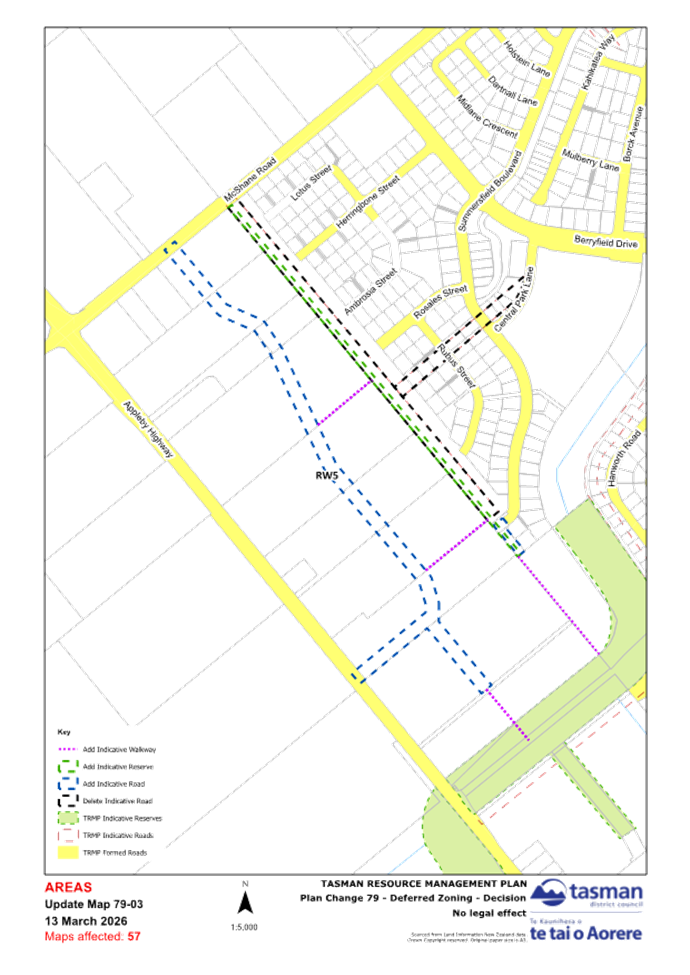

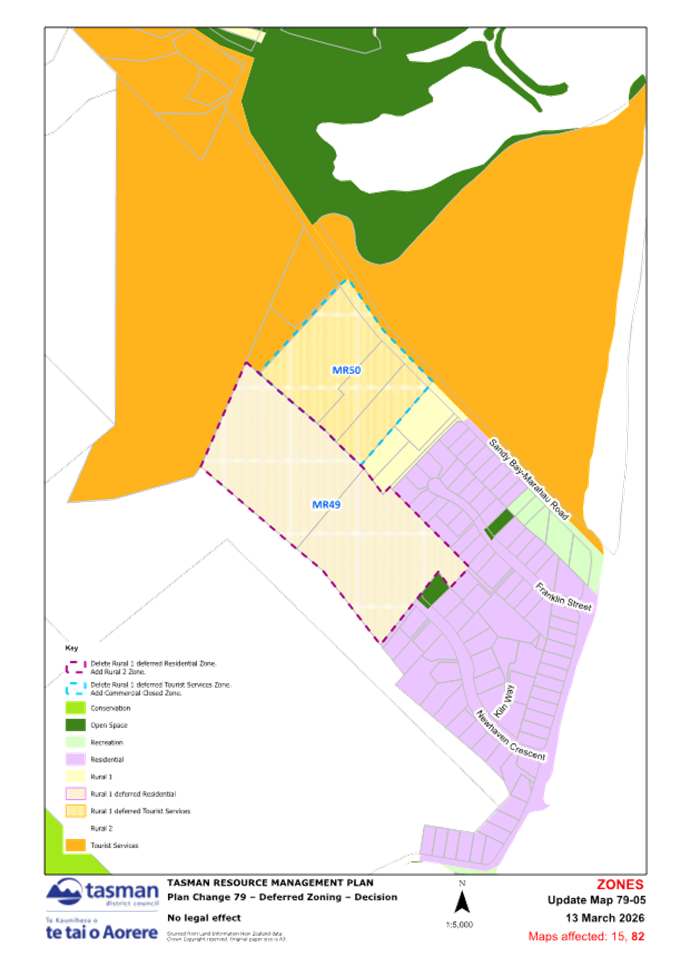

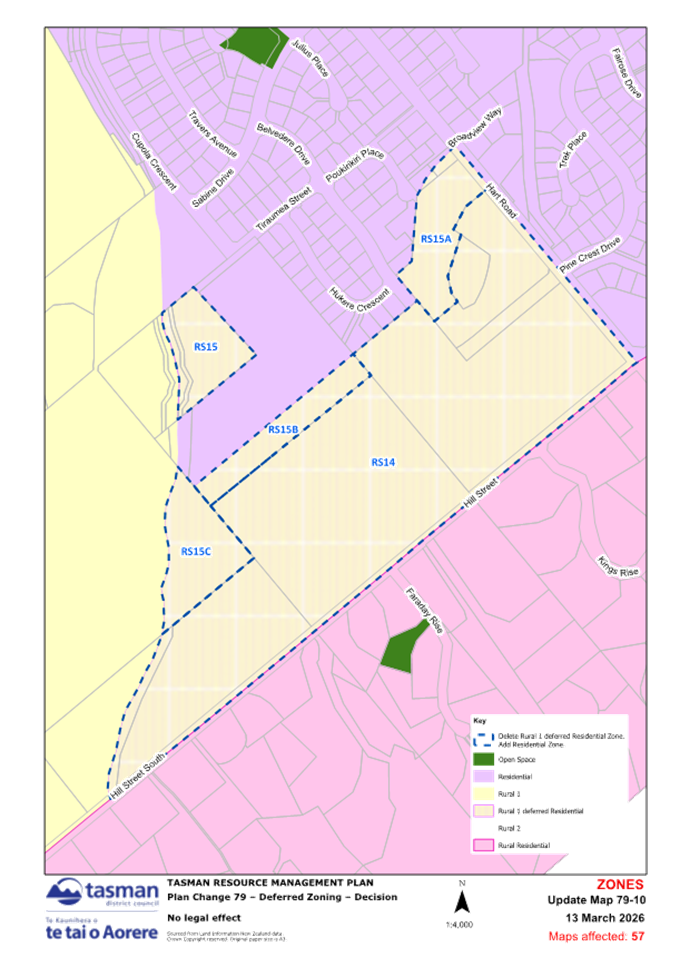

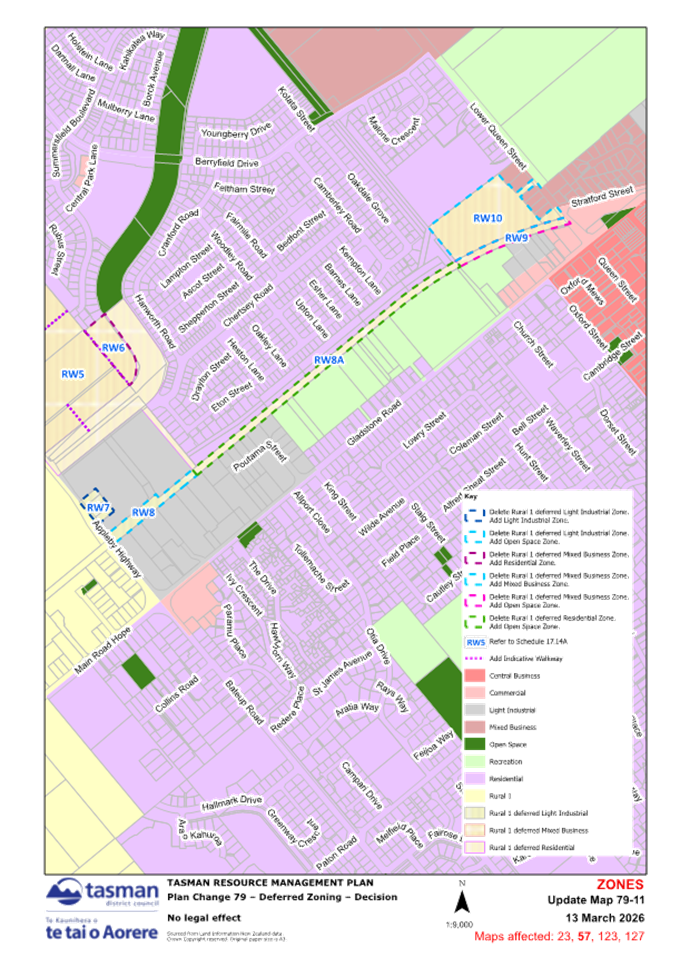

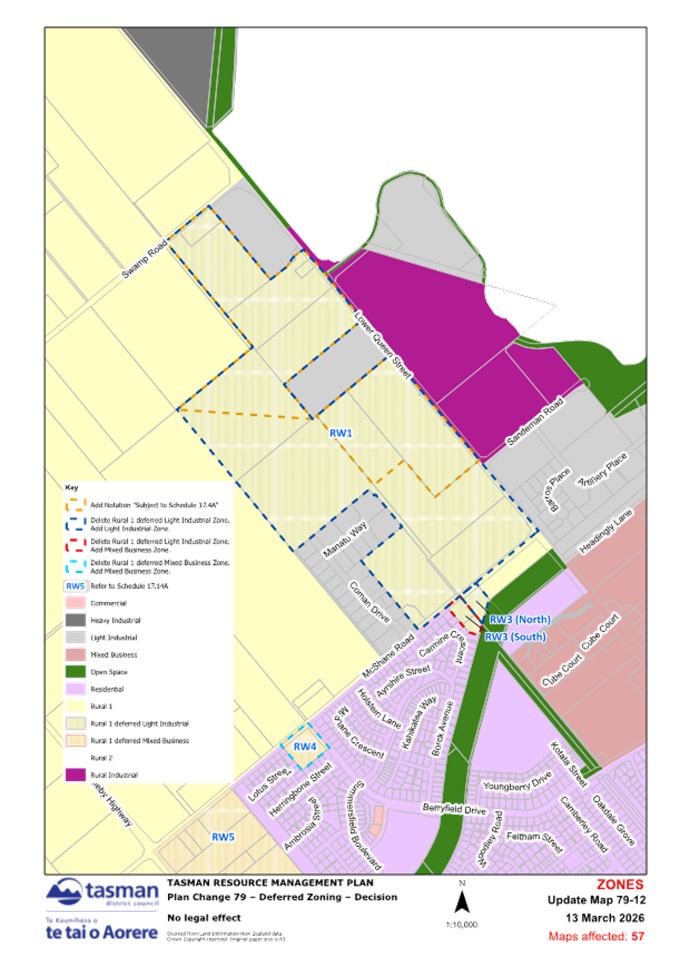

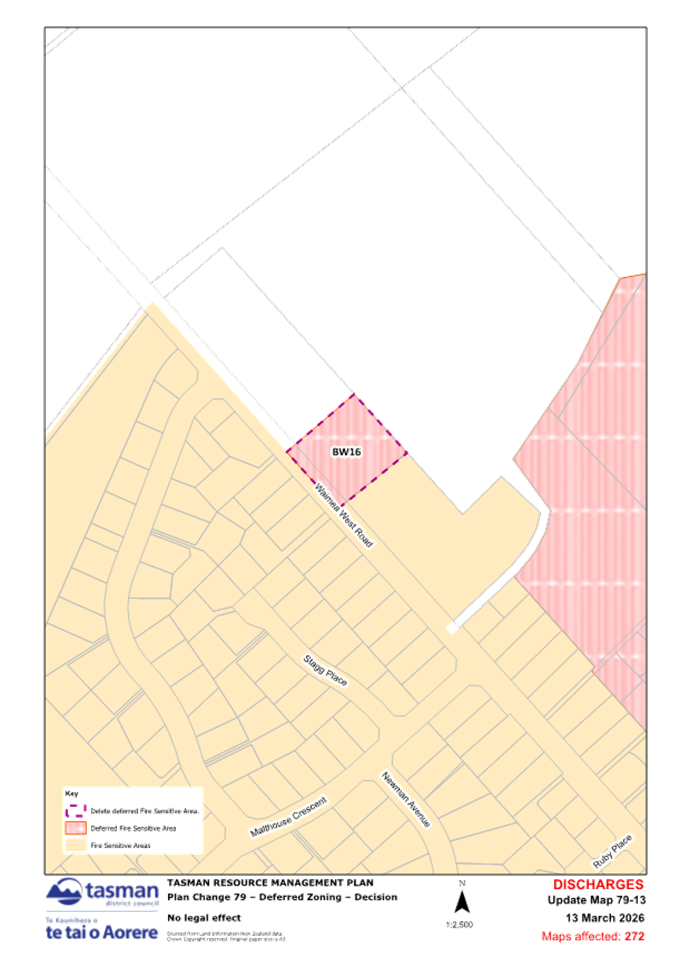

1.⇩

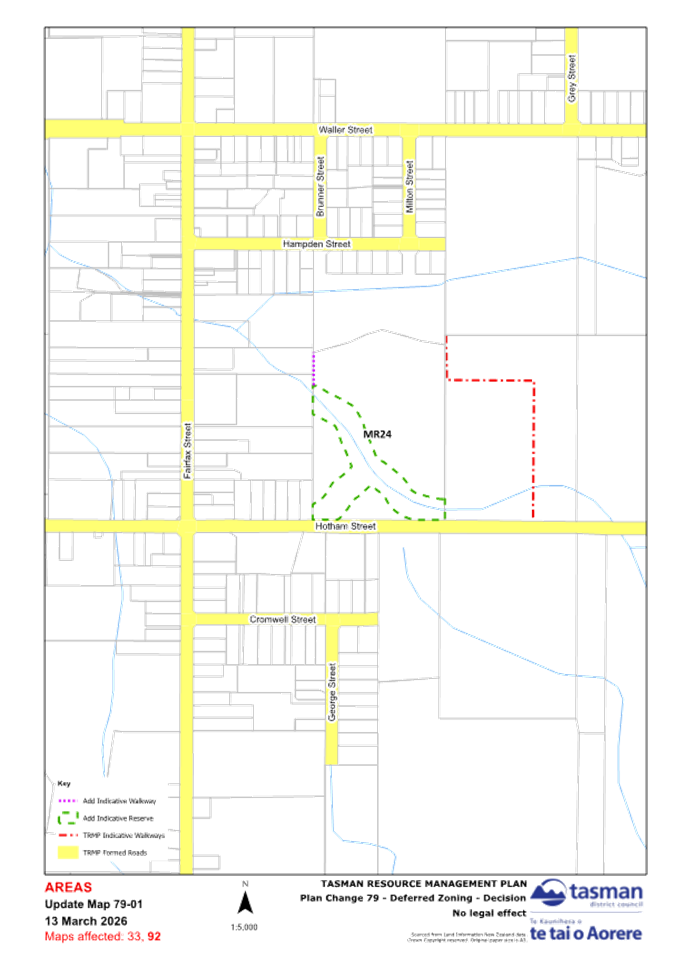

|

Provisions

to be approved (not highlighted) and not approved (highlighted in orange)

|

13

|

|

2.⇩

|

Appeal

document

|

118

|

|

3.⇩

|

Map: Areas

Murchison

|

333

|

|

4.⇩

|

Map: Areas

Richmond South

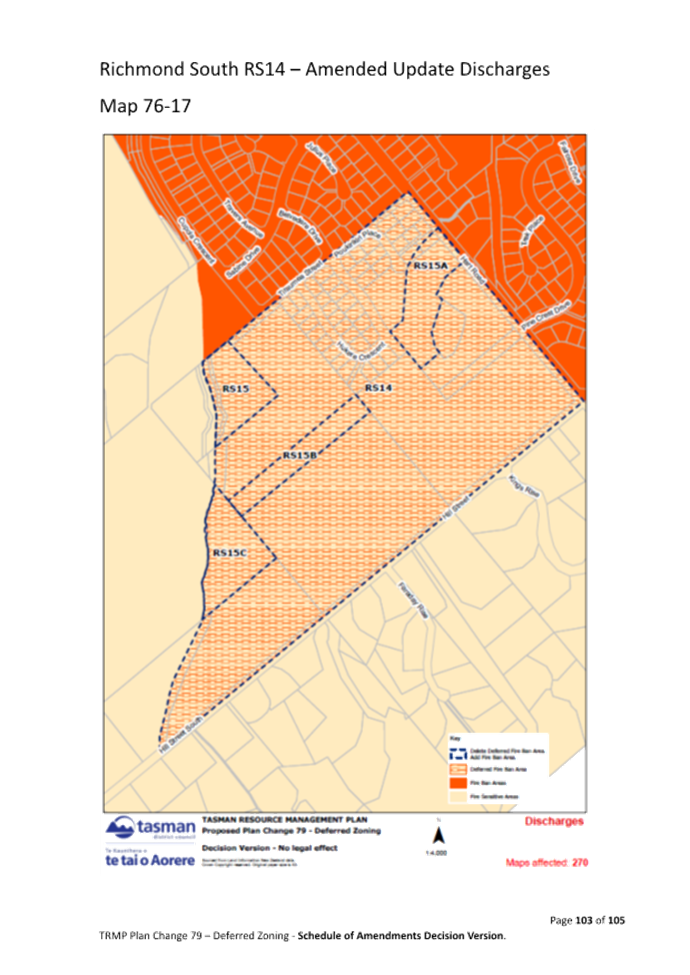

|

334

|

|

5.⇩

|

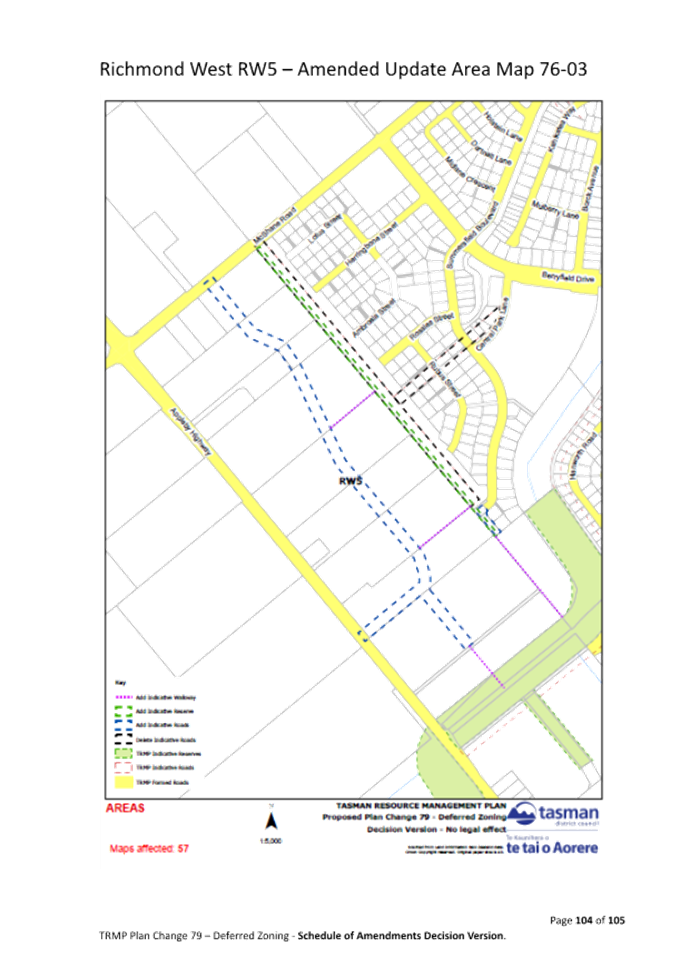

Map: Areas

Richmond West

|

335

|

|

6.⇩

|

Map: Zones

Brightwater

|

336

|

|

7.⇩

|

Map: Zones

Marahau

|

337

|

|

8.⇩

|

Map: Zones

Moutere

|

338

|

|

9.⇩

|

Map: Zones

Murchison

|

339

|

|

10.⇩

|

Map: Zones

Patons Rock

|

340

|

|

11.⇩

|

Map: Zones

Richmond East

|

341

|

|

12.⇩

|

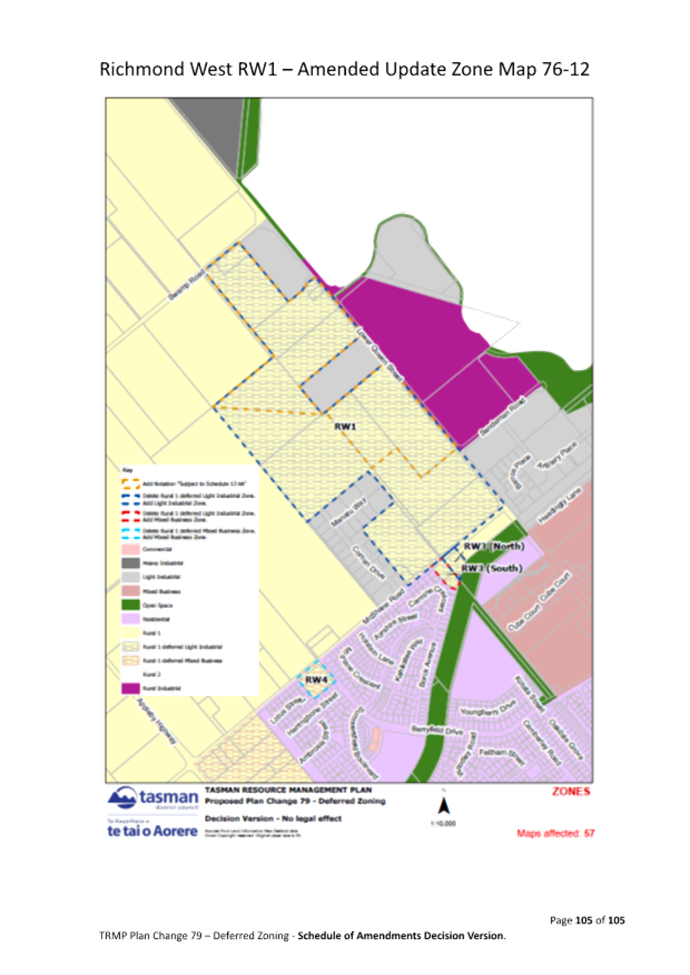

Map: Zones

Richmond South

|

342

|

|

13.⇩

|

Map: Zones

Richmond West A

|

343

|

|

14.⇩

|

Map: Zones

Richmond West B

|

344

|

|

15.⇩

|

Map:

Discharges Brightwater

|

345

|

|

16.⇩

|

Map:

Discharges Marahau

|

346

|

|

17.⇩

|

Map:

Discharges Murchison

|

347

|

|

18.⇩

|

Map:

Discharges Richmond East

|

348

|

|

19.⇩

|

Map:

Discharges Richmond South

|

349

|

|

20.⇩

|

Map:

Discharges Richmond West A

|

350

|

|

21.⇩

|

Map:

Discharges Richmond West B

|

351

|

7.2 Annual Plan 2026/2027 and Schedule of Fees and

Charges - Deliberations Report

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

28

May 2026

|

|

Report

Author:

|

Amy

Smith, Community Policy Advisor; Emily Garland, Graduate Community Policy

Advisor; Dwayne Fletcher, Strategic Planning & Enterprise Manager; Matthew

McGlinchey, Financial Strategy & Planning Manager; Alan Bywater, Team

Leader - Community Policy

|

|

Report

Authorisers:

|

Dwayne

Fletcher, Strategic Planning & Enterprise Manager; Leonie Rae, Chief

Executive Officer

|

|

Report

Number:

|

RCN26-05-14

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 The

purpose of this report is to:

1.1.1 Provide a summary of submissions received on the Annual

Plan 2026/2027 and Schedule of Fees and Charges 2026/2027;

1.1.2 Provide the Mayor and Councilors with an opportunity to

discuss and obtain advice from staff on matters raised in the submissions; and

1.1.3 Make decisions on matters to be included in the Annual

Plan 226/2027.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 At

its meeting on 19 March 2026 the Council made a series of decisions on changes

from the Long-Term Plan 2024-2034 (LTP) for 2026/2027.

2.2 The

net outcome of these changes was a rates revenue increase of 9.9% (excluding

growth) for 2026/2027, and net debt is project to be $320m. This was an

increase compared to the 5.2% (excluding growth) planned for Year 3 of the LTP.

As a result, the Council agreed to consult on the Annual Plan 2026/2027 and

Schedule of Fees and Charges 2026/2027.

2.3 At

its meeting on 2 April, the Council adopted a consultation document and

supporting material and a public consultation period was open from 2 April

until 3 May 2026. The Submissions Hearing meeting was held on 14 May and 44

submitters were heard.

2.4 There

were 367 submissions received over the consultation period, including 46 from

groups and organisations. Staff have prepared an overview of the submissions (Attachment

1) and all submissions can be accessed and viewed here: TDC

Submissions.

2.5 Two

other matters have arisen over the last few weeks that staff wish to address in

the final Annual Plan:

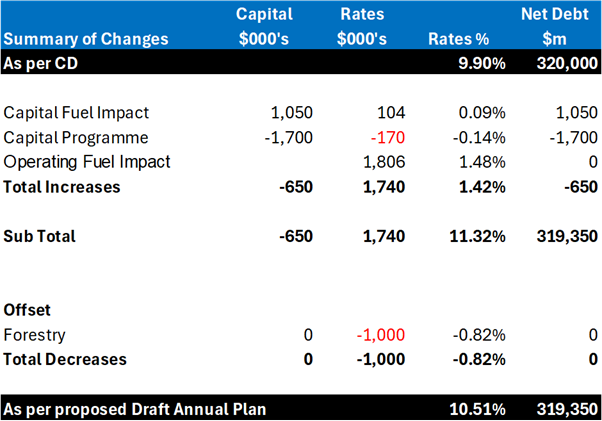

2.5.1 Estimated operating fuel price impact of $1.8m for

2026/2027 (1.48% additional rates) and a capital impact of roading resealing of

$1.05m ($105k loan servicing, or 0.09% additional rates).

2.5.2 A review of the deliverability of the capital programme

for 2025/2026 and the proposed capital programme 2026/2027, which has resulted

in proposed budget reductions with reduction in rates of 0.14% and a reduction

in net debt of $1.7m.

2.6 In

the 7 May Council report, the following financial pressures in 2025/2026 were

raised:

2.6.1 Three Waters maintenance overspend of $1.85m.

2.6.2 Oil price impact of $328k (a decrease from the

previously advised $500k).

2.7 Staff

believe these costs can be absorbed within the current financial year without

impacting the 2026/2027 Annual Plan. This is due to careful management of costs

in some areas to provide temporary relief and additional revenue from gravel

extraction and water consumption.

2.8 Staff

advise amending the proposed fee structure for property files, as a result of

feedback received in submissions. The dog control fees are to be adopted at this meeting as proposed,

to enable the statutory notification requirements to be met. The remainder of

the schedule of fees and charges will be presented for adoption at the 25 June

2026 Council meeting.

2.9 Overall

the impacts of the above listed items is a rates increase for the 2026/2027 of

11.3% (excluding growth), which is an increase of 1.4% on what we consulted on.

Debt would be $650k, less than the $320m, consulted on.

2.10 To

reduce the impact of this increase on the community at a difficult time, staff

have investigated the feasibility of increasing forest harvesting in the short

term. We believe we can generate an additional $1.0m (net) for the 2026/2027

year, although advice from PF Olsen will not be finalised when

this report is circulated. This will result in a rates revenue increase

of 10.5% instead of 11.3% (excluding growth). Note that any

lift in revenue for 2026/2027 is only temporary and not sustainable into the future

– it will reduce forestry income in future years.

2.11 Elected

members may want to consider this option as it increases the proportion of

operating expenditure funded from operating revenue, which supports the

Council’s objective of improving financial sustainability over time.

2.12 If

the Council wants to retain the 9.9% (excluding growth) rates revenue increase

it consulted on, it could increase debt funding of operational costs for

2026/2027 by $750k. This would smooth the impact of the oil price shock on the

community, assuming it is temporary in nature. This is relativity

straightforward but will shift us further from financial sustainability and may

put more pressure on the rates increase required for following financial years,

especially 2027/2028.

2.13 Staff

have not included service reviews as an option to reduce costs. The

organisation operates lean for the services it offers, three such reviews have

occurred in recent years and another is currently progressing within the LTP,

organisation resources are strained, and there is insufficient time or

resources to complete this process and undertake any necessary consultation in

time to finalise the Annual Plan 2026/2027 in approximately four weeks time.

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman

District Council

1. receives

the Annual Plan 2026/2027 and Schedule of Fees and Charges - Deliberations

Report RCN26-05-14; and

Changes and financial impacts

2. approves the revised capital programme for 2026/2027 in Attachment 1

to the agenda report, noting the projects that have been delayed and likely

consequences of these changes; and

3. notes that fuel cost increases are estimated to increase operating

costs for core services by $1.8m across Council and by $1.05m in the capital

transportation activity in 2026/2027, and that this has been included in

revised budgets; and

4. notes that staff expect increased maintenance costs in Three Waters

activities and contract fuel costs in 2025/2026 will be largely offset by

additional revenue or savings within the same activities and have no material

bearing on the starting position for the 2026/2027 year; and

Key proposals in the Annual Plan

5. approves

the introduction of a recovery rate for five years to

repay the costs of the 2025 weather events only, charged as a uniform fixed

amount per rating unit in the Annual Plan 2026/2027; and

6. requests staff to amend the Revenue and Financing Policy and Funding

Impact Statement to be consistent with resolution 5. (a recovery rate for five

years) for adoption at the 25 June 2026 Council meeting; and

7. agrees to the following next steps for the three community

facilities projects:

7.1 pause and defer the Tapawera Community Hub project to the next Long

Term Plan; and

7.2 continue

the Waimea South facilities projects (Wakefield Community Hub and Brightwater

facilities), as planned; and

7.3

continue the Motueka Pool project as planned, progressing through the design

stage; and

8. agrees to slow funded depreciation for roading assets as proposed in

the consultation document, with a target of 21% to be reached by the end of

2026/2027; and

9. agrees

to retain most fees and charges as proposed and make the following changes to

the fee structure for property files:

9.4 reducing

the proposed fee for individual property owners from $30 to $25 per property

file; and

9.5 retaining

the proposed ‘pay as you go’ charge of $60 per property file; and

9.6 introducing

a flat rate of $40 per property file for bulk users, rather than the proposed

$3,000 fee for 60 files (equivalent to $50 per file); and

10. adopts the Dog Control fees set out in Attachment 3 to the agenda

report, to allow for public notification in the month before the fees take

effect, in accordance with the Dog Control Act 1996; and

Response to submissions

11. notes in-principle support from the Motueka Community Board to

allocate funding from its 2025/2026 Special Projects Fund to the Motueka

Heritage Wharf Restoration Project, and this will be considered by the Board at

its 16 June 2026 meeting; and

12. notes

staff advice at paragraph 0 of this report in response to requests from the

Motueka Community Board in its submission; and

13. requests

staff further develop funding options for the Eighty Eight Valley Water Scheme

based on percentages of the urban metered charge, for further consideration in

the Long Term Plan 2027-2037; and

14. notes

that a comprehensive rating review for rivers has been initiated; and

15. declines the request to start maintaining the section of Tasman View

Road from the junction with Harley Ridge to “the Lookout”; and

16. notes that budget provision for stormwater improvements on Welsh

Place, Richmond has been included in the Annual Plan budget; and

17. notes that project scoping for work on the Riuwaka River stopbanks

has been initiated and staff are working directly with affected landowners; and

Finalising the Annual Plan

18. notes

that the net impact of cost increases of $1.7m to the Annual Plan results in a

total rate revenue increase of 11.3% (excluding growth) and end of year net

debt of $319.4m for 2026/2027; and

19. agrees

that a $1.0m increase in net forestry income is used to reduce the rates

revenue requirement for 2026/2027 to 10.5%, noting this lift is not sustainable

and will reduce future forestry income; and

20. agrees

the remaining impacts of cost increases to the Annual Plan 2026/2027 will be

funded via rates, resulting in a 10.5% rates revenue increase;

OR

agrees that the remaining

impacts of cost increases to the Annual Plan 2026/2027 will be funded via debts

resulting in a rates revenue increase of 9.9%; and

21. notes

that the Annual Plan 2026/2027 will be presented for adoption at the Tasman

District Council meeting on 25 June 2026.

4.1 Since the adoption of the LTP 2024-2034 and the Annual Plan

2025/2026, there have been a range of factors that have increased the

Council’s expected costs for 2026/2027. The primary drivers of

these increased costs are:

4.1.1 The impacts of the

June/July 2025 weather events;

4.1.2 New costs resulting from

water supply and resource management regulation from central government;

4.1.3 Higher than anticipated

interest rates, loan repayment and depreciation funding (as a result of

increased asset valuations);

4.1.4 Higher than anticipated

operating costs for the Regional Sewerage Business Unit, resulting from

Council’s increased use (capacity) of the network to support

growth;

4.1.5 Higher than anticipated

reactive maintenance costs in Three Waters, Transportation and Reserves and

Facilities activities; and

4.1.6 Increased Waimea

Community Dam costs re settlement $3.8m.

4.2 In addition, expenditure forecasts for the 2025/2026 year

indicated that the Council will have a larger net operating deficit than

planned (i.e. more unfavourable) because of the impact of the weather event

(net impact $14.6m). This affects the financial starting position for the

2026/2027 Annual Plan year.

4.3 We

are unable to maintain our current Levels of Service within the planned (LTP)

rates increase or indicative rates increase identified in the last Annual Plan

process. A forecast rates rise of 11.2% (excluding growth) for the Annual Plan

2026/2027 was identified in November 2025.

4.4 To

try and limit the impact of the increasing costs on rate increases for

2026/2027 the Council has:

4.4.1 Sold approximately

$0.35m of unencumbered ETS credits to reduce the rates requirement for

2026/2027 by -0.3%.

4.4.2 Proposed reducing

planned increases in funding depreciation from operating revenues

(i.e.‘cash funding’ depreciation) for roading by 3%, from 24% to

21%, by the end of 2026/202, against our target of 49% by 2030, reducing the

rates requirement for 2026/2027 by -0.5% or approximately $650,000.

4.4.3 Proposed a new 2025

Weather Event Recovery Rate to fund the recovery costs (debt) of $14.6m

resulting from the 2025 weather events ($2.8m in 2026/2027 rating year).

4.4.4 Proposed pausing and

deferring the Tapawera Community Hub project to the next LTP process.

4.4.5 Proposed increasing most

fees and charges by 7.0%.

4.4.6 Adjusted operational and

capital budgets.

4.5 At its meeting on 19 March 2026, the

Council made a series of decisions on changes from the LTP 2024-2034 for

inclusion in the Annual Plan for consultation.

4.6 At its meeting on 2 April 2026, the

Council adopted a consultation document and supporting material, including the

draft Schedule of Fees and Charges 2026/2027, for a public consultation period

that ran from 2 April to 3 May 2026.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 This section:

5.1.1 covers a range of cost impacts that have been identified

since consultation began;

5.1.2 summarises the feedback received during consultation;

5.1.3 presents submitter requests, staff advice and

recommendations; and

5.1.4 discusses the net impact of

these changes to the Annual Plan and sets out the options available to the Council, with recommendations.

Changes and impacts identified since consultation

5.2 A number of changes are proposed by

staff that have financial implications and are discussed below. The changes

have resulted as further information has come to light since the draft Annual

Plan was approved for consultation.

Current year operational position

5.3 Several cost escalations are hitting the

current financial year, but staff forecast these will largely offset by

additional revenue from gravel extraction and water consumption or reductions

elsewhere due to careful management of costs to provide temporary relief,

largely within the same activities. Overall, these are not forecast to

materially affect the starting position of the 2026/2027 financial year

compared to the forecast used to underpin the Annual Plan 2026/2027 position to

date.

5.4 Cost increases include additional

maintenance costs in Three Waters and additional fuel costs across the board.

Areas where there will be savings against budget for the current 2025/2026

financial year include (but is not limited to);

5.4.1 Gravel Income $300k more than planned

5.4.2 Targeted volumetric water: $650k higher than planned

(noted earlier)

5.4.3 Operational NRSBU costs: $515k lower than planned

5.4.4 Net interest costs: $250k lower than planned

These savings

are indicative.

There is a risk

that the forecast savings do not eventuate. If this is the case the deficit

position will need to be recovered in the first year of the LTP. An activity

report on the final year-end closed account positions will be presented to the

Strategic, Finance and Performance Committee when it meets on 17th

September. The required transfers of balances will be submitted for approval at

that meeting.

Impact of

the fuel crisis

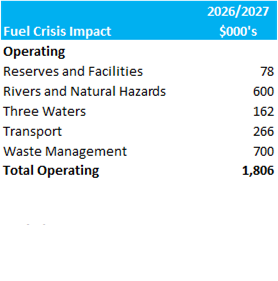

5.5 In a report to the Council on 7 May

2026 (refer to RCN26-05-10), the potential cost of the fuel crisis was noted

across the Council. These figures have been reviewed and the impacts for

2026/2027 updated in the table below:

The figures in

the table are still indicative only; the reality may be better or worse and how

this plays out is extremely difficult to predict.

Changes to

the 2026/2027 capital programme

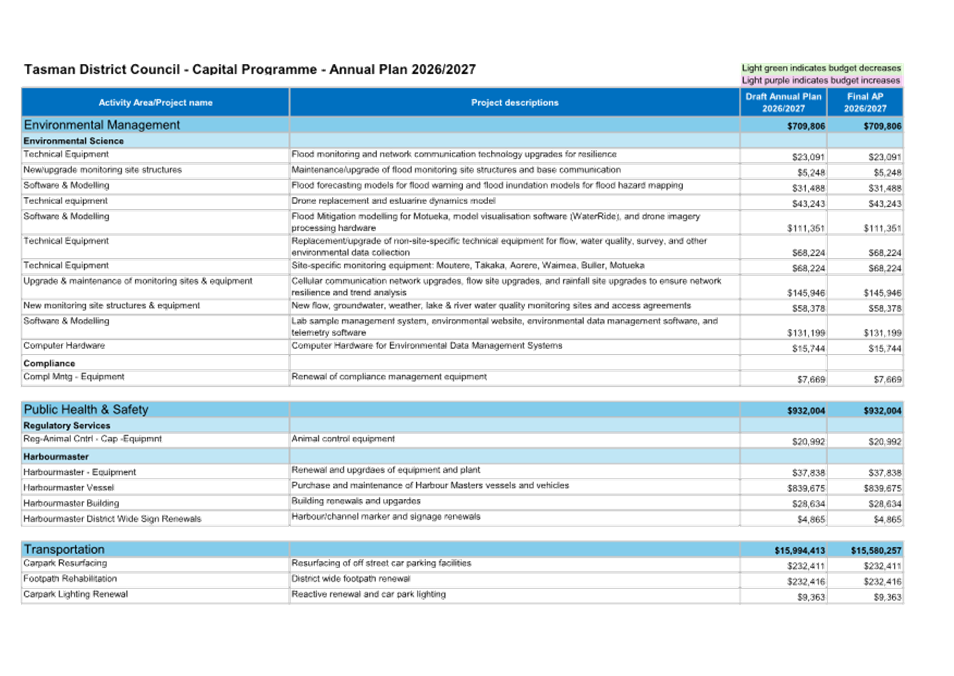

5.6 Changes to the proposed capital programme are shown in Attachment 1

and result in a net reduction of approximately $650k for 2026/2027. These

changes have resulted from:

5.6.1 Updated delivery forecasting:

Ongoing reforecasting of both the current year and Annual Plan year programmes

indicates that a number of projects will not be completed this year and have

been deferred into 2026/2027. This reduces costs in 2025/2026 but impacts the

Annual Plan capital programme. The most significant movements are:

5.6.1.1 River stopbank refurbishment

$3.2m (deferral of current year budget).

5.6.1.2 Tākaka wastewater

treatment plant compliance $1.57m (deferral of current year budget).

5.6.1.3 Redwood Valley water supply

compliance upgrades $2m (deferral of current year budget and budget forward

from 2027/2028).

5.6.1.4 Wai-iti Dam augmentation

pipeline $2.6m (deferral of current year budget and increase to enable land

purchase to complete the project).

There are a range of smaller

adjustments reflecting improved cost and timing information.

5.6.2 Three Waters phasing and

programme refinement: Initial detailed phasing work in Three Waters has been

applied to the Annual Plan, reducing the Three Waters capital programme from

$49.0m to $42.6m. Further reductions have been identified in residential green

space (-$148k) and tranche 3 of the river stopbank refurbishment (-$513k).

5.6.3 Asset renewals brought forward:

Condition assessments previously identified elevator component replacements for

the Council main building and Richmond Library were not needed in 2026/2027.

Recent failures and the increased risk of further outages mean these renewals

are now required earlier and have been added to the Annual Plan capital

programme ($260k).

5.6.4 The overall capital programme

was $98.0m and reduced by $10.2m once the capital lag was applied. The final

capital budget for 2026/2027 is $87.8m.

Further

savings to offset cost increases

5.7 Staff

have not included service reviews as an option to reduce costs because:

5.7.1 There is not sufficient time

before 1 July 2026 Annual Plan to undertake a review and further consultation

on any meaningful changes.

5.7.2 The Council runs lean and has

also been through three service and budget reviews in recent years. The Council

has very limited capacity to respond to further shocks and has exhausted our

ability to absorb any increases in operational costs for 2026/2027 without

major changes to the business.

5.7.3 The LTP 2027/2037 process is

underway, involves consideration by the Council of potential long-term changes,

and is already straining organisational capability.

5.8 Options for funding the overall

increases in costs and the impact of any submissions are discussed later in

this report.

Consultation summary

5.9 Public consultation on the Annual

Plan 2026/2027, including the draft Schedule of Fees and Charges, commenced on

2 April 2026 and closed 3 May 2027. The Submissions Hearing meeting was held on

14 May and 44 submitters were heard.

5.10 We received 367 submissions over the

consultation period including from 46 groups and organisations. We received

online submissions via the Shape Tasman engagement page, paper submission

forms, email submissions and written submissions.

5.11 We have prepared an overview of the

submissions (Attachment 2). All submissions can be viewed here: TDC Submissions.

5.12 Community views were also sought through two

quick polls on progressing or the community facilities projects and on the

proposed recovery rate. These were promoted via social media channels and

Antenno. We received 3,478 votes from 2,856 contributors.

5.13 The submission feedback regarding the

proposals in the consultation document has been summarised below.

2025 Weather Events Rating

5.14 The

consultation document presented four options for establishing a new rate to

fund the $14.6m recovery costs of the 2025 weather events:

5.14.1 Option 1: A targeted district-wide recovery

rate for five years to repay the costs of the 2025 weather events only, charged

as a uniform amount of $125. This was presented as the Council’s

preferred option

5.14.2 Option 2: A targeted district-wide recovery

rate for five years to repay the costs of the 2025 weather events only, charged

based on capital value.

5.14.3 Option 3: A targeted district-wide recovery

and resilience rate, charged as a uniform amount, to repay the initial weather

event costs and then continue as an ongoing fund for future natural hazard

events.

5.14.4 Option 4: A

targeted district-wide recovery and resilience rate, charged based on capital

value, to repay the initial weather event costs and then continue as an ongoing fund for future natural hazard events.

5.15 Council received 184 submissions on the proposed 2025 weather events

recovery rate, with submitters selecting an option as follows:

5.15.1 Option 1: 78 submissions (42%)

5.15.2 Option 2: 26 submissions (14%)

5.15.3 Option 3: 35 submissions (19%)

5.15.4 Option 4: 24 submissions (13%)

5.15.5 NA or none of the options: 21 (11%)

5.16 The

quick poll on the recovery rate options received 346 votes from 309

contributors as follows:

5.16.1 Option 1: 124 votes (36%)

5.16.2 Option 2: 83 votes (24%)

5.16.3 Option 3: 73 votes (21%)

5.16.4 Option 4: 66 votes (19%)

5.17 The

main themes across all submissions on the proposed recovery rate were:

5.17.1 Fairness and simplicity

5.17.2 Ability to pay and equity

5.17.3 Risk attribution and responsibility

5.17.4 Trust in council governance and financial

management

5.17.5 Time-limited recovery versus ongoing

resilience planning

5.18 Submitters

who preferred Options 1 and 3 generally supported equal treatment of

ratepayers. They considered that the benefits of disaster recovery are shared

across the district. Some also supported a time-limited rate rather than an

ongoing charge.

5.19 Several

submitters who preferred Options 1 and 3 said capital value is not a good

measure of a person’s ability to pay. In contrast, submitters who

preferred Options 2 and 4 considered that owners of higher-value properties are

generally better able to contribute more.

5.20 Some

submitters who preferred Option 2 felt that people not directly affected should

not be required to help fund the recovery. They also considered that those

living in higher-risk areas should meet more of the cost.

5.21 Several

submitters who preferred Options 3 and 4 said similar events are likely to

happen again and that an ongoing fund is needed to improve future preparedness

and response.

5.22 Some submitters across all options raised

concerns about Council’s financial management and whether money collected

for recovery and resilience would be used only for those purposes. Others said

the recovery costs should instead be met through Council savings, insurance, or

central government support.

5.23 A

small number of submitters suggested hybrid and other rating options,

including:

5.23.1 District-wide and targeted components; or

5.23.2 Capital value and uniform rate components;

or

5.23.3 Capital value with

a cap.

5.24 Submitter 35441 suggested that the establishment of

a dedicated extreme weather response fund as a joint Council and charitable

trust. A few submitters also raised concerns about the process used to

develop and consult on the recovery rate.

5.25 The main arguments raised by submitters reflect the

matters already considered by Council during workshops and meetings when the

consultation options and preferred option were developed. These issues have

already been weighed up by elected members as part of the decision-making

process.

5.26 The question of whether ratepayers in higher risk

areas of the District should bear all or a higher proportion of the costs for

funding was discussed during Annual Plan workshops. However, the idea of

hybrid rates was not discussed. At the 19 March 2026 meeting the Council made

decisions about its proposals in the Annual Plan. These included proposing a

targeted district-wide recovery rate for five years to repay the costs of the

2025 weather events only, charged as a uniform amount. The report stated three

other options that would be included in the consultation document. None of

these was a hybrid option.

5.27 If the Council was to introduce rating to fund the

2025 weather event which departs from the four options consulted on at this

stage in the process, it would open itself up to significant risk of legal

challenge. If the Council wants to introduce a hybrid rating model, it will

need to re-consult with the community on this new option.

5.28 Based on the number of submitters supporting each

option, the feedback received and its consistency with the Council’s

Financial Strategy, staff advise proceeding with Option 1: A targeted

district-wide recovery rate for five years to repay the costs of the 2025

weather events only, charged as a uniform amount of $125.

5.29 The Council should also critically evaluate the

concerns raised about the process used to introduce this rate and use that to

help improve future rating processes.

Operating budget movements

5.30 The consultation document invited feedback

on the proposed operating budget movements and 74 submitters responded to this

question. These views were overwhelmingly unsupportive or critical of the

proposals. Dominant concerns include the affordability of rates increases, a

perceived lack of cost control, rising debt and long-term financial

sustainability.

5.31 A small number of submitters accept the

increases as necessary, but question specific areas and delivery efficiency.

5.32 At least 17 submissions were explicitly

form-based and a further 11 submissions showing strong evidence of coordinated

or near identical content. These submissions raised criticism of the

consultation process, claims of misleading financial information and views

around fiscal discipline, debt reduction, and staff and consultant cost

scrutiny.

Community facilities projects

5.33 The consultation document invited feedback

on progressing or pausing the three community facilities projects. 288

submitters responded to this question and the quick polls received 3,132 votes.

5.34 There is strong overall support for

progressing community facilities, driven primarily by high levels of support

within the directly affected communities that viewed these facilities as

essential infrastructure, not “nice to haves”.

5.35 70 submitters explicitly did not support

council investment in community facilities projects at this time, or actively

seek to pause, defer, or cancel them. This feedback focused on cost-of-living

pressures and rates affordability, high and growing Council debt, ongoing

operational costs and “non‑essential” spending, and was often

framed at a district‑wide

level.

Tapawera Community Hub

5.36 48 submitters provide feedback on the

Tapawera Community Hub project. The quick poll received 630 votes from 523

contributors. 22% (140 votes) supported contributing with the Tapawera Hub and

78% (490 votes) wanted to pause this project.

5.37 There is strong support to progress the project and

that the hub will be well utilised. Pausing the project is viewed by supporters

as risking loss of external funding, continued exposure to safety and

resilience risks and rural inequity.

5.38 Opposition is limited and focussed on project

readiness, consultation quality, and community division. Some submitters argue

that existing facilities could instead be refurbished instead.

5.39 The submissions received and views of the

submitters that spoke at the hearing meeting reflect mixed views regarding

progressing or pausing the Tapawera Community Hub project. The feedback

indicates the importance of ensuring that any future investment is well aligned

with the needs, priorities, and capacity of the local community.

5.40 We will continue to work alongside the Tapawera

community to explore how best to support their ambitions for a Community Hub,

recognising the need to balance service provision with affordability and local

expectations. Staff advise pausing the Tapawera Community Hub project and

deferring it to LTP 2027-2037 discussions, as proposed.

Waimea South Facilities

5.41 43 submitters provided feedback on the Waimea South

facilities projects. The quick poll results are as follows:

5.41.1 Wakefield Hub: 953 votes from 714

contributors. 53% (509 votes) supported continuing with the Wakefield Hub and

47% (477 voters) wanted to pause this project.

5.41.2 Brightwater facilities upgrade: 559 votes

from 475 contributors. 27% (151 votes) supported continuing with the

Brightwater facilities upgrade and 73% (408 votes) wanted to pause this

project.

5.42 There is strong local support to progress these

projects and submitters noted that pausing now would impose higher future

costs, undermine community effort, and damage trust.

5.43 Submitters opposing or wanting this project paused

expressed affordability and debt concerns, and preferred refurbishment of

existing facilities. Submitter 35579 has concerns about the site location for

the Wakefield Hub including parking, SH6 access and flood risk.

5.44 The submissions emphasize the importance of the

Waimea South facilities projects for supporting community wellbeing,

strengthening local connections and providing fit-for-purposes spaces for

community activities. The concerns raised by some submitters regarding costs

and alternative options are also acknowledged. Staff advise continuing with the

Waimea South facilities projects, as proposed.

Motueka Pool

5.45 116 submitters provided feedback on the

Motueka Pool project and the quick poll received 990 votes from 835

contributors. 58% (574 votes) supported continuing with the Motueka Pool and

42% (416 votes) wanted to pause this project.

5.46 There is extensive support for progressing the

Motueka Pool; it is viewed as long overdue and essential for health, wellbeing

and safety. Equity of access was frequently raised and submitters noted pausing

the project would exacerbate inequity and undermine public trust and community

donations. Submissions from five iwi (35452, 35455, 35549, 35553 and 35598)

expressed strong support for progressing the Motueka Pool project.

5.47 Limited opposition to this project is

largely general rather than Motueka-specific, citing reasons like affordability

concerns, and competing priorities. The Motueka Youth Council (35355) does not

see the need, citing natural water options and Richmond access.

5.48 It is evident in the submissions received and the

views shared by submitters who spoke at the hearing meeting that the Motueka

Pool project is of long-standing and considered to be essential local

infrastructure that will provide health, safety and social benefits to all of

the local community. The Council discussed this project at a confidential

workshop on 27 May 2026. Staff advise continuing the Motueka Pool project

through the design phase, as proposed.

Changes to the capital programme

5.49 The consultation document invited feedback

on the proposed changes to the capital programme. 91 submitters responded to

this question, 21 of whom provided no comments.

5.50 There is limited support for the capital

programme as a whole, but conditional support for selected high‑value or urgent projects

especially in essential infrastructure or specific community facilities. The

main sentiment is that the capital programme is too expansive for current

economic conditions, lacks clear prioritisation and inadequately demonstrates affordability,

necessity, and deliverability. Many submitters are asking Council to slow down,

narrow focus, improve transparency and better justify trade‑offs.

5.51 Changes to the proposed capital programme 2026/2027

are discussed in paragraph 0 and shown in Attachment 1.

Slowing planned funding of depreciation

for roading assets

5.52 The consultation document invited feedback

on the proposed slowing of planned funding of depreciation for roading assets.

91 submitters responded to this question, 22 of whom provided no comments.

There was broad consensus that roading is a core council function, but

disagreement on whether slowing depreciation is an acceptable mechanism for

managing current fiscal pressure.

5.53 Supportive submitters emphasised short‑term financial relief, economic context and/or the view that

depreciation is largely an accounting construct that can be adjusted without

impacting service delivery. Submitters opposing or arguing against deferred

funding of depreciation stressed intergenerational equity and viewed it as

short‑term budget optics that undermines asset integrity, increases debt,

and unfairly shifts costs to future ratepayers by “kicking the can down

the road”.

5.54 The Council began a programme to fully fund

depreciation in July 2015. The original goal in the LTP 2015-2025 was to

achieve this by June 2025. Subsequent LTPs and Annual Plans have extended the

timeframe, and full funding of depreciation is now planned for June 2030.

Extending the timeframe reduces rates in the short term but increases the

Council’s debt. The Department of Internal Affairs does not require

councils to fully fund depreciation by a specific date; Audit New Zealand is

satisfied as long as the Council continues to make progress.

5.55 By June 2028, all activities except Roading will

have depreciation fully funded. Recent high inflation has significantly

increased asset valuations and therefore depreciation costs, which has

contributed to pushing out the target date. By pushing out the target date it

has meant the Council can reduce the annual increase in rates.

5.56 The decision to aim for full funding by June 2030

was confirmed in the 2024–2034 LTP to help keep rates at manageable

levels. The Council considers this approach a prudent balance between rates

affordability and long term financial sustainability.

5.57 Feedback from submitters, both supportive and

opposed, has been noted and will inform deliberations for the LTP

2027–2037.

Changes to the Council’s fees and

charges

5.58 The consultation document invited feedback

on the proposed changes to Council’s fees and charges for 2026/2027. 115

submitters responded to this question, 17 of whom said ‘no’.

5.59 Seven submitters support the proposed increases to

fees and charges. Opposition to the proposed increases is widespread and

strongly expressed, especially where increases exceed inflation. There is

qualified support for user‑pays, but only where the costs are transparent and charges are

clearly justified and cost reflective. Submitter 35473 advocates further

increasing cost recovery levels (~10%).

5.60 Trust and transparency are key issues and

many submitters are not convinced fees reflect real costs or do not have

confidence in the fee-setting process. Contentious issues included the level of

increases, charges for accessing Council-held information particularly property

files, and perceived Council inefficiencies driving costs. Suggested

alternatives included tiered pricing systems, hourly or proportional charging

and flexible bulk pricing.

5.61 Twelve submitters provided feedback on the proposed

changes to how property file fees are charged. Submissions were received from

both individual property owners and bulk users. Property owners opposed the

introduction of a $30 fee to access their property files, stating that this

information has already been paid for through rates and they should not be

charged for access to their own information. Bulk users opposed the proposed

$3,000 fee for access to 60 files. They considered the 60-file threshold to be

arbitrary and the increase too large for real estate companies, and suggested a

more gradual increase. They also requested tiered pricing by volume access for

bulk users, and investment in digital access to property files.

5.62 Staff have considered the feedback and provide the

following changes to the proposed fee structure for property files for the

Council’s consideration:

5.62.1 charging individual property owners $25 per

property file, noting that preparing a file typically requires 30–60

minutes of staff time and that this approach helps reduce the burden on rates

by supporting a user-pays model.

5.62.2 retaining the proposed ‘pay as you

go’ charge of $60 per file.

5.62.3 In response to feedback on bulk user

charges, staff do not recommend proceeding with the proposed $3,000 fee for 60

files (equivalent to $50 per file). Instead, staff recommend a flat rate of $40

per file for bulk users. This would ensure all bulk users are charged a

consistent discounted rate, addressing inequities in the current annual fee of

$2,750 for unlimited access to files, where some users effectively pay around

$40 per file while others pay as little as $4 per file due to higher volumes.

5.63 One

submitter commented on the proposed increase to the bulk water take fee,

requesting a lower rate for bulk potable delivery operators compared to other

commercial users, as they supply water to rural homes. They also compared the

charge to those set by regional councils. The Council seeks to balance cost

recovery, fairness between users, and minimising impacts on the wider ratepayer

base. Bulk water charges reflect the infrastructure costs required to deliver

the service and are consistent with a user-pays approach, regardless of user

type. Staff advise retaining the proposed bulk water take charge.

5.64 Four submitters commented on the Project

Information Memorandum (PIM) fee increase. Views were mixed, with two

supporting a user‑pays approach and no rates subsidy, and two opposing the size of the

increase. Submitters that opposed suggested differential fees for project sizes

or amount of staff time needed. The increase in PIM fee this year is a step

towards user pays and has been calculated on the average time spent. PIMs for

consent‑exempt small dwellings may require more assessment, but there is

currently insufficient data to support differential fees. A single standard fee

provides transparency and simplicity during the implementation of the new

regulatory setting. Staff advise retaining the proposed PIM fees.

5.65 Seven submissions raised concerns about dog fees including cost, how

the three categories are set, and the level of fees for working dogs, with some

suggesting a cap of five dogs. Dog registration fees were not proposed to

change. The three categories are based on property size to reflect that dogs on

larger properties generally require fewer council resources. The ‘working

dog’ fee is set at 55% of the ‘category 1’ fee, which staff

consider reflects the level of control work required. A cap of five

working dogs was considered; however, any reduction in fees would need to be

offset by increasing charges for other dog owners to maintain overall cost

recovery.

5.66 Staff advise retaining the proposed fees for Animal Control. The

Dog Control Act 1996 (s.37[6]) requires that the Council publicly notify the

Dog Control fees fixed for the registration year, in a newspaper circulating in

the District, at least once during the month preceding the start of every

registration year. In addition, pound fees are required to be adopted at least

14 days before the resolution comes into effect and be publicly notified in a

newspaper circulating in the District.

5.67 To enable us to meet these notification requirements, this report

includes a resolution to adopt the Dog Control fees set out in Attachment 3

at this meeting. The remainder of the schedule of fees and charges will be

presented for adoption at the 25 June 2026 Council meeting.

Other matters raised in submissions

5.68 Affordability was a dominant concern,

particularly for households already experiencing cost pressures (food, fuel,

insurance, housing) and with limited capacity to absorb further increases in

rates or fees. Staff acknowledge these concerns and that efforts address the

Council’s financial and economic challenges are

occurring in the same context of financial pressure being experienced by the

community. In developing the proposed Annual Plan, the Council sought to

balance affordability with the need to maintain current services levels and

business operations.

5.69 Some submitters expressed concern about the

level of detail provided in the consultation document and supporting material,

noting the information was unclear, potentially misleading, or lacked

visibility of underlying cost drivers. The feedback received is acknowledged

and staff consider the information provided was appropriate for an Annual Plan

consultation (as opposed to more detailed information for a LTP consultation); there is an inherent challenge in balancing sufficient detail with

accessible information that supports public engagement.

Requests received from submitters

The Motueka

Heritage Wharf

5.70 The Heritage Wharf Restoration Group (35396)

is seeking funding of $60,000 to assist with the re-construction of the Motueka

Heritage Wharf, which is a significant Council historical structure.

5.71 The Council was updated on the Group’s

proposal and presented with its business case for the restoration work and

associated funding request at the Environment, Regulatory and Operations

Committee meeting on 12 May. The project and funding options were discussed but

no decision was made and the matter is to be covered at this meeting.

5.72 At its meeting on 19 May, the Motueka

Community Board also discussed the project and indicated in-principle support

to allocate funding from its 2025/2026 Special Projects Fund. Staff will

present a report at the next Board meeting on 16 June.

5.73 Staff advise that Motueka Reserve Facilities

Contributions are already allocated to other projects, including the Motueka

Pool. Council may wish to allocate capital budget to this request but, given

the indicative funding support from the Motueka Community Board, this is not

recommended by staff as funding is not currently included in the Annual Plan

budgets.

Motueka Community Board

5.74 The Motueka

Community Board (35426) makes a range of requests to the Council, listed below

along with staff advice:

5.74.1 Motueka Beautification and Public Spaces:

Request that the Motueka High Street upgrade identified in the LTP 2021-2031 be

reinstated in future planning, particularly following the removal of several

Golden Elm trees.

5.74.2 This would be a matter for Council. At

present, there has been no indication from the Mayor and Councillors to include

a project of this nature in the next LTP, and it would likely be challenging to

accommodate given current financial constraints.

5.74.3 Road safety review: Requests that a safety

review be undertaken for the intersection of King Edward Street, College

Street, and Queen Victoria Street.

5.74.4 Staff will revisit this intersection,

noting that a range of measures have previously been implemented to improve

signage and visibility. More substantive safety improvements would likely

require a full upgrade, such as a roundabout, and this is estimated to cost up

to $1m and require land purchase. At this stage, it is unclear whether there is

capacity within the LTP and Council’s financial constraints to

accommodate a project of this scale

5.74.5 Coastal Protection Investigation: Requests

that Council investigate the coastal rock wall protection along the Motueka

ward foreshore.

5.74.6 The Council’s Coastal Assets activity

does not have records of significant coastal rock protection infrastructure

along the Motueka ward foreshore, other than the wall at Marahau. Existing

coastal rock protection features will need to be identified and investigated on

a case-by-case basis to determine history, ownership, and maintenance

responsibility. Staff note there is informal fill/erosion protection along the

coastline, including in some road reserve. These will continue to be monitored

to ensure that the road and cycle trail network are not adversely affected by

coastal erosion.

5.74.7 Motueka Library Big Meeting Room: Mitigate

the challenges of the library meeting room with IT issues and lack of sound.

Investigate set up of microphones and adequate speaker system.

5.74.8 Staff agree with the Board’s concerns

and will investigate the matters raised.

5.74.9 Motueka Historical Wharf Restoration: The

Motueka Community Board requests that Tasman District Council endorse the

Motueka Historical Wharf Restoration in principle. The Board acknowledge

current funding constraints may limit direct support.

5.74.10 Stormwater: Prioritise improvements to stormwater

resilience, including consideration of a modern automated gate at Thorp Drain

similar to Woodlands Drain. Target known problem areas such as Woodlands

Avenue, and review drainage limitations from Wratt Street through to Monahan

Street, including additional soak pits where appropriate.

5.74.11 Staff advise that replacement of the Thorp Drain tide

gate is under consideration, alongside related work Woodlands Drain tide gate

near the Recreation Centre. Minor improvements for Woodlands Avenue are being

priced, however capacity in this area is very limited due to low ground levels.

In addition, high groundwater levels mean soakage solutions may not be

effective for the design storm events.

5.74.12 Motueka i-SITE: Support the continued operation of the

Motueka i-SITE as a key asset for the district’s growing visitor economy.

Request that Council maintain its annual contribution to preserve current

service levels, staffing, and opening hours.

5.74.13 Staff advise that the annual contribution to the

i-SITE has been allocated in the Annual Plan budget.

5.74.14 Wallace Street: Advocate for pedestrianisation of

Wallace Street, from the High Street end to the Decks Reserve car park

entrance, creating a plaza-style public space similar to Sundial Square in

Richmond and upper Trafalgar Street in Nelson.

5.74.15 Staff consider that this proposal would best be

contemplated as part of a town centre upgrade project, as requested above by

the Board.

5.74.16 Rivers: Review flood protection measures for the

Little Sydney stream including Factory Road, Swamp Road and Umukuri Road

catchment extending from Brooklyn, also the Dehra Doon catchment and the

Riuwaka River to better protect residents and productive land.

5.74.17 There is currently no flood protection level of

service for the Little Sydney stream and associated drains around the Factory

Road, Swamp Road, and Umukuri Road areas, other than the benefit received from

the Lower Motueka and Riuwaka stopbank systems. However, a scheme-plan for this

area has been prepared in the past (1972) and it is the intention of staff to

revisit this plan and develop improvement options for this area.

5.74.18 Otuwhero and Marahau Rivers Catchments: There is no

River Management Plan for the Marahau/Otuwhero catchments, which needs to be

addressed. Coastal, inlet and land use (forestry) issues for the area

similarly.

5.74.19 Council does not provide any river management level of

service to the Otuwhero and Marahau Rivers; there is no River X or River Y

rating area at these locations and Council provides no active river management

service in unmanaged/River Z areas. However, staff have initiated a

comprehensive review of the current river rating system, which will include an

assessment of existing unrated areas like Otuwhero and Marahau, to see if the

current system is fit for purpose and to provide greater clarity around river

management levels of service. Our Catchments and Land Use team can work with

landowners in these catchments to improve river and land management over time.

5.74.20 Memorial Park Reserve Management Plan: Request that

this Reserve Management Plan be reviewed in the coming 2026-2027 year. The

previous review for Memorial Park occurred in 1997 and is a high priority. The

Motueka Ward Reserves Plan was reviewed in 2019 but the Memorial Park Reserve

was not included.

5.74.21 Staff advise that the review of the Memorial Park

Management Plan is scheduled to begin in 2027/2028, with no capacity to bring

this work forward into the already committed 2026/2027 work programme.

5.75 Submitter

35571 provides a wide range of recommended actions for the Council to consider

for 2026/2027, including requests marked as priority by the submitter. These

matters are covered in the Motueka Community Board requests above.

Eighty Eight Valley Water

Scheme

5.76 The

Eighty Eight Valley Rural Water Supply Committee (35505) suggests

a tiered rating system for users of this scheme, when the scheme joins the

urban water club. This would be a departure from the rating for similar urban

extensions. The submission argues that:

5.76.1 Rural users of the scheme have additional

infrastructure costs not provided by the Council (e.g. tanks and pipework).

5.76.2 Existing users have sought to retain the

rural stockwater scheme rather than become part of the urban reticulation but

the Council has made other decisions.

5.76.3 Holders of larger numbers of units are

required to use highly treated potable water for their stockwater and other

non-potable rural needs.

5.76.4 Holders of larger numbers of units will

likely relinquish some of their units because of cost increases.

5.76.5 Users have already paid for the existing

reticulation (some through helping to install the scheme, unpaid in 1981) and

installed internal reticulation on their farms and properties which require

upgrades if their source of water is changed

5.77 During the 2027/2028 year the Eighty Eight Valley water scheme will

be split into two parts:

5.77.1 Lower part – north of Totara View

water tanks will effectively become an urban extension receiving treated water

from the Wakefield urban supply.

5.77.2 Upper part – Parkes Stream to Totara

View will effectively become stock water with staff investigating

different models for its ongoing operation.

5.78 Staff consider that many of the arguments being

advanced are valid and are concerned that applying the full urban extension

charges will result in some (more) users leaving the scheme and the number of

units others use being reduced. This in turn will increase the costs to those

in the water club.

5.79 Staff support in general terms adopting a rating

schedule based on percentages of the urban metered charge for the Eighty Eight

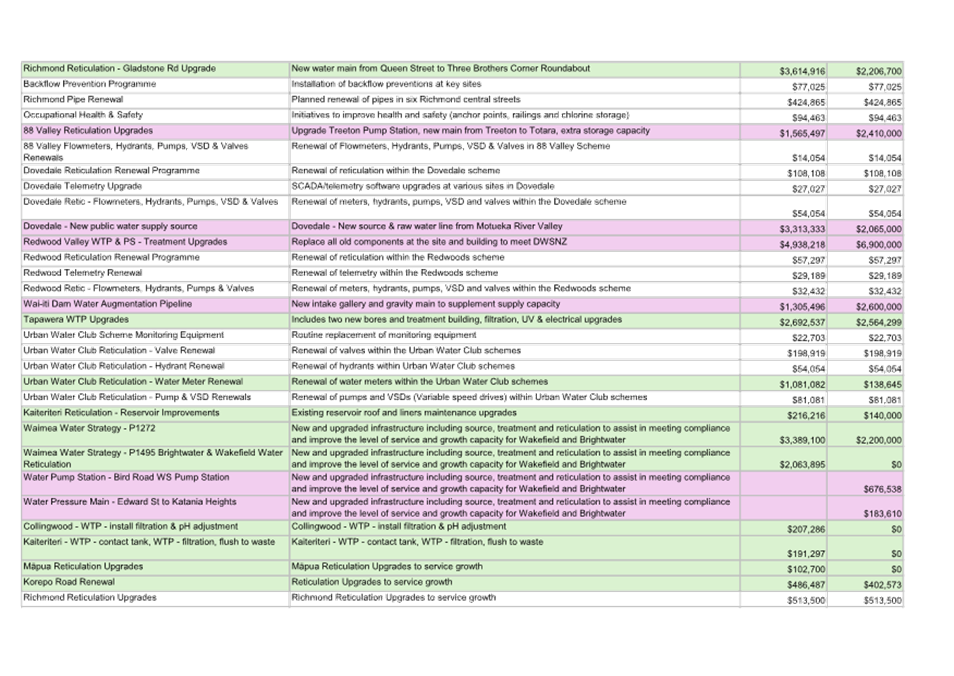

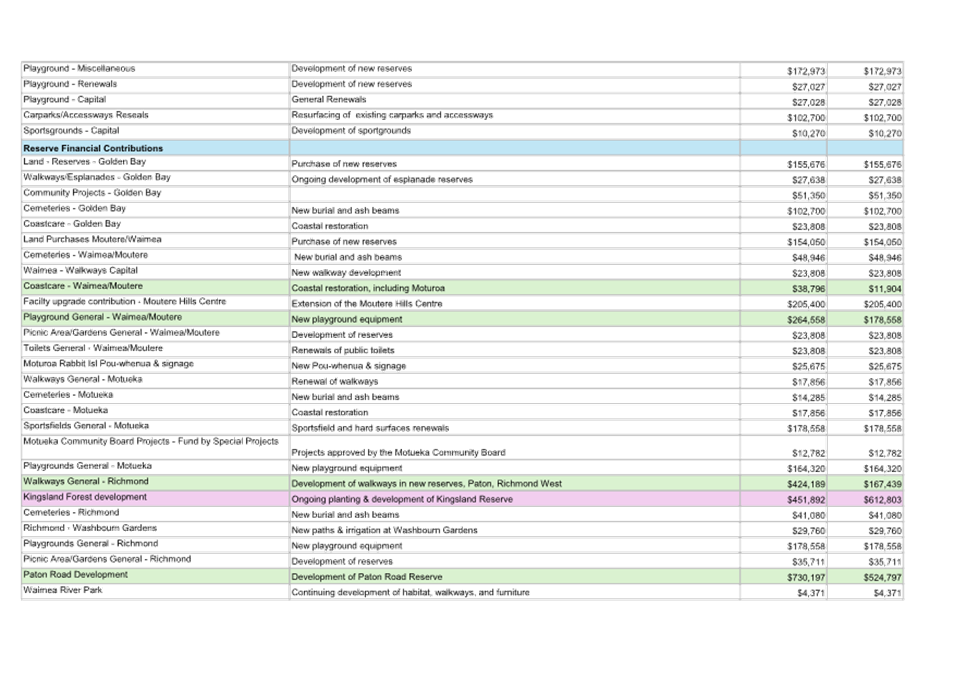

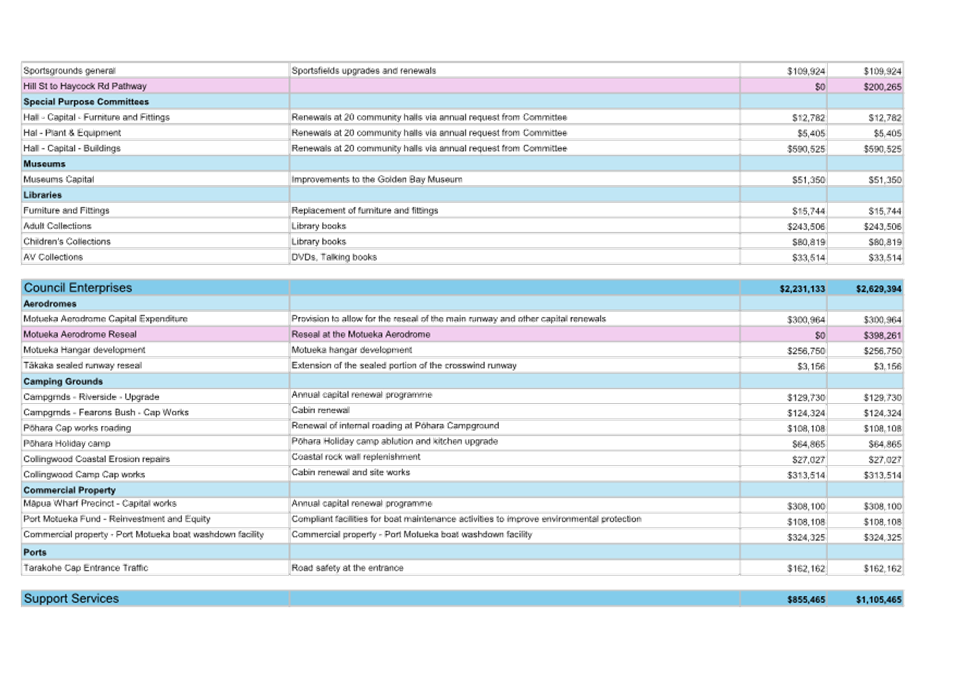

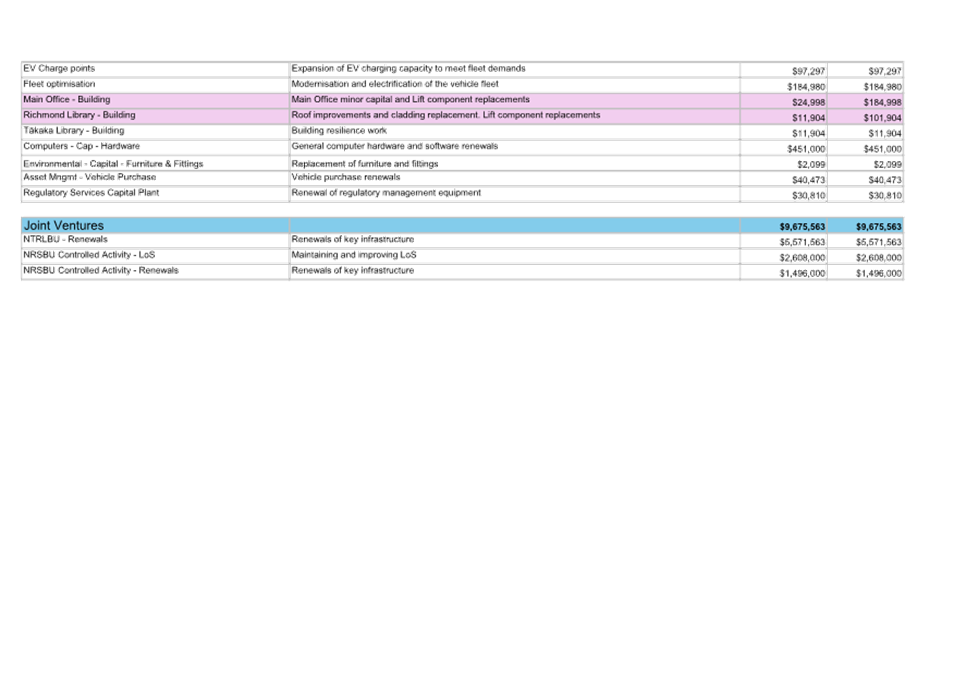

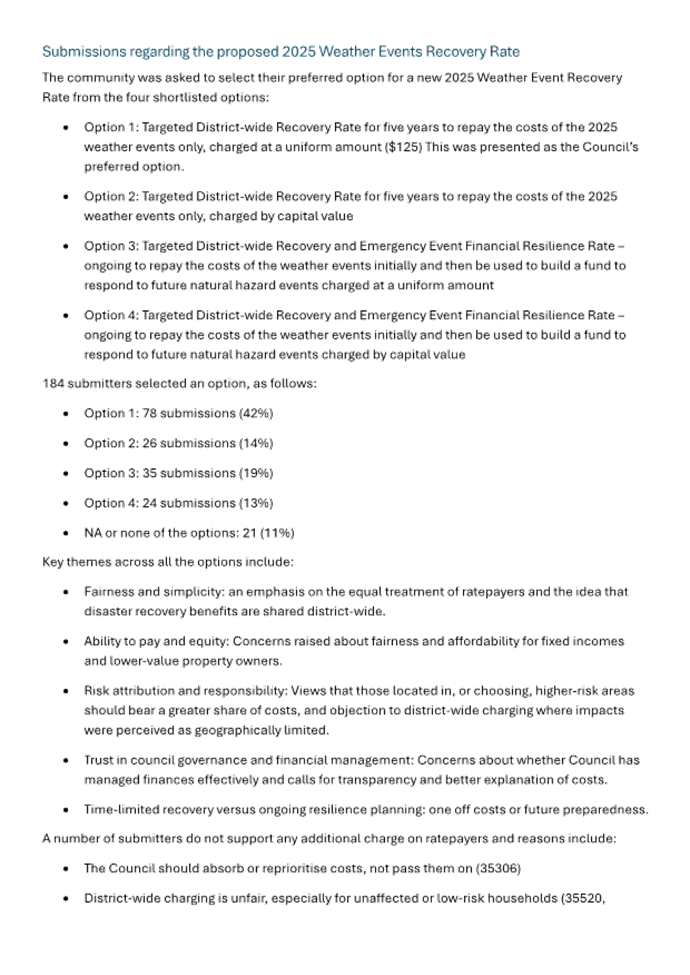

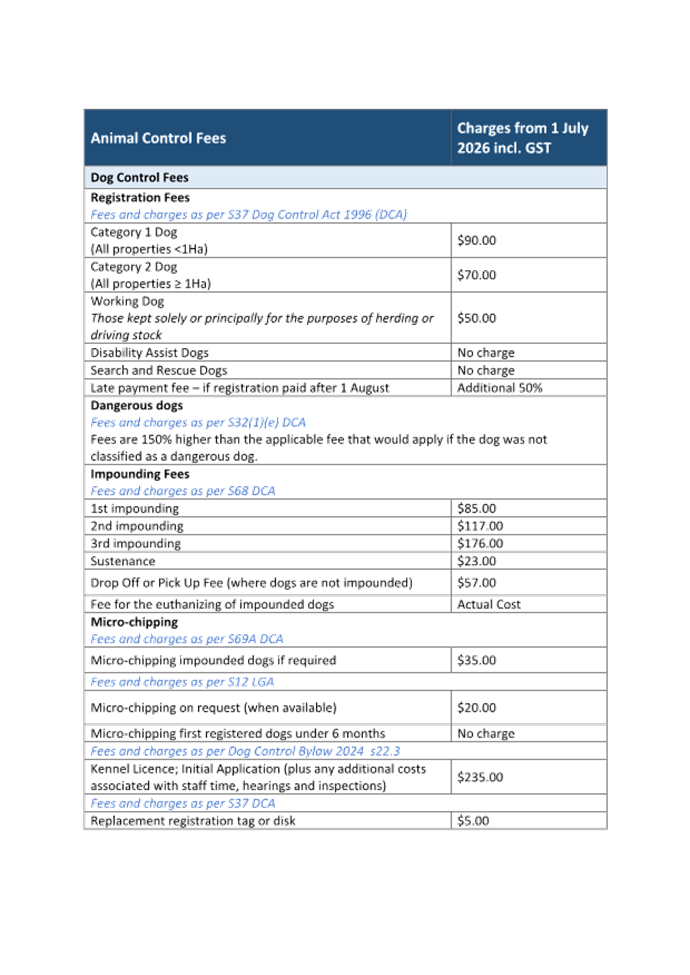

Valley Scheme and seek an indication today from elected members about