Notice

is given that an ordinary meeting of the Strategy Finance and Performance

Committee will be held on:

|

Date:

Time:

Meeting

Room:

Venue:

YouTube Link

|

Thursday 19 March 2026

9.30am

Tasman Council Chamber

189 Queen Street, Richmond

Tasman District Council - YouTube

|

|

Strategy

Finance and Performance Committee

Komiti

Rautaki me te Kaupapahere

AGENDA

|

MEMBERSHIP

|

Chairperson

|

Cr K Maling

|

|

|

Deputy

Chairperson

|

Cr D Woods

|

|

|

Members

|

Mayor T King

|

Cr M

Kininmonth

|

|

|

Cr C Butler

|

Deputy Mayor B

Maru

|

|

|

Cr J Ellis

|

Cr D McNamara

|

|

|

Cr K

Ferneyhough

|

Cr P Morgan

|

|

|

Cr M Greening

|

Cr T Neubauer

|

|

|

Cr J Gully

|

Cr T Walker

|

|

|

Cr M Hume

|

|

|

(Quorum 8 members)

|

|

Contact Telephone: 03 543 8400

Email: tdc.governance@tasman.govt.nz

Website:

www.tasman.govt.nz

|

Strategy Finance and

Performance Committee Agenda – 19 March 2026

AGENDA

1 Opening, Welcome, KARAKIA

2 Apologies

and Leave of Absence

|

Recommendation

That the apology

from Councillor D Woods be accepted.

|

3 Public

Forum

Nil

4 Declarations

of Interest

5 LATE

ITEMS

6 Confirmation

of minutes

|

That the minutes of

the Strategy Finance and Performance Committee meeting held on Thursday, 19

February 2026, be confirmed as a true and correct record of the meeting.

|

|

That the confidential

minutes of the Strategy Finance and Performance Committee meeting held on

Thursday, 19 February 2026, be confirmed as a true and correct record of the

meeting.

|

7 Reports

7.1 Presentation by Mr Tim Cadogan from Taumata

Arowai........................................ 4

7.2 Financial Report....................................................................................................... 5

7.3 Long-Term Plan Assumption - Population

Projection........................................... 17

7.4 Adoption of Tasman Inundation Practice Note...................................................... 64

7.5 Six-Month Performance Measure Progress

Report 2025/2026.......................... 132

7.6 Chair's Report...................................................................................................... 163

8 Confidential

Session

8.1 Procedural

motion to exclude the public............................................................. 165

8.2 Community Occupancy Policy - Financial

implications....................................... 165

9 CLOSING

KARAKIA

Strategy Finance and

Performance Committee Agenda – 19 March 2026

7 Reports

7.1

Presentation by Mr

Tim Cadogan from Taumata Arowai

|

Report

To:

|

Strategy

Finance and Performance Committee

|

|

Meeting

Date:

|

19

March 2026

|

|

Report

Number:

|

RSFP26-03-5

|

1. Presentation

/ Whakatakotoranga

Mr Tim Cadogan from Taumata Arowai will

make a presentation to the Strategy Finance and Performance Committee on Water

101. Mr Cadogan is the Engagement Specialist with

Taumata Arowai and a former Mayor of Central Otago District Council.

He has been presenting “Water

101” to several councils throughout New Zealand.

Nil

Strategy Finance and

Performance Committee Agenda – 19 March 2026

7.2 Financial Report

Information Only - No Decision

Required

|

Report

To:

|

Strategy

Finance and Performance Committee

|

|

Meeting

Date:

|

19

March 2026

|

|

Report

Author:

|

Paul

Egan, Management Accounting Manager

|

|

Report

Authorisers:

|

Sue

McLean, Group Manager - Strategy & Finance; Matthew McGlinchey, Financial

Strategy & Planning Manager

|

|

Report

Number:

|

RSFP26-03-6

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 This

report provides an update on key financial results for the seven months ended

31 January 2026.

1.2 The

report also outlines recent trends in the balanced budget benchmark, capital

expenditure, and maintenance expenditure.

1.3 Section

9 responds to questions raised in the equivalent report considered on 19

February 2026. Staff remain open to making further refinements where possible,

noting that system limitations may restrict some changes.

1.4 Overall,

financial results continue to track consistently with the position reported to

the Committee at its meeting on 19 February 2026.

1.5 Key

point updates are summarised below:

1.5.1 Severe weather events continue to have a material impact on

the Council’s financial position. As at 31 January 2026, operating

expenditure related to these events totalled $25.3 million, of which $23.0

million has been classified as maintenance. This excludes staff time. A

separate report is being prepared for the Information‑Only Council

meeting on 28 April 2026, which will provide an update on the emergency events,

including financial and insurance matters.

1.5.2 Net debt has increased $23.8 million since 30 June 2025,

largely reflecting expenditure associated with the severe weather events.

1.5.3 Capital expenditure year to date is $29.7 million,

representing 31% of budget.

1.5.4 Additional maintenance and operations costs are expected in the

Three Waters activities. This has previously been reported to the

Information Forum of 11 February 2026, with further reporting on

reactive maintenance and renewals scheduled for the Full Council meeting on 7

May 2026.

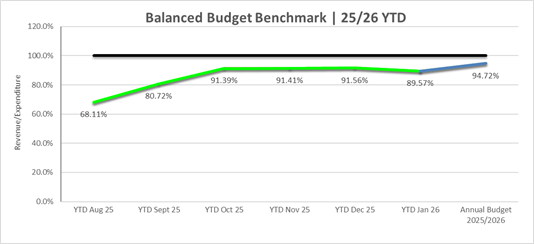

1.5.5 The balanced budget benchmark was 89.6% as at 31 January

2026, compared with a budgeted position of 94.72%.

1.5.6 No material insurance recoveries, relating to the emergency

event, had been recognised as income as at 31 January 2026.

2. Recommendation/s

/ Ngā Tūtohunga

That the Strategy

Finance and Performance Committee

1. receives the Financial Report Year to Date January 2026 report RSFP26-03-6.

3. Balanced

Budget Benchmark

3.1 The

balanced budget benchmark is a prescribed measure used to assess the operating

performance of local authorities. It is used in preference to a traditional

“profit and loss” measure because local government financial

statements include a range of revenue items that are capital, one‑off, or

non‑controllable in nature, which can obscure the Council’s

underlying operating position.

3.2 The

benchmark forms part of the suite of prudence measures set out in the Local

Government (Financial Reporting and Prudence) Regulations 2014 and is reported

alongside other benchmarks in the Council’s statutory planning and

reporting documents. Consistent with the Council’s Financial Strategy,

the benchmark is intended to be considered over the medium to long term, rather

than as a point‑in‑time target, acknowledging that temporary

deviations may occur due to timing effects, significant capital programmes, or

exceptional events

3.3 The

benchmark indicates the extent to which operating expenditure is funded

from operating revenue after excluding items that do not relate to core

operations, such as development contributions and revaluation movements. It

should be read in conjunction with the full financial results, cashflow

position, and debt measures to provide a balanced view of the Council’s

financial sustainability.

Chart 1 | YTD Balanced Budget

Benchmark

3.4 The

year‑to‑date balanced budget benchmark is 89.57%, representing a

slight decline from the position reported previously.

3.5 The balanced

budget benchmark has been below 100% in several recent years. In some years,

this position is also budgeted, reflecting deliberate funding decisions that

are consistent with the Council’s Financial Strategy. These include

instances where operating expenditure is funded from sources other than

operating revenue, such as:

3.5.1 Loan funded Operating Expenses, primarily related to:

· Contributions

to assets of Saxton Fields facilities, where the asset is constructed on land

owned by Nelson City Council and recorded as an asset of Nelson City

Council. While the expenditure contributes to long‑lived assets,

the accounting treatment for Tasman District Council is as a grant or

contribution, as the Council does not own the assets.

· Expenditure

on the Tasman District Council Digital Innovation Programme, which is largely

classified as operating expenditure due to cloud‑based accounting

treatment requirements

· Expenditure

on the Tasman Resource Management Plan.

· A grant

contribution towards the new ARC facility

· Decisions to

not fully fund depreciation in a given year, consistent with adopted funding

and affordability settings

3.5.2 The

use of Reserves, representing surplus funds carried forward from prior years to

be used on expenditure in the current year.

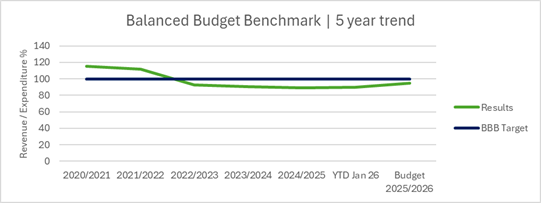

3.6 To

provide context and illustrate recent trends, the chart below presents the

balanced budget benchmark as reported in the most recent Annual Report, updated

to include year‑to‑date actuals and the current year budget.

3.7 The

chart is presented on a consolidated basis and includes year‑end

adjustments relating to the Council’s share of joint ventures and joint

operations up to 24/25.

Chart 2 |

Balanced Budget Benchmark – Comparison to Prior Years

3.8 The Council’s

year‑to‑date balanced budget benchmark is a provisional position

and does not include year‑end adjustments associated with joint ventures

and joint operations. In the previous two financial years, the inclusion of

these adjustments at year end did not result in a material change to the

benchmark outcome.

3.9 The most

likely factor that may improve the final year‑end benchmark position is

the reclassification of certain unplanned repair expenditure arising from

severe weather events to unplanned capital expenditure, following the

completion of impairment testing. Any such adjustments will be reflected in the

year‑end financial statements.

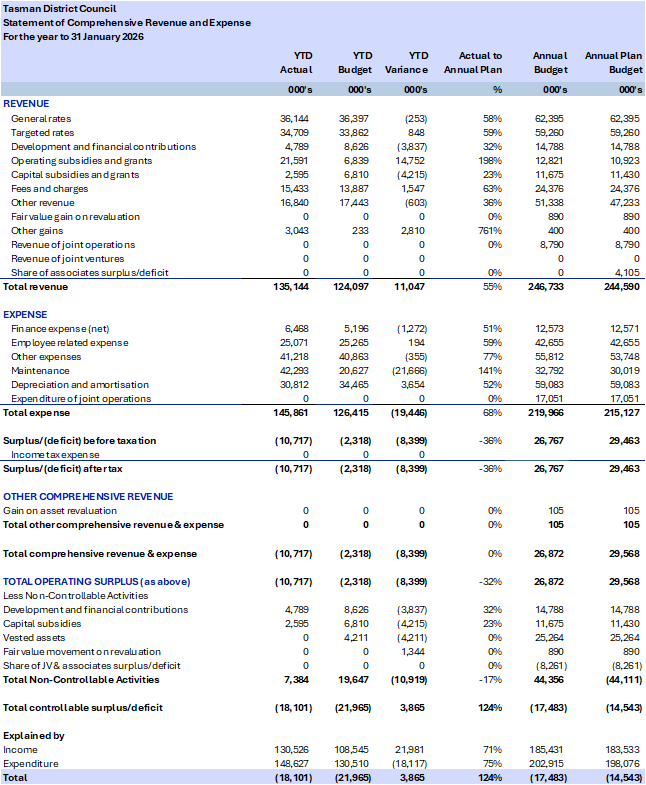

4.1 Table 1 | Statement of

Comprehensive Revenue and Expense

Development and financial contributions

4.2 Development

and financial contributions, which largely support future growth, continue to

track below the year‑to‑date (YTD) budget by $3.8 million. This

variance reflects the impact of current economic conditions on development

activity.

Operating subsidies and grants

4.3 Operating

subsidies and grants are $14.8 million above the YTD budget and exceed the

full-year budget of $6.8 million. This increase is primarily driven by

additional funding from government agencies, including Waka Kotahi, MBIE, and

MfE, largely in response to the severe weather events. The majority of this

variance reflects accounting accruals rather than cash received to date.

Capital Subsidies

4.4 Capital

subsidies are $4.2 million below the YTD budget. This variance reflects delays

in MBIE-funded Lower Motueka River works and disruptions to planned roading

projects, and thus the Waka Kotahi subsidy, caused by weather events.

Fees and charges

4.5 Fees

and charges are tracking at 63% of the annual budget at $1.5 million ahead of

YTD budget. This is driven by Resource Consents, Solid Waste and Industrial

water supply exceeding budget. There are also timing impacts from areas

where there are annual charges that have been billed for the year in

Environmental Services.

4.6 While

some areas are tracking above YTD budget, many have a seasonal or annual aspect

to their income, and it cannot be assumed that this favourable variance will

continue to grow.

Other Gains

4.7 Other

gains relate to the sale of ETS credits ($3.0 million), approved by the Council

after the adoption of the annual plan 2025/2026.

Finance Expense (net)

4.8 Net

finance expenses are at 51% of full year budget at 58.3% of the way through the

year. Some joint venture related interest costs are expected and budgeted at

end of financial year.

Employee related expense

4.9 Employee

costs are aligned with budget expectations as at 31 January 2026. Senior

management continue to actively manage staffing levels and the timing of

vacancy appointments.

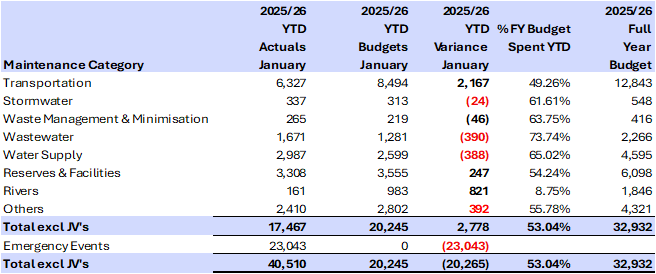

Maintenance expense

4.10 For

reporting clarity, this report separates routine operational maintenance from

emergency event‑related costs (refer Table 2).

4.11 Emergency maintenance expenditure to date totals $23.0 million. The

externally funded component of this expenditure is still being finalised, as

confirmation of amounts is taking time, particularly where multiple external

funders are contributing to the same affected assets. In the interim, the

unfunded balance is being financed through debt. Net recovery of these costs is

planned through the proposed recovery rate.

4.12 Excluding

weather-related activity, maintenance expenditure remains below budget and is

expected to continue to do so. Water Supply and Wastewater activities, however,

continue to experience elevated reactive maintenance costs and are forecast to

exceed their respective budgets. Reactive

maintenance budgets have been increased in the 2026/2027 draft Annual Plan to

maintain asset value and service performance.

4.13  Table 2 | Maintenance Expenses

Table 2 | Maintenance Expenses

5.1 The

capital works programme is developed using a planning assumption that, on

average, around 10% of approved capital projects are not fully delivered within

a financial year. This reflects the inherent uncertainty in large and complex

capital programmes, including consent timing, procurement, weather, and

external dependencies. This assumption reduces the level of forecast borrowing

required and, in turn, limits debt servicing costs and the need to set rates to

fund borrowing that may not ultimately be drawn

5.2 Year‑to‑date capital expenditure totals $29.7

million against a planned budget of $95.6 million, representing 31% of the full‑year

budget. As part of normal capital programme management, staff are reviewing

project sequencing and priorities within the current year programme to develop

a refined reforecast and a more accurate spend profile. In parallel, a

technical review of emergency‑related expenditure is underway, which may

result in some costs currently recorded as maintenance being reclassified as

capital expenditure following impairment assessment. Any updated forecasts will

be reported to the Committee in a future financial update

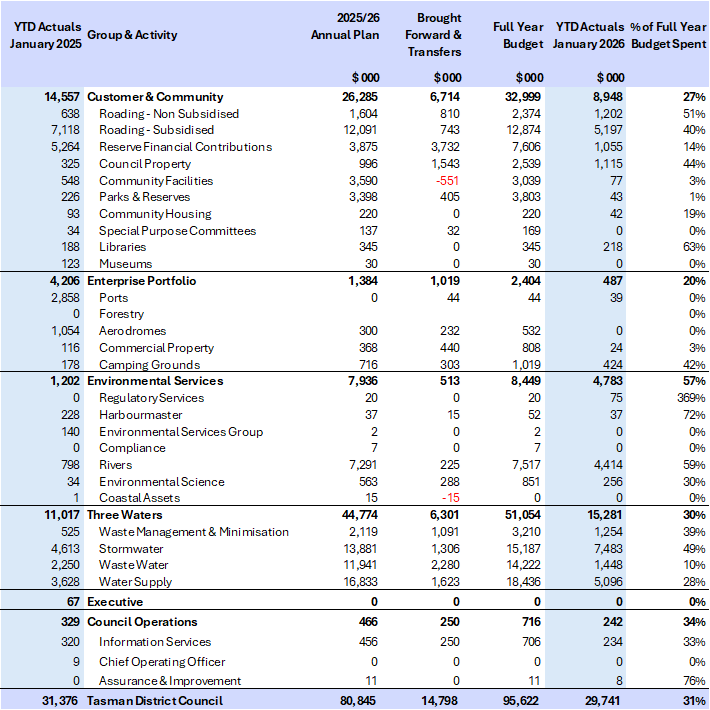

5.3 A summary of the budget, actual spend by

activity is provided in Table 3.

Table 3 | Capital Expenditure

Table 3 | Capital Expenditure

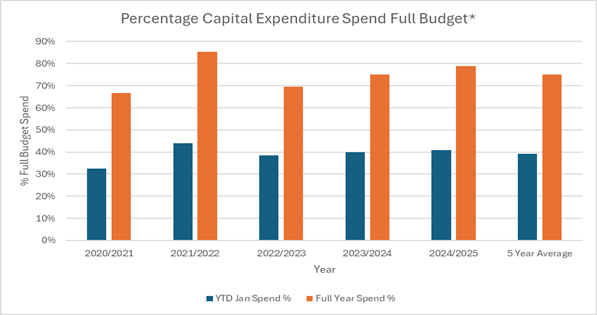

5.4 The following chart provides context on

how capital programme delivery typically profiles through the financial year

and how the Council actively manages delivery, borrowing, and affordability

risks.

Chart 4 | Historical Capital Expenditure

Trend (Excluding JV’s)

Chart 4 | Historical Capital Expenditure

Trend (Excluding JV’s)

* Note:

“Full Budget” refers to the Annual Plan budget, including approved

carry‑forwards and any additional amounts or changes approved by Council

during the financial year.

5.5 Over

the five‑year period shown in the chart above, the average proportion of

the full capital budget delivered within each financial year is approximately

75%. The remaining ~25% is predominantly timing-related underspend that

is carried forward into the next financial year as approved carry-forwards to

complete the same projects.

5.6 A summary of capital programme

management is outlined below.

5.6.1 As at 31

January 2026, capital expenditure represents 31% of the full‑year

programme. This result reflects both the timing of project delivery and

the concentration of expenditure later in the financial year for a number of

large projects, rather than a uniform slowdown across the programme.

5.6.2 While the programme’s unconstrained technical

forecast indicates a potential year‑end spend of $83.6 million against a

full‑year budget of $95.6 million, the Executive Leadership Team has

endorsed a reduced working capital delivery envelope of $70 million for the

current year. This envelope reflects assessed deliverability and will be used

as the basis for programme prioritisation, borrowing assumptions, and financial

management.

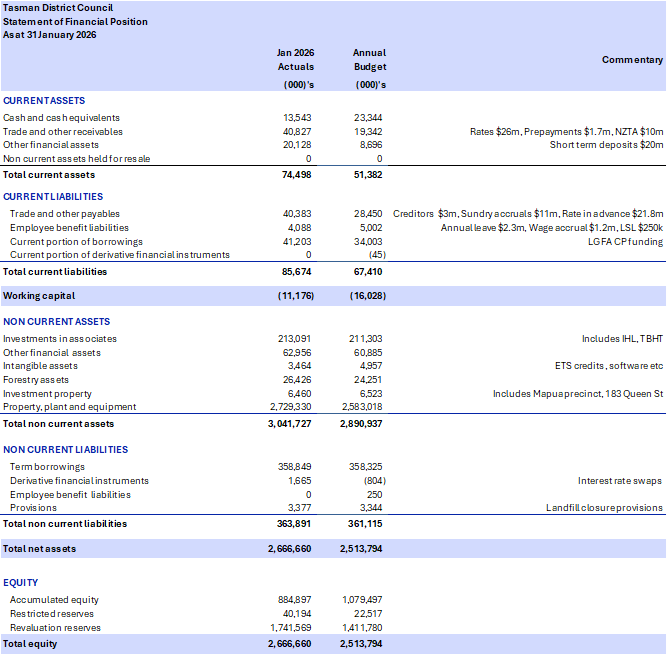

6. Statement of Financial Position (Balance Sheet)

6.1 Table 4 | Statement of Financial Position

6.2 Trade and other

receivables are higher at 31 January 2026 predominantly due to the timing of

quarterly rates billing.

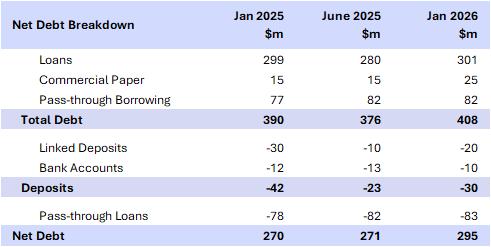

7. Net Debt and External Debt

7.1 As at 31 January 2026, the

Council’s total debt was $408.0 million, compared with $376.4 million at

30 June 2025. Net debt was $295.0 million, up from $271.3 million at 30 June

2025. This remains below the net debt level of $305 million projected in the

2025/26 Annual Plan.

7.1 As at 31 January 2026, the

Council’s total debt was $408.0 million, compared with $376.4 million at

30 June 2025. Net debt was $295.0 million, up from $271.3 million at 30 June

2025. This remains below the net debt level of $305 million projected in the

2025/26 Annual Plan.

7.2 Pass‑through

loans relate to shareholder advances to Waimea Water Limited to fund the Waimea

Community Dam. These loans are excluded from the Council’s net debt

calculation, as the associated cashflows are passed through to the Council‑controlled

entity. However, they are included when assessing the Council’s total

borrowings from the Local Government Funding Agency (LGFA) and compliance with

LGFA covenants.

7.3 Commercial

paper is a short‑term funding tool used to manage liquidity and timing

differences within the financial year. The use of commercial

paper is consistent with the Council’s Treasury Management Policy and

supports prudent cashflow and debt management without increasing long‑term

debt commitments.

7.4 Linked

deposits reflect the pre‑funding of the Council’s April 2026 LGFA

loan repayments and form part of the Council’s approved treasury

management strategy. These deposits temporarily increase gross debt but reduce

refinancing risk and support liquidity management.

7.5 Table

5 below provides a breakdown of net debt, including the impact of pass‑through

loans and linked deposits.

Table 5 | Net

debt breakdown

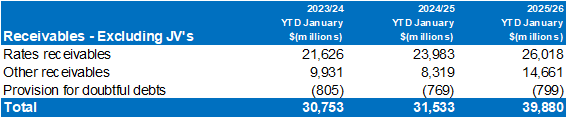

8.1 Rates receivables are consistent

with the same period in the 2024/2025 year after accounting for rates income

increases. The balance primarily reflects the timing of this report. Other

receivables are higher than the prior year, largely due to the recognition

of subsidy and grant income related to recent weather events.

8.2 The receivables

summary is set out below:

Table 6 |

Debtors / Receivables

8.3 As noted earlier

in the report the timing of the quarterly rates billing leads to a larger rates

receivable in January. Other receivables includes $9.1 million of Waka

Kotahi weather event related funding that has been agreed.

9. Councillor Queries at 19th February

Equivalent Report

9.1 At the meeting held on 19 February, councillors raised a

number of questions and requests for further information. Staff undertook to

consider these matters and report back where practicable. This section provides

an update on those items.

9.2 Some requests are constrained by the capability of the

Council’s current financial system, which has been in place since the

1990s. While the Modern Finance programme is intended to address these

limitations, the transition to a new system is complex, costly and will take

time. Certain information cannot currently be produced due to the structure of

the general ledger and the way the system (MagiQ Enterprise) captures and

records data.

9.3 The following actions have been

completed in response to councillor queries:

9.3.1 A

historic year‑to‑date capital expenditure comparison for the same

period in the previous financial year has been included.

9.3.2 We have added a five-year capital expenditure graph that

shows where the current year compares with previous years spend.

9.3.3 Development

contributions have been clarified. Contributions are payable once a Section 222

certificate is issued and ultimately fund capital expenditure. At present,

receipts are primarily used to reduce development‑related debt, as the

development contribution balance is in deficit due to the pace of growth in the

district. By the end of 2033/34, development‑related debt is expected to

exceed $100 million. This debt is forecast to be repaid over time as

development contributions are collected, reflecting the Council’s growth

profile.

9.3.4 The councillors are provided financial results regularly

through the Strategy, Finance and Performance Committee. This is where

monthly financial results are best sourced.

9.3.5 A question was asked around lower development contributions this

year and how that impacts future years. Lower development contribution

revenue in the current year will be reflected in updated budget projections and

considered as part of future planning cycles.

9.4 Other

requests cannot currently be progressed without significant changes to the

general ledger structure or the implementation of an enhanced financial system

or are simply not appropriate.

9.4.1 A request for cost and revenue reporting by ward, community,

or neighbourhood cannot be supported at this time. Even with a modernised

system, allocating costs at this level would be complex and would require

careful consideration as part of any future system design

9.4.2 It was suggested that known future commitments be

incorporated into the net debt cap calculation. Net debt is a point‑in‑time

measure reflecting the Council’s cash position. Including commitments

without also including known future income would not provide a balanced or

meaningful measure. The new debt calculation in the Annual Plan is intended to

act as a proxy for these future inflows and outflows, including commitments.

9.4.3 For similar reasons, net debt calculations are not produced

on a monthly basis. Operating revenue is received unevenly throughout the year,

and the information required to calculate the dynamic net debt cap is most

appropriately assessed at year end.

9.4.4 A

request was made to provide the Net Debt Headroom with regard to the both the

Treasury policy limit of a dynamic 160% and the LGFA requirements for the

current year. This ratio is calculated on a full revenue figure. We do not have

this till year end so the ratio or graph presented would be meaningless if

calculated during the year.

Nil

Strategy Finance and

Performance Committee Agenda – 19 March 2026

7.3 Long-Term Plan Assumption - Population

Projection

Decision Required

|

Report

To:

|

Strategy

Finance and Performance Committee

|

|

Meeting

Date:

|

19

March 2026

|

|

Report

Author:

|

Geoff

Everitt, Senior Policy Advisor – Data Analysis

|

|

Report

Authorisers:

|

Sue

McLean, Kaiwhakahaere ā Rōpū – Te Pae Rautaki Ahumoni |

Group Manager - Strategy & Finance

|

|

Report

Number:

|

RSFP26-03-4

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 Staff

seek approval of the population growth assumption for the Long-Term Plan (LTP)

2027-2037.

1.2 The

decision sought now is for the Committee to approve the population growth

assumption (High) that will be used to anchor the Growth Model update and

Long-Term Plan 2027–2037.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 Staff

recommend adopting the High population growth scenario to guide the Growth

Model update and Long-Term Plan 2027–2037, as it provides a more cautious

basis for identifying potential long‑term infrastructure, regulatory, and

land‑supply risks.

2.2 The

High scenario is expected to provide a more risk‑aware planning

foundation if higher growth occurs.

2.3 The

executive leadership team (ELT) endorsed the use of the High projection on 17

February 2026, following consideration of a memo presented to it.

3. Recommendation/s

/ Ngā Tūtohunga

That the

Strategy Finance and Performance Committee

1. receives

the Long-Term Plan Assumption - Population Projection RSFP26-03-4; and

2. approves the high population assumption as the basis

for the growth model and related planning in the Long-Term Plan 2027-2037.

4.1 A

population assumption is required so staff can complete the Growth Model update

and ensure supply and demand modelling is ready to inform subsequent LTP

workstreams, including infrastructure, land‑use, and financial planning.

Timely endorsement is essential

to keep Growth Model outputs on schedule for May 2026, allowing them to feed

into wider LTP development without delay.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 For

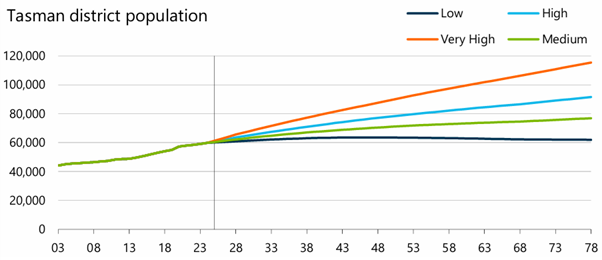

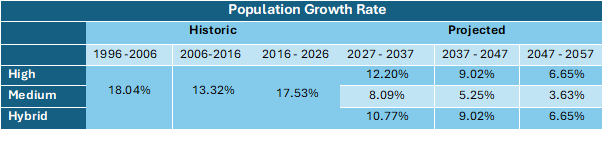

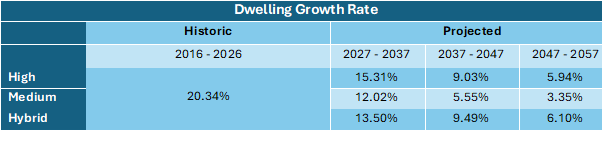

LTP purposes, analysis has focused on the Medium, High, and Hybrid population

scenarios. All three track similarly in the early years; however, by 2037 the

difference between Medium and High is approximately 900 dwellings and 3,600

residents, widening further over the longer term. The Hybrid scenario sits

between the two.

5.2 The

High scenario aligns with the assumption used in the previous LTP. Although

growth has slowed recently, reflected in the decline in building consent

applications, long‑term trends, including historic population

variability, have more closely tracked the High projection. The Hybrid scenario

reflects current short‑term slowdown more directly but introduces

additional modelling complexity.

5.3 The

demographer advised that growth is statistically most likely to follow the

Medium projection but noted that planning decisions should incorporate wider

policy and infrastructure considerations. Historically, national projections

have tended to be too conservative (i.e. underestimated growth).

5.4 Tasman

has experienced large year‑to‑year swings in both dwelling and

population growth, with periods of rapid increase followed by sharp slowdowns.

Because of this volatility, short‑term movements may give only limited

guidance for long‑term planning.

5.5 Selecting

a higher projection reduces the risk of under‑estimating long‑term

demand, particularly for long‑life infrastructure where capacity

constraints are costly to correct. Lower‑than‑expected growth can

be adjusted for through future LTP cycles with comparatively limited impact.

This decision sets only a planning assumption and does not approve or alter any

projects, funding, or levels of service.

5.6 Councillors

asked whether selecting a Medium or High population assumption would influence

longer‑term rates

movements. Staff cannot advise how the two assumptions will affect the final

rates requirements for the LTP 2027–2037, as financial modelling is still

underway and depends on multiple interacting factors.

5.7 In

principle, however, the total revenue requirement in any given year is divided

across the number of rating units. If growth is higher, the same total revenue

requirement is spread across more rating units, which has a moderating effect

on the average rates increase. Over a 10‑year

period, the Medium and High scenarios differ by approximately 3.48 percentage

points in projected dwelling growth, and this difference represents the scale

of additional rating units over which future revenue requirements would be

allocated. This effect is only one component of overall rates movements and

will be assessed in more detail through the LTP financial modelling.

5.8 Staff

also used AI‑assisted analysis to explore whether councils experiencing

higher population growth tend to have higher rates than lower‑growth

councils. The findings were inconclusive and did not show a consistent

relationship. Rates movements are influenced by multiple factors beyond growth

alone, including development timing, density, funding gaps, and the sequencing

of infrastructure investment.

5.9 Projections

do not determine whether a council is “high growth”; this is based

on actual population and development trends, and there is no formal criterion

for defining high growth status. Tasman has experienced what is commonly

regarded as high growth for at least two decades and continues to maintain

comparatively low rates relative to the wider sector. Projections are planning

tools used to understand possible future demand, and risks for rates exist

under both under‑ and over‑estimating growth.

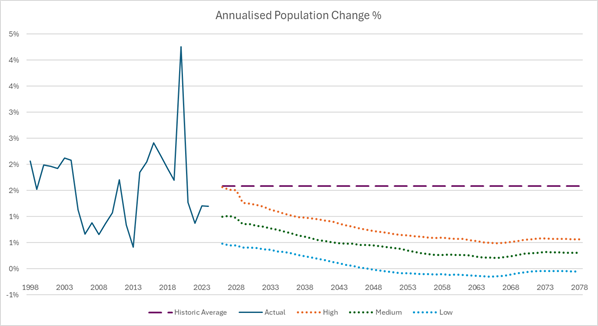

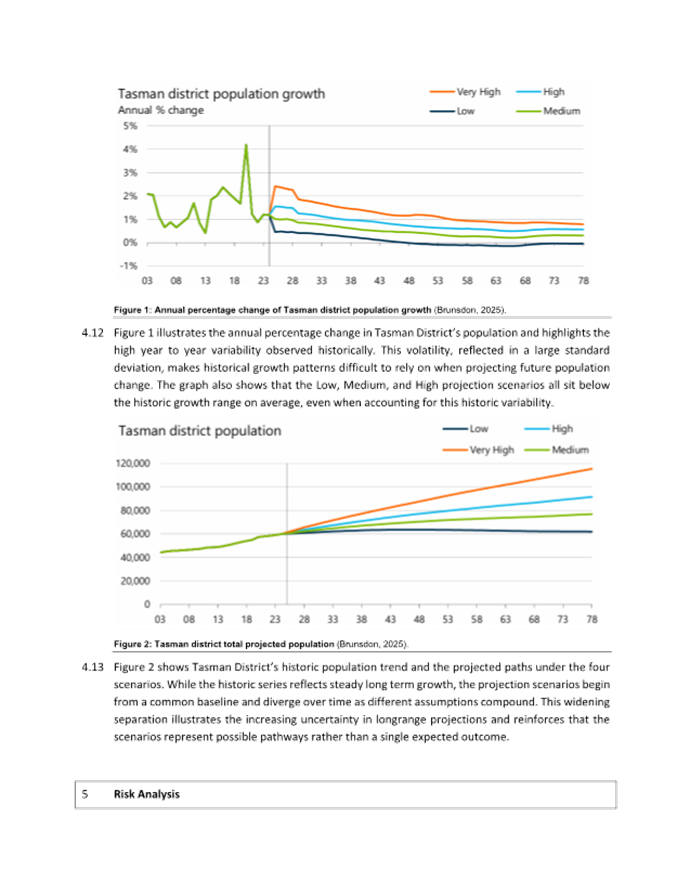

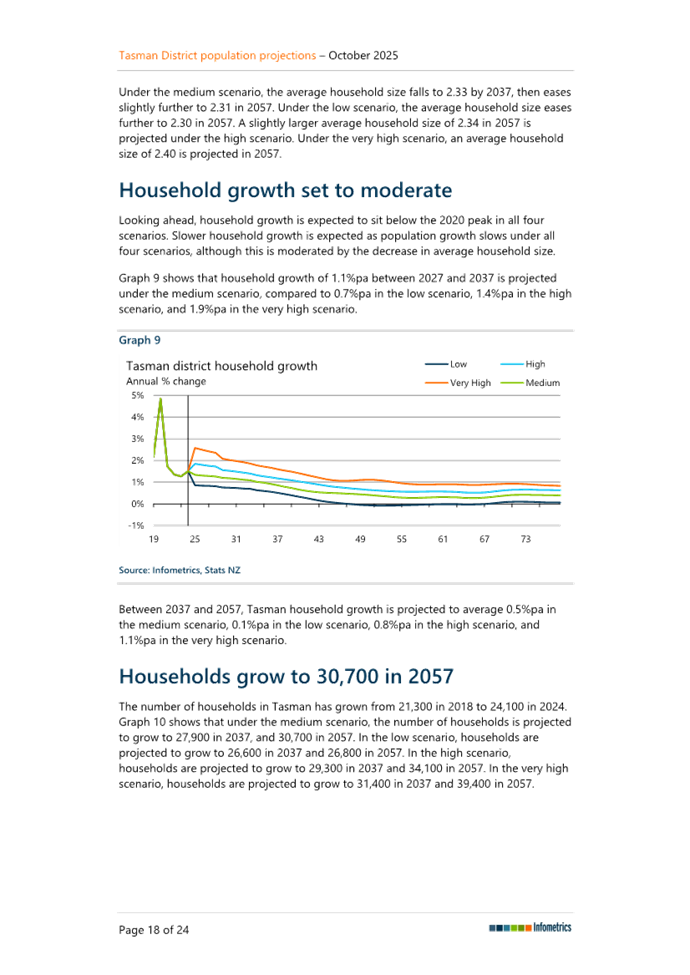

Figure 1 - Annual population change % historic,

projected, and historic average

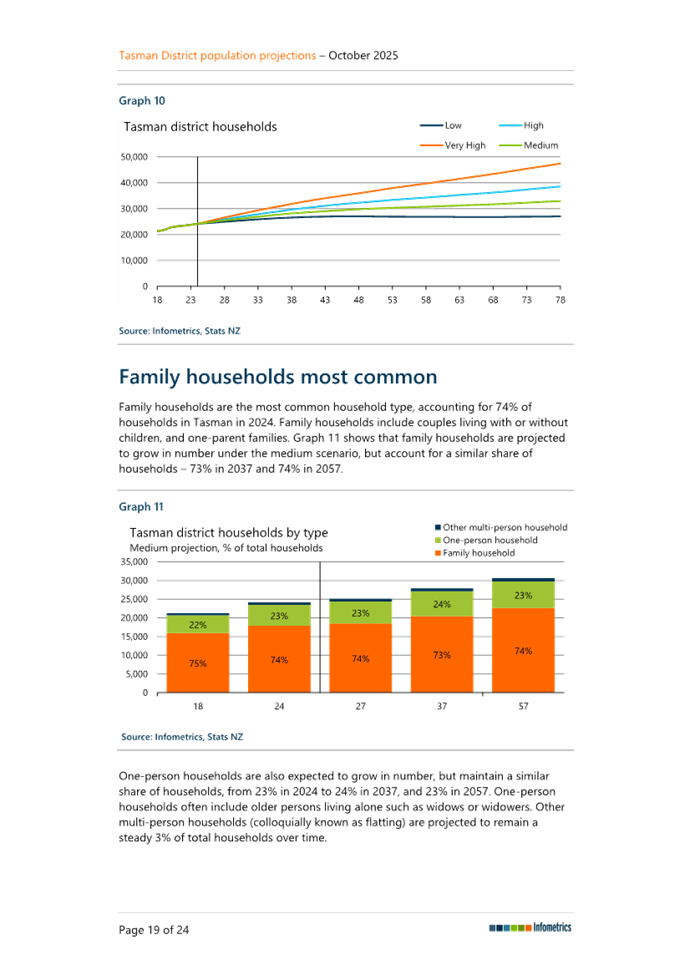

Figure 2 - Total population historic and projected

Figure 2 - Total population historic and projected

Table 1 - Historic and projected population growth

10-year average

Table 2 - Historic and projected dwelling growth

10-year average

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

6.1 This decision has no direct

financial impact. It may indirectly influence long‑term revenue and

expenditure forecasting as growth assumptions flow into later stages of the LTP

programme.

7.1 The options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Approve the High scenario

|

Provides a resilient planning basis for long‑life

infrastructure, identifying the risk of under‑investment and future

capacity shortfalls.

Aligns with Tasman’s longer term growth trends,

which have tracked closer to the High projection.

Is considered to support LGA obligations to plan for the

long term and manage risk.

Identifies the likelihood of community impacts arising

from higher‑than‑expected growth

without sufficient infrastructure.

Consistent with emerging central government signals to

plan for higher growth.

Rates and debt settings can be adjusted in future LTP

cycles if actual growth is lower than projected.

|

May indicate a need for infrastructure to

be timed earlier than ultimately required if growth slows.

Could create perception of over‑planning or over‑estimating growth in the short term.

Higher growth rate could indicate earlier infrastructure

needs during preliminary modelling, which could place pressure on early

financial forecasts.

Building Consent data shows a sharp decline in building

consents applications.

|

|

2.

|

Approve the Hybrid scenario

|

Recent declines in building consent

applications indicate lower dwelling growth in the short term, and the Hybrid

scenario better reflects this early‑period slowdown.

After the initial years, the Hybrid

trajectory transitions toward a rate that more closely matches Tasman’s

longer‑term growth behaviour.

By applying the Medium projection in the

early years, the Hybrid scenario reduces the chance of signalling

infrastructure needs earlier than necessary during the first one to two LTP

years.

Switching to the High rate for later

years still provides visibility of potential long‑term

infrastructure pressures if higher growth occurs.

It avoids the binary choice between Medium and High by

recognising both current market signals and the district’s longer‑term

trend, which may reduce the likelihood of short‑term financial

pressure.

|

Using two different growth rates over the projection

period can introduce additional complexity for modelling.

The rationale for using a transitional projection may

require more explanation to stakeholders compared with a single scenario.

Central government are trending toward planning for higher

growth; the Hybrid scenario may be seen as less aligned with that direction.

Applying the Medium rate early could delay the

identification of future infrastructure requirements if high growth resumes

sooner than expected.

|

|

3

|

Approve the Medium scenario

|

Aligns with the demographer’s

statistical assessment of the most likely population trajectory.

Aligns with sort term growth expectations

based on building consent applications being received.

May indicate a lower need for

infrastructure timing and capital expenditure assumptions if growth

moderates.

Could be perceived as a more conservative

or “right‑sized”

approach to current economic conditions

|

Increases the risk of under‑estimating future demand, particularly for long‑life infrastructure that is costly and slow to expand once

constrained.

Higher‑than‑expected growth can lead to community impacts that are more

difficult and costly to address than adjusting for lower growth over time.

Does not fully reflect recent or

long-term historic trends, which exceed the higher projection.

Provides less alignment with emerging

central government direction to plan for higher growth.

May require earlier corrective action if

growth exceeds expectations.

|

|

4

|

Approve the Low scenario

|

Lower assumed demand in the early years reduces the

likelihood of identifying infrastructure upgrades earlier than ultimately

required during preliminary modelling.

Can signal caution in the current economic environment by

avoiding assumptions that may appear optimistic or out of step with recent

slowdown.

Lower projected growth may reduce initial pressures on

debt, funding pathways, or capital programme assumptions during early

modelling stages.

|

If higher growth resumes, as has occurred historically,

this scenario may result in infrastructure capacity constraints that are

costly and slow to correct.

Under‑projecting growth can push key investments too

far into the future during modelling, increasing later pressure on levels of

service, compliance, and financial planning.

Diverges from national signals encouraging councils to

adopt more risk‑aware and future‑proofed growth planning

approaches.

|

7.2 Option 1 High growth scenario is

recommended.

8.1 The decision is primarily

governed by the Local Government Act 2002, which sets the requirements for LTP

assumptions, prudent financial management, and decision‑making processes.

The Resource Management Act 1991, particularly the National Policy Statement on

Urban Development, is also relevant as growth projections inform long‑term

land‑use and infrastructure planning. No other legislation directly

affects or constrains this assumption‑setting decision.

8.2 The following provisions of the

Local Government Act 2002 were considered particularly relevant to this

decision, and the recommendation has been assessed for alignment with them: the

purpose and principles in sections 10 and 14, the financial management

obligations in section 101, the decision‑making and engagement

requirements in sections 76–82, and the risk‑management

requirements for LTP assumptions in Schedule 10, clause 17. These sections

guided the assessment to support prudent, risk‑aware long‑term planning.

9. Iwi

Engagement / Whakawhitiwhiti ā-Hapori Māori

9.1 Engagement with iwi has not been

undertaken and is not proposed as this decision sets an internal planning

assumption and does not directly affect land, water, cultural values, or levels

of service. In line with the LGA 2002 requirement for engagement to be

proportionate to significance, iwi engagement is not required at this stage,

with any future implications addressed through subsequent LTP or statutory

processes.

10. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

10.1 The overall significance of the decision has been

assessed as low to moderate

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Medium

|

Some level of interest may arise

from stakeholders who follow growth and planning matters, but the decision is technical and does not

directly change services or rates at this stage. It may attract attention

from specific stakeholders, but is not expected to be widespread.

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Medium

|

The decision

influences long‑term planning assumptions but does not directly change

services, assets, or financial settings at this stage. Any effects on

community well‑being would occur indirectly through later LTP

decisions, so impacts are possible but not immediate or substantial.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Low

|

The decision sets an

assumption for planning purposes only. Any long‑term effects depend on

later LTP decisions, so the duration of impact from this specific decision is

limited.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

Low

|

The decision informs

planning for Council’s strategic infrastructure assets but does not

alter, dispose of, or reprioritise any specific asset at this stage. The link is

indirect, so the level of significance is medium rather than high.

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

Low

|

The decision does not change any

levels of service. It only sets a planning assumption, so no substantial

service impacts arise at this stage.

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

Low

|

The decision does not directly

change financial settings. Any effect on debt or rates would occur later

through LTP processes, so the immediate financial impact of this decision is

low.

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

NA

|

The decision does not involve

any sale of shareholdings in a CCO or CCTO.

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

NA

|

The decision does not involve

entering into any private sector partnership or contracting out any Council

activity.

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

NA

|

The decision does not involve

entering into or exiting from any group of activities.

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

Low

|

While the growth projection will

inform future infrastructure planning for water services, this decision does

not itself change any water, wastewater or stormwater activities, nor does it

trigger specific Te Mana o te Wai obligations. Current water sector reforms

do not materially affect or change the nature of this assumption‑setting

decision.

|

11. Communication

/ Whakawhitiwhiti Kōrero

11.1 Communication to date has been internal and with

Nelson City Council (NCC) officers, including discussions with engineering,

planning, ELT and other staff who rely on the Growth Model for LTP inputs.

Staff have also engaged with NCC to understand whether there is an opportunity

to align approaches.

11.2 NCC currently propose using the Medium scenario for

their LTP and the High scenario for other planning purposes, reflecting the

demographer’s advice that actual growth is statistically more likely to

track near the Medium projection. Council staff have considered this advice in

the context of Tasman’s infrastructure risk profile and planning

requirements and have formed their recommendation accordingly.

12.1 The overall risk is assessed as medium and relates

to the planning consequences of selecting a higher or lower population

projection.

12.2 Adopting the High scenario carries the risk

that actual growth may be lower than projected, which could indicate

infrastructure timing earlier than necessary and create perceptions of over‑planning. Any

implications arising from this assumption can be addressed through later stages

of this LTP or future LTP and annual plan cycles.

12.3 Not adopting the High scenario increases the

possibility of under‑estimating long‑term demand,

which is difficult and costly to correct once infrastructure constraints

emerge. This risk profile has greater potential implications for levels of

service, compliance, and financial sustainability.

12.4 Mitigation includes ongoing monitoring of growth,

regular reassessment through LTP cycles, annual plan cycles, and refinement of

infrastructure and financial assumptions as new information becomes available.

12.5 Revising the population assumption at a

later stage will require re‑work for the Growth Model and for any Council

outputs that rely on it, which may in turn delay delivery of the LTP programme.

12.6 If Nelson City Council adopts a lower

projection, there is a possibility of divergence in long‑term

assumptions. This does not materially alter the assessment undertaken for

Tasman. However, if higher growth occurs in Nelson without corresponding

provision, demand may shift toward Tasman, with potential implications for

infrastructure planning and cost‑allocation, noting that cross‑boundary

demand could arise under any scenario if actual growth exceeds local provision.

13. Climate

Change Considerations / Whakaaro

Whakaaweawe Āhuarangi

13.1 The decision in this report was considered by staff

in accordance with the processes set out in Council’s Climate Change

Consideration Guide.

13.2 This decision will have no impact on greenhouse gas

emissions. This decision will have no impact on resilience to climate change

and the ability of the Council to proactively respond to the impacts of climate

change.

14. Alignment

with Policy and Strategic Plans / Te Hangai ki ngā aupapa Here me ngā

Mahere Rautaki Tūraru

14.1 This decision supports the development of the Long‑Term Plan by establishing a planning assumption required under the

Local Government Act 2002. The population projection informs, but does not

determine, subsequent work on infrastructure, financial, and land‑use planning. Any future implications for levels of service,

infrastructure programmes, or financial settings will be considered through

later LTP processes or other statutory planning documents, including asset

management plans, the Financial Strategy, Infrastructure Strategy, and the

Tasman Resource Management Plan.

14.2 The decision is within the delegation of the

Strategy, Finance and Performance Committee, which is responsible for oversight

of LTP preparation and underlying assumptions

15. Conclusion

/ Kupu Whakatepe

15.1 The High population projection is considered to

provide a sound planning assumption for the development of the Long‑Term Plan and the associated Growth Model update. It offers a

resilient basis for identifying future infrastructure and land‑use pressures while allowing any financial implications to be

addressed through later LTP processes. The decision does not commit Council to

any specific programme or funding pathway and can be refined in future planning

cycles as new information becomes available.

16. Next

Steps and Timeline / Ngā Mahi Whai Ake

16.1 Growth

Model outputs are on schedule for May 2026, allowing them to feed into wider

LTP programme.

|

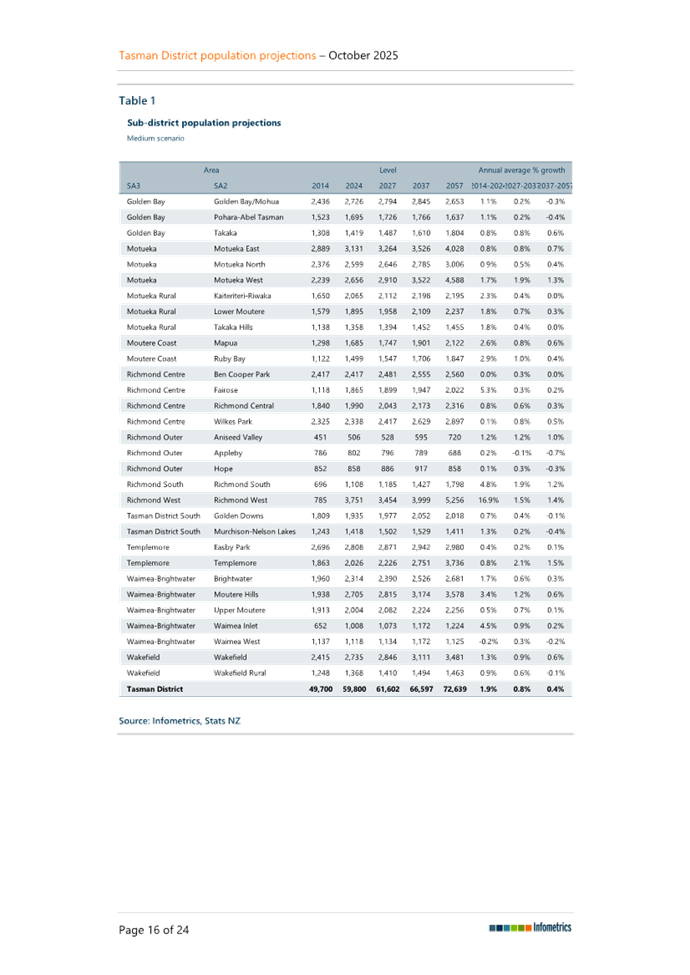

1.⇩

|

Population

Projection Technical Options Analysis

|

27

|

|

2.⇩

|

Infometrics

Tasman projection report

|

40

|

Strategy Finance and

Performance Committee Agenda – 19 March 2026

Strategy Finance and

Performance Committee Agenda – 19 March 2026

Strategy Finance and

Performance Committee Agenda – 19 March 2026

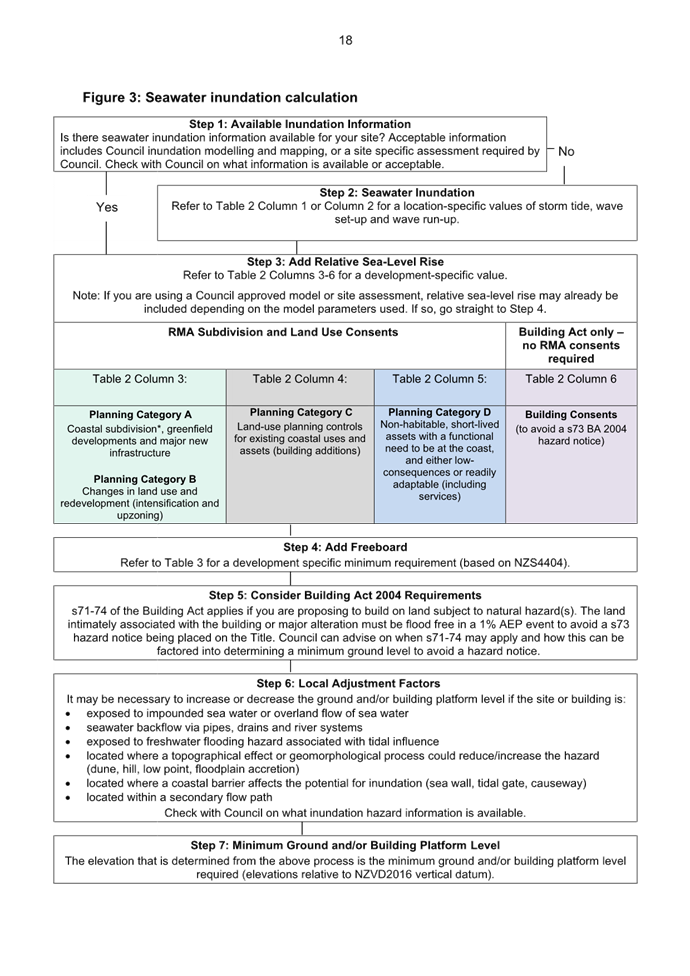

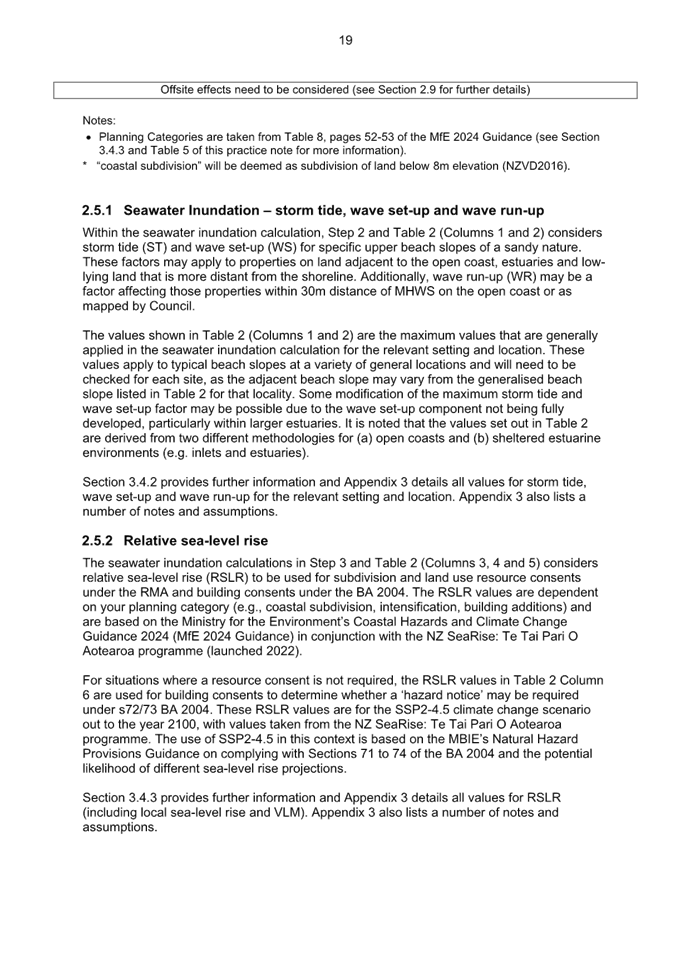

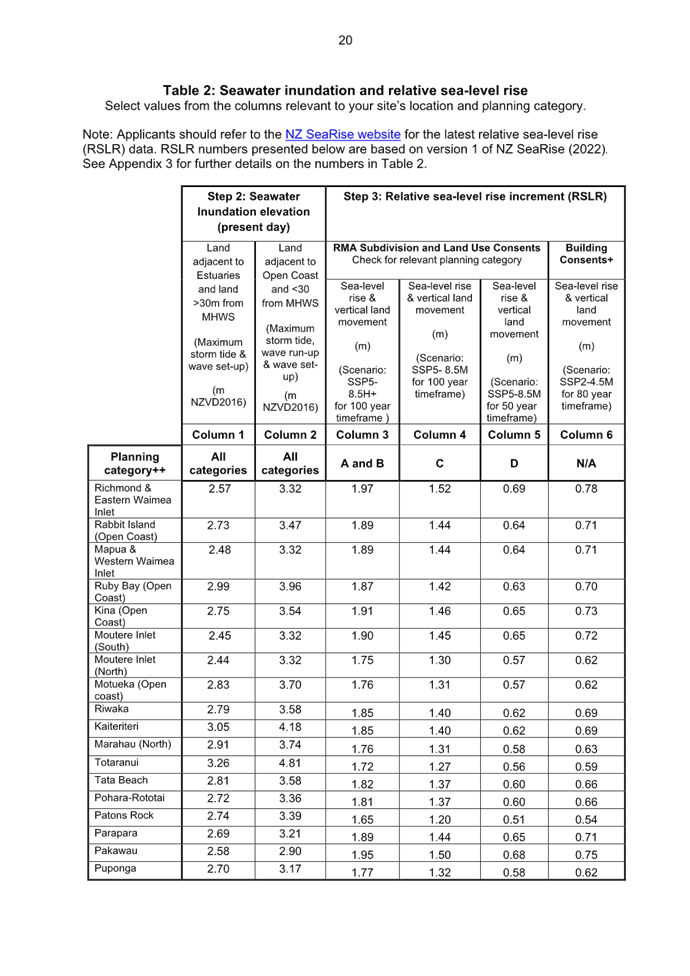

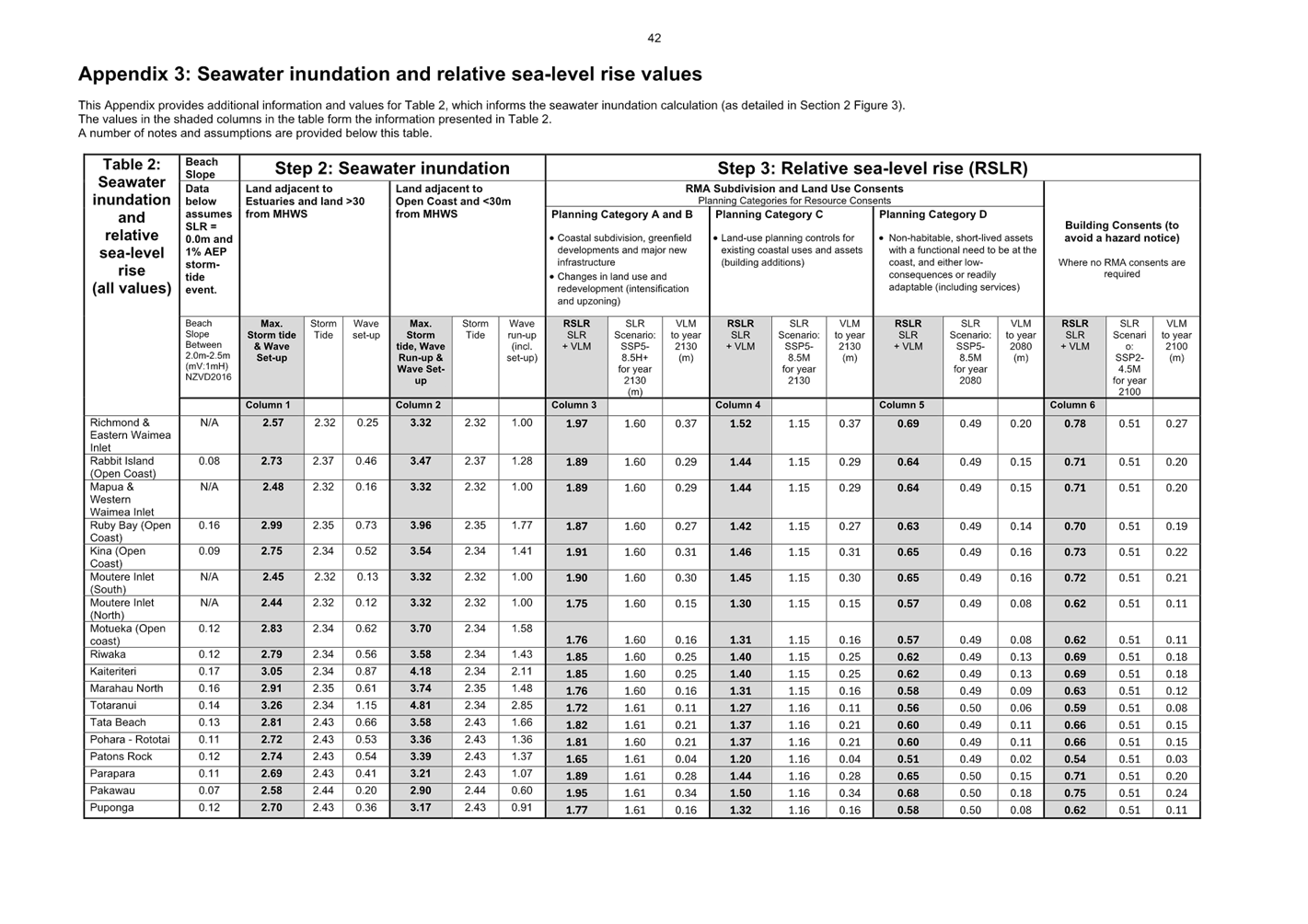

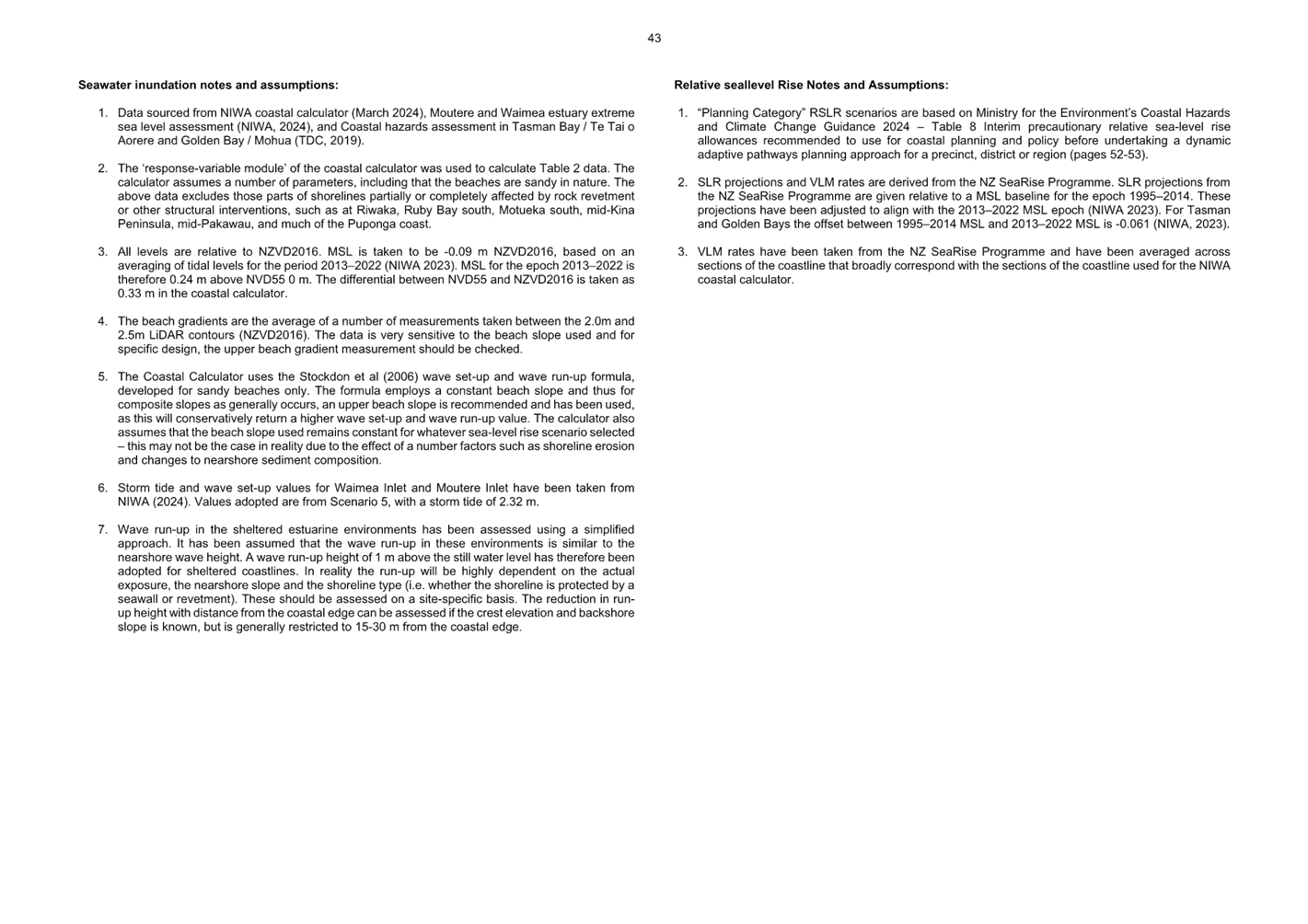

7.4 Adoption of Tasman Inundation Practice Note

Decision Required

|

Report

To:

|

Strategy

Finance and Performance Committee

|

|

Meeting

Date:

|

19

March 2026

|

|

Report

Author:

|

Paula

Hammond, Policy Planner - Natural Resources

|

|

Report

Authorisers:

|

Barry

Johnson, Environmental Policy Manager; Sue McLean, Group Manager - Strategy

& Finance

|

|

Report

Number:

|

RSFP26-03-1

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 This

report seeks the Council’s approval to adopt the Tasman Inundation

Practice Note (2026) (Attachment 1), incorporating minor amendments following

community engagement in late 2025/early 2026.

2. Summary

/ Te Tuhinga Whakarāpoto

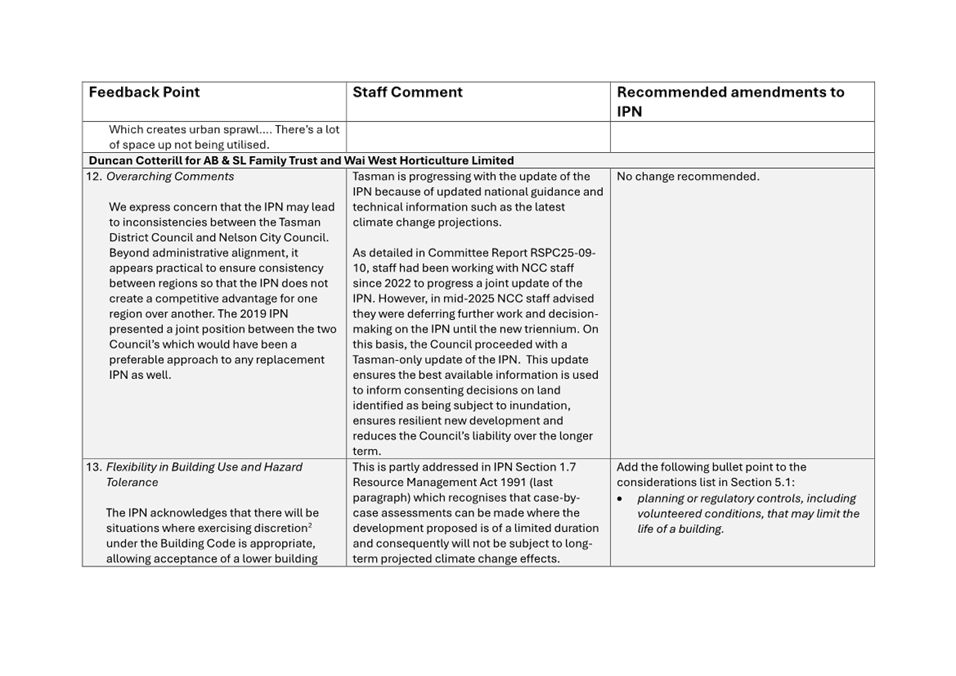

2.1 The Strategy and Policy Committee (18 September 2025 meeting)

approved release of the draft Tasman Inundation Practice Note (2025) for

community engagement (RSPC25-09-10).

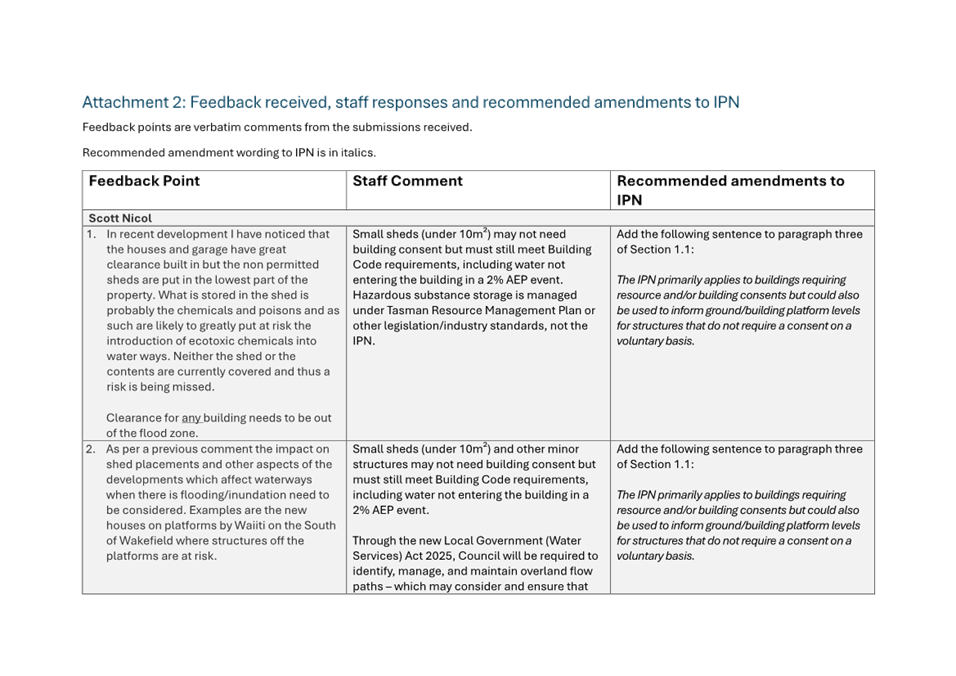

2.2 The Inundation Practice Note (IPN) is non-statutory guidance that

provides a standardised methodology to determine minimum ground and/or building

platform levels for development exposed to inundation (freshwater and coastal).

It assists implementation of the Resource Management Act 1991(RMA), the

Tasman Resource Management Plan (TRMP), and Building Act 2004 (BA).

2.3 During November 2025 to February 2026, Council sought community

feedback and five responses were received. Staff response to the feedback and

recommended amendments to the IPN are summarised in this report, with the full

feedback table presented in Attachment 2.

2.4 The feedback received was constructive and focused primarily on

clarifying the application of the IPN, particularly in relation to minor

structures, access and curtilage considerations, hazard notices, and the

interpretation of national guidance. There were no objections to the overall

methodology.

2.5 A

copy of the Tasman Inundation Practice Note 2026 for adoption is provided in

Attachment 1 with the recommended amendments included. Details

of the recommended amendments, including the specific locations within the IPN

where the changes have been incorporated, are provided in Attachment 2.

3. Recommendation/s

/ Ngā Tūtohunga

That the Strategy Finance and Performance Committee

1. receives

the report Adoption of Tasman Inundation Practice Note RSFP26-03-1; and

2. approves the recommended amendments to the Tasman

Inundation Practice Note in response to community engagement (as set out in

Attachment 2), noting that all requested amendments have been incorporated in

Attachment 1 to the agenda report; and

3. adopts the Tasman Inundation Practice Note 2026,

Attachment 1 to the agenda report.

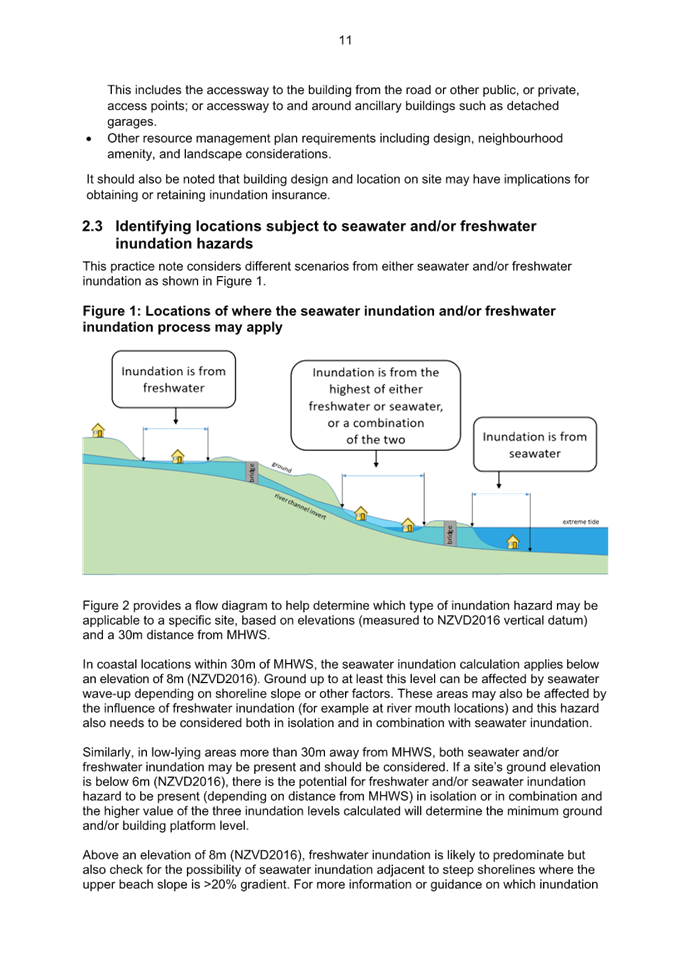

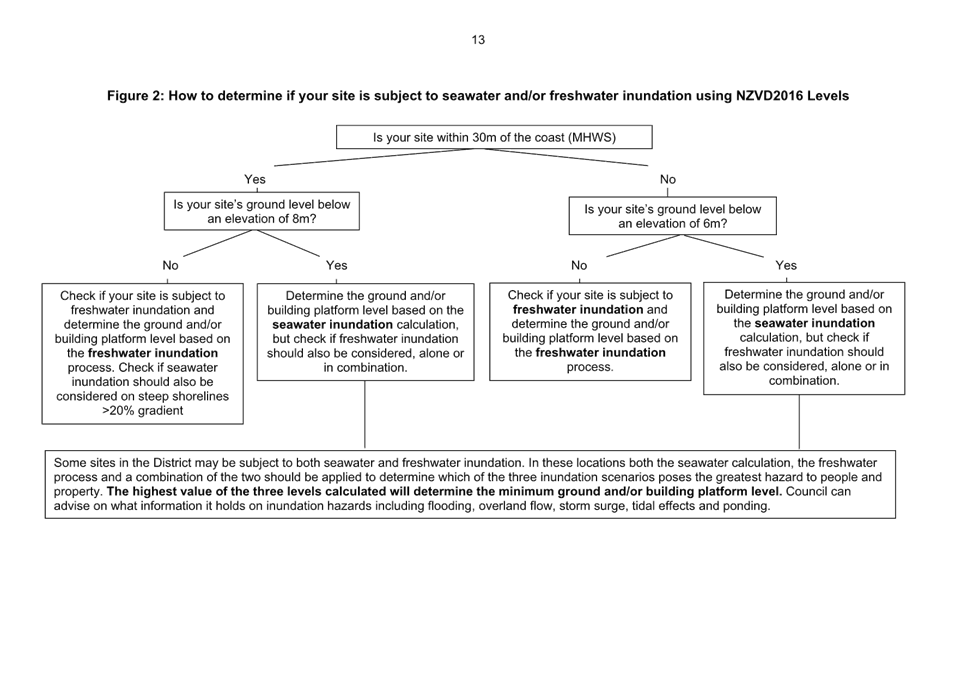

What is the Inundation Practice Note?

4.1 The IPN was

originally developed jointly with Nelson City Council (NCC) and adopted in 2019

to provide a consistent methodology for determining appropriate minimum ground

and/or building platform levels for development in areas at risk of seawater

and/or freshwater inundation. It is non-statutory guidance that supports the

TRMP, RMA and the administration of the BA.

4.2 Since adoption,

central government guidance and local technical datasets have been updated and

evolved. Tasman has progressively implemented these updates in consenting

practice, as the new guidance and data has become available.

4.3 Tasman and

Nelson staff had been working since mid-2022, toward completing a review and

update of the 2019 IPN. However, Nelson deferred decisions on reviewing and

updating the IPN to this triennium. Tasman prepared a standalone Tasman IPN

(2025) to align the document with current practice, national guidance and

updated technical data.

4.4 The Strategy and Policy Committee (18 September 2025 meeting)

approved an update of the 2019 Inundation Practice Note independently of Nelson

City Council and approved the draft Tasman Inundation Practice Note (2025) for

community engagement and feedback (RSPC25-09-10).

Engagement Undertaken

4.5 Public feedback

on the draft Tasman IPN (2025) was sought from November 2025 to February 2026

through Council’s communications channels (Shape Tasman, Newsline, social

media) with targeted outreach to Post Settlement Governance Entities, the

development and building sector, and planners via emails and sector

newsletters.

4.6 Key documents,

including a summary of the proposed changes, and a track change version of the

IPN were available on Shape Tasman to support feedback. A video offered a

summary of the IPN and provided a practical example of how the IPN could be

applied.

4.7 Five submissions

were received with the key themes and responses summarised in section 5 below,

with a detailed assessment set out in Attachment 2.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 The community engagement process from

November 2025 to February 2026 provided Council with valuable insights from a

range of stakeholders, including two lawyers on behalf of a developer and

landowners, one consultancy representative, and two members of the public.

While the volume of submissions was modest, the feedback received was

constructive and focused primarily on clarifying the application of the IPN,

particularly in relation to minor structures, access considerations, hazard

notices, and the interpretation of national guidance. The volume of feedback

received is consistent with the low to medium level of interest anticipated for

this technical document and is on par with the three responses received via the

2019 IPN consultation.

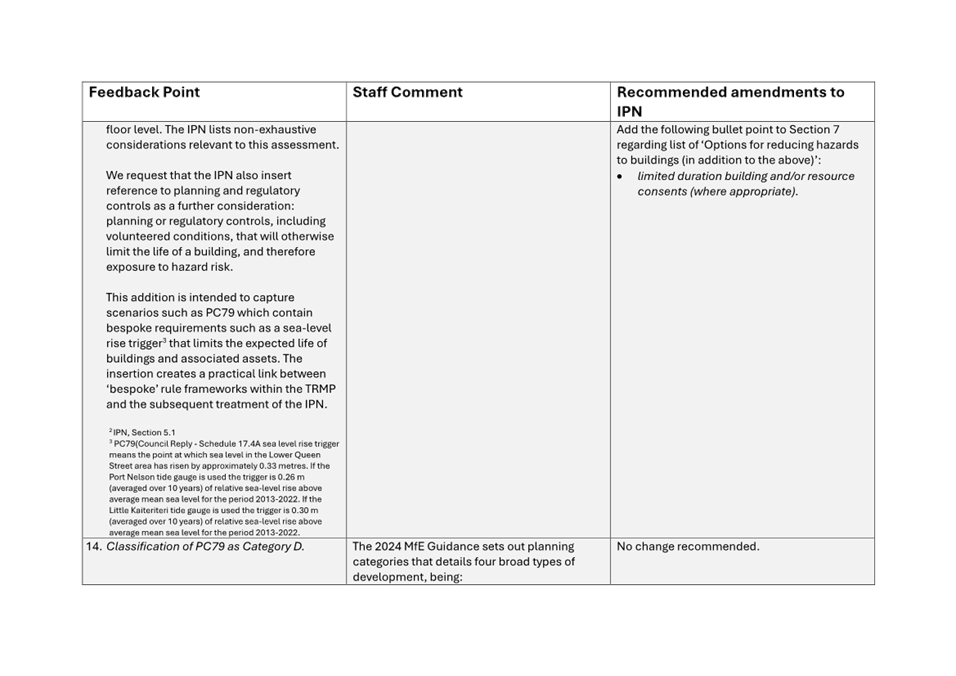

5.2 Attachment 2 details staff responses and

recommended amendments to the IPN for each individual submission point.

Key feedback

points and staff recommendations

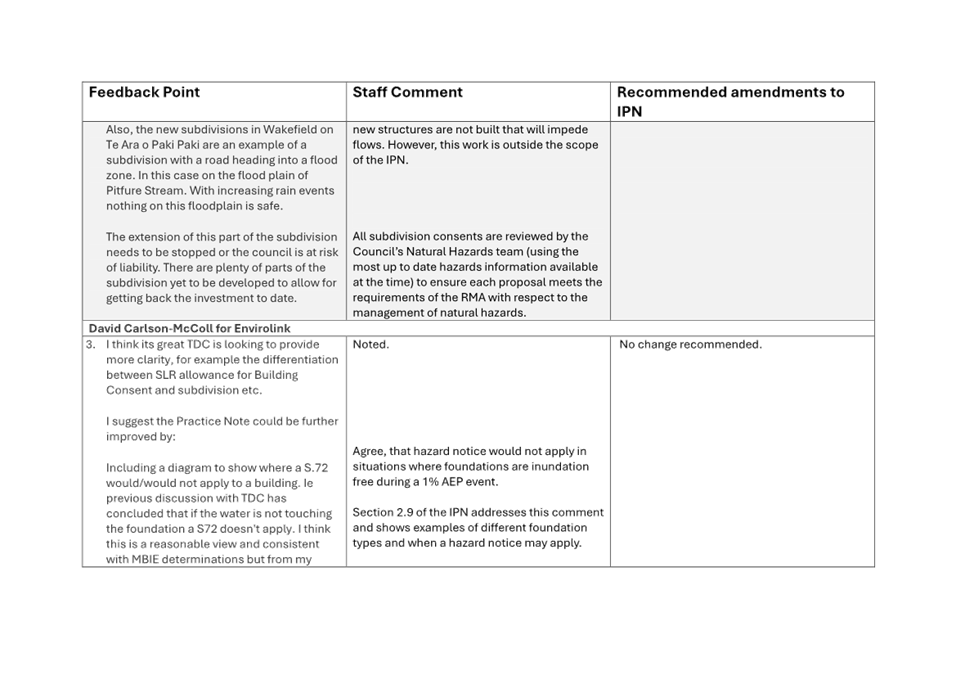

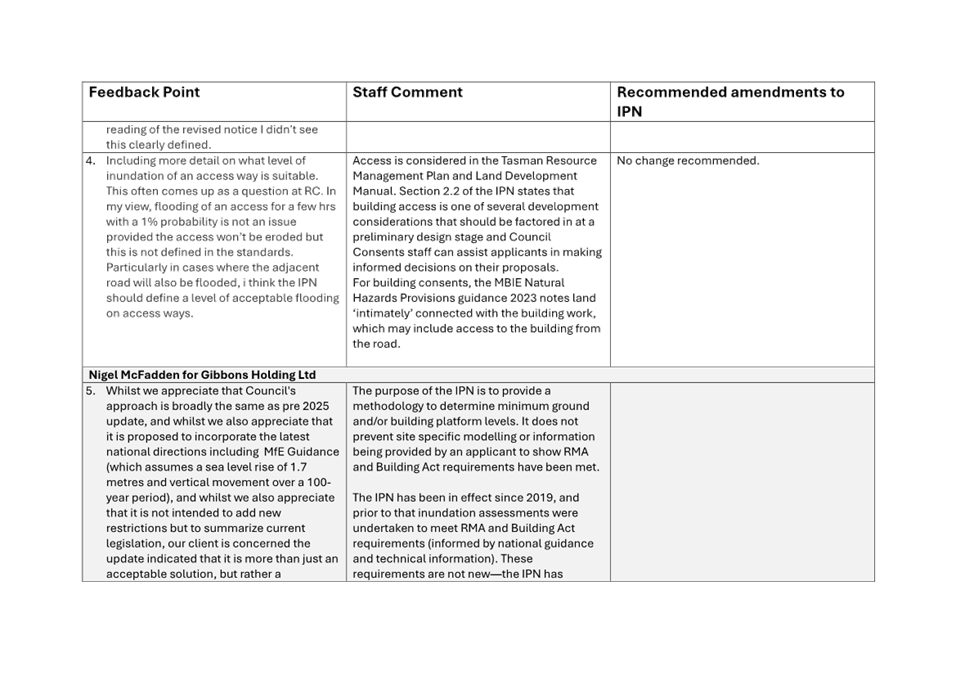

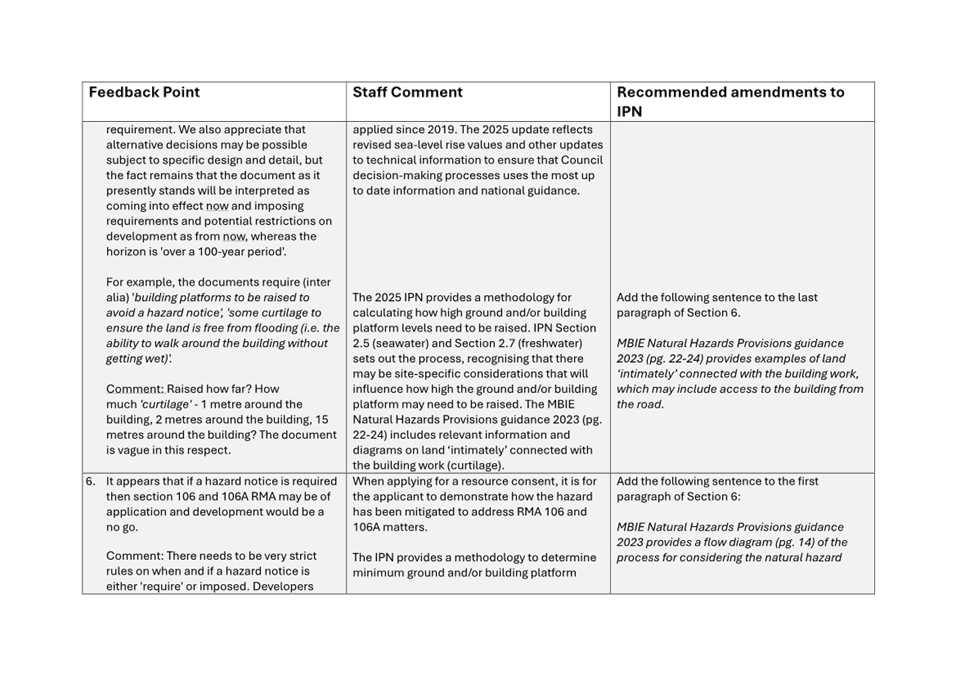

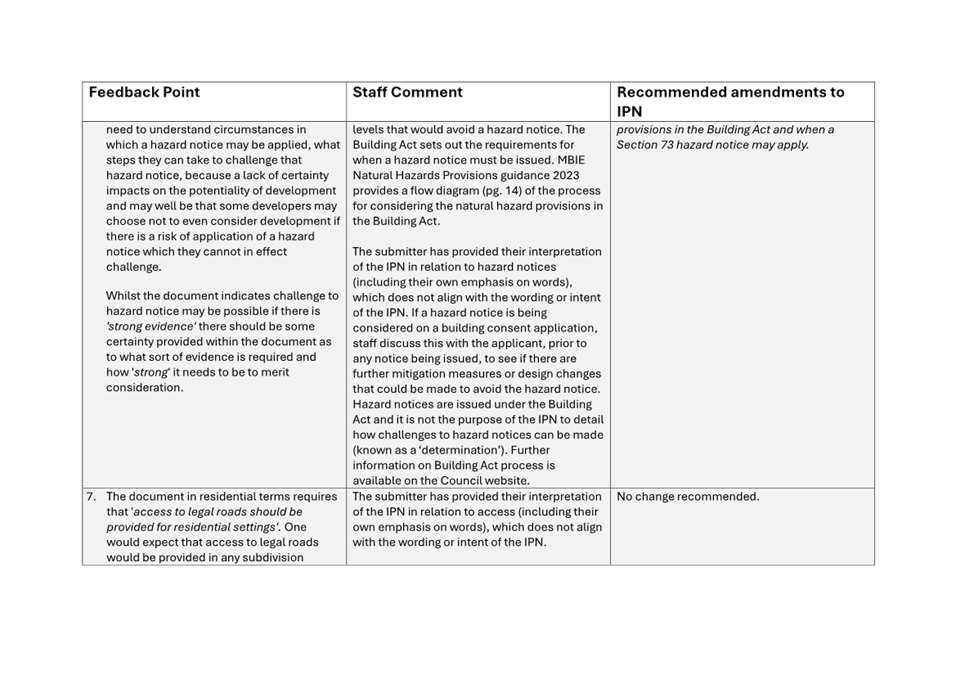

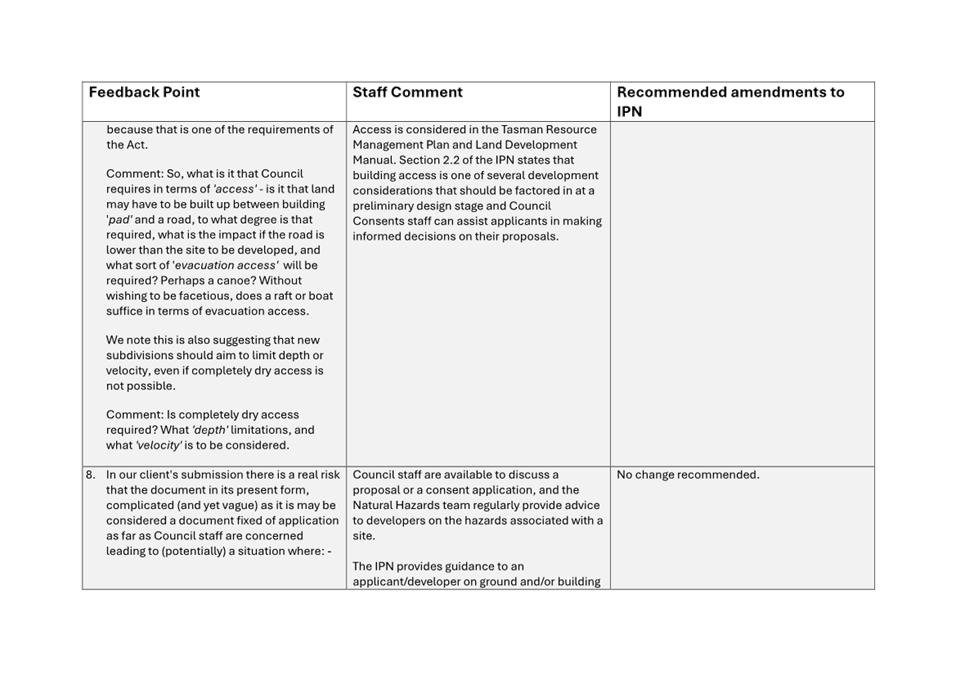

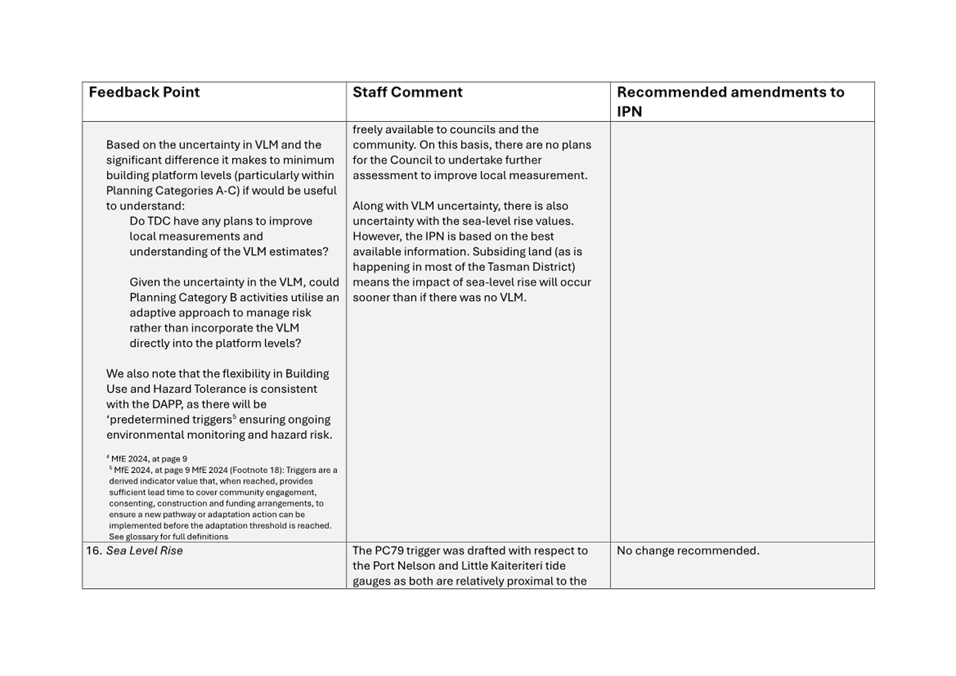

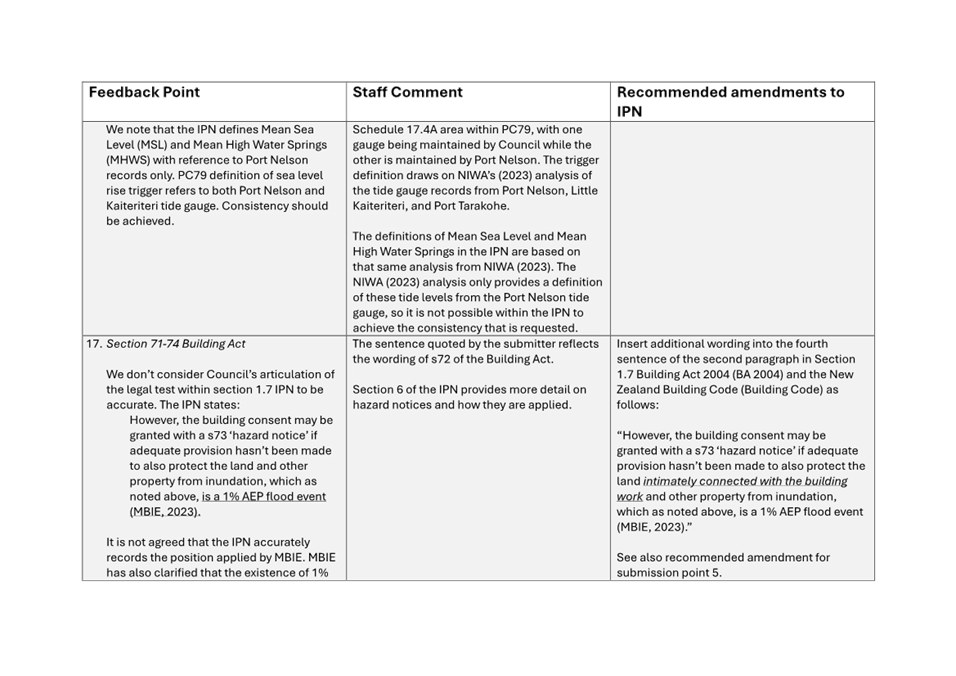

5.3 Submitters sought greater clarity on how the IPN applies in

practice, particularly for minor structures, hazard notices, and access or

curtilage requirements. They noted issues such as small, unconsented sheds

located in low‑lying areas, uncertainty around when Building Act hazard

notices apply, and how to interpret MBIE guidance. Staff recommend minor

clarifications to Sections 1.1 and 6 of the IPN, including cross‑references

to MBIE diagrams and guidance. No changes are recommended where the Tasman

Resource Management Plan, Land Development Manual or national direction

addresses the feedback points within these higher-order documents.

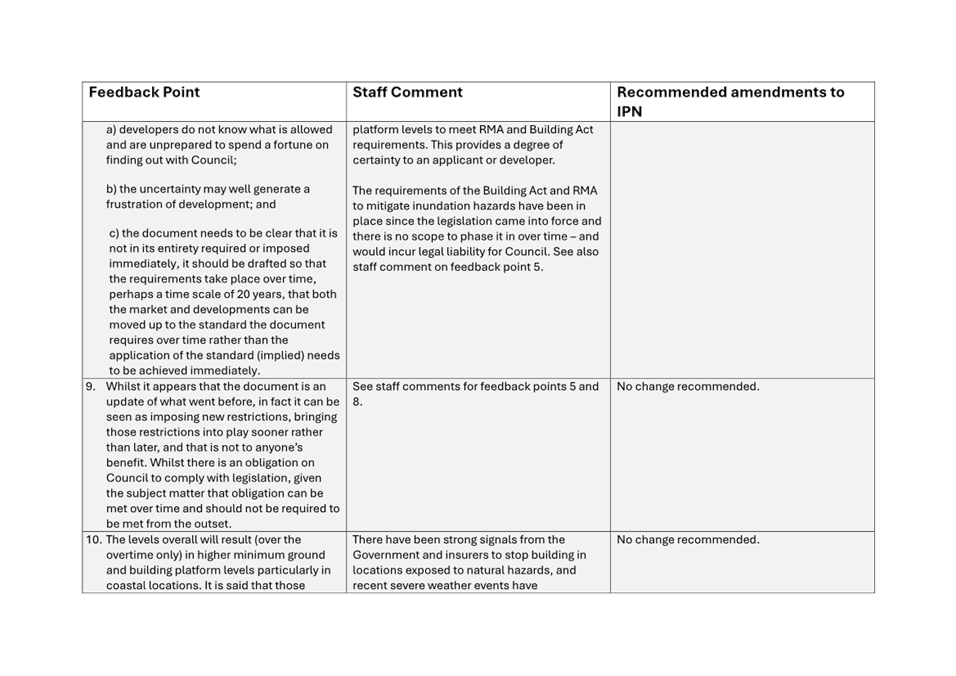

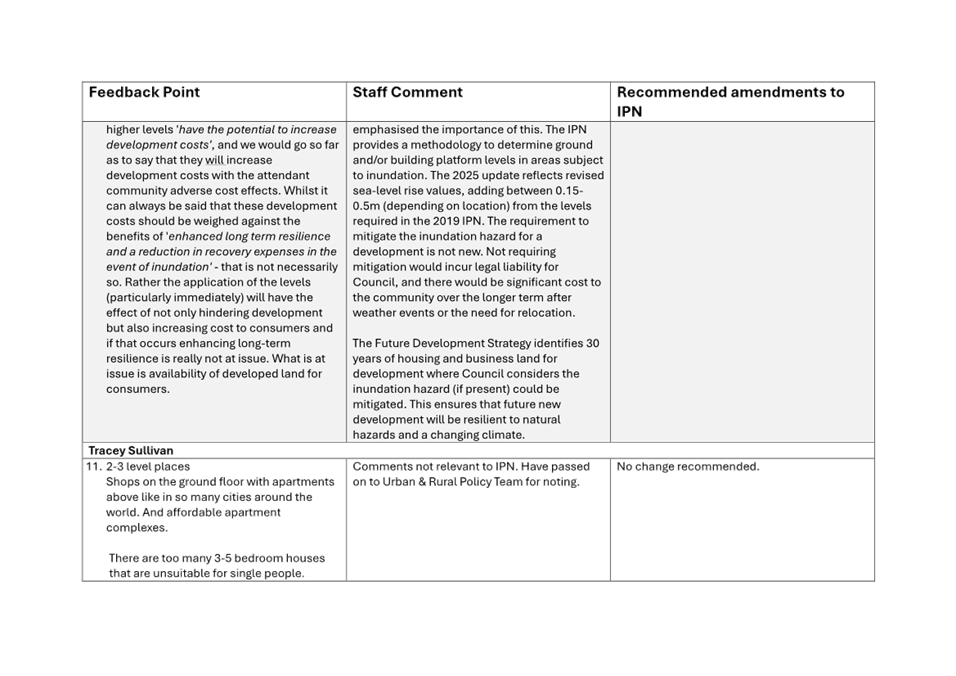

5.4 Feedback also touched on implementation concerns, including the

immediate effect of higher platform levels, cost implications, the treatment of

limited‑duration or trigger‑based consents, and alignment with

Nelson City Council. While recognising these issues, staff note that statutory

obligations to manage inundation hazards already exist, and phased

implementation of mitigation measures is not required as the requirement in

some instances to have higher platform levels is already being applied through

building and resource consents.

5.5 A further set of comments related to technical matters such as the

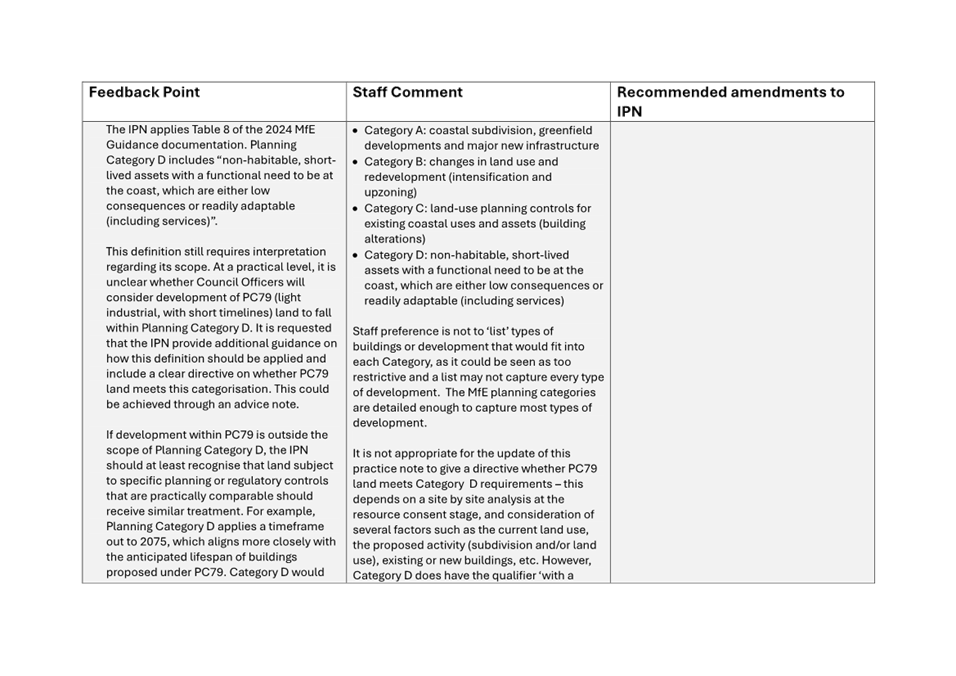

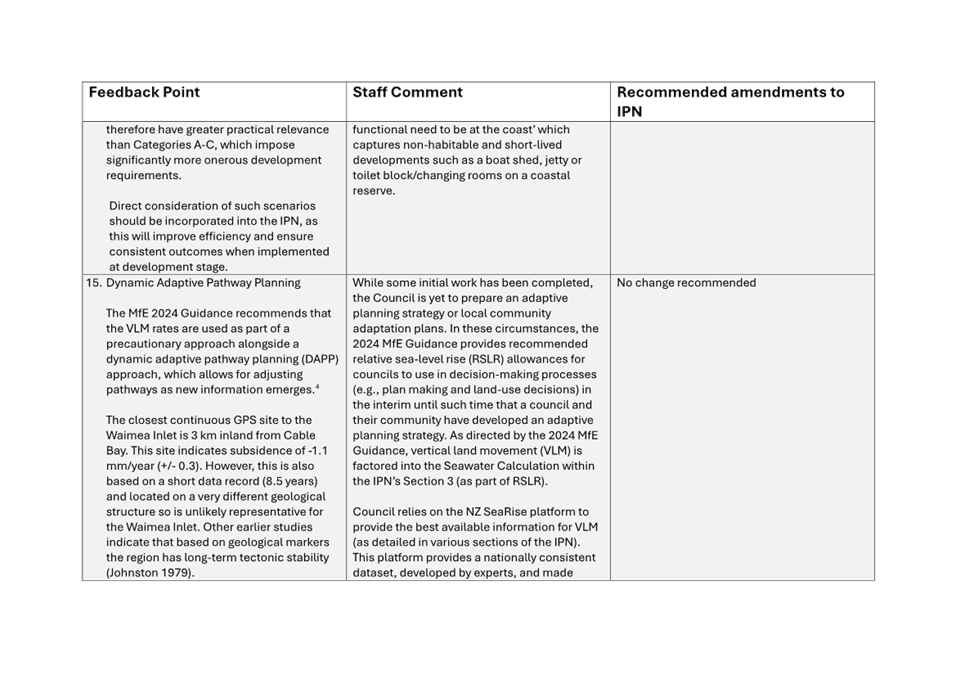

application of MfE guidance’s ‘planning categories’,

uncertainty in use of national vertical land movement data, and adaptive

pathways planning. Staff comments confirmed that the IPN reflects national

guidance, the NZ SeaRise data remains the best information available, and no

local vertical land movement work is planned at this time. No changes are

recommended on these points.

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

Review and feedback process

6.1 Costs for the update to the IPN

and community engagement were met from existing staff and operational budgets.

No additional funding is required to complete the updated Tasman IPN 2026.

Financial implications for the community

6.2 The IPN sets out

the methodology for determining minimum ground and building platform levels to

reduce the risk of inundation. Meeting these levels may involve raising land

or, in some cases, elevating buildings on piles. While such measures add to

construction costs, they need to be weighed against the potentially much higher

costs of repairs and recovery if a property is inundated.

6.3 There is also a

potential financial cost to Council if, following an inundation event, it is

found that Council did not follow national guidance or use the most up‑to‑date

information; applying the IPN helps avoid this potential liability. Having the

IPN 2026 in place therefore reduces future financial risk to Council by

ensuring that decisions are based on current national guidance and the best

available data, providing a clear and defensible basis for managing inundation

hazards.

7.1 The options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Agree to the staff recommended changes

and adopt the amended IPN (see Attachment 2) as the IPN 2026.

|

This option shows that submitter views

have been considered by staff and, where appropriate, amendments have been

made to the IPN.

Provides a clear and defensible basis for

decision-making and reduces Council’s legal and reputational risk.

|

Not every

submission point has been accepted. Some submitters may therefore be

disappointed that their suggestions were not given effect to in the amended

IPN. However, this is part of the feedback process, and not all suggestions

will be deemed appropriate based on staff technical advice.

|

|

2.

|

Adopt the draft IPN 2025 as the final IPN

without amendment, other than the amendments necessary to change the IPN from

a “draft” to the “final” IPN.

|

Provides a clear and defensible basis for

decision-making and reduces Council’s legal and reputational risk.

|

The Council will be open to criticism for

not listening to the community’s views through the public consultation

process, particularly when some valid feedback was provided that can improve

the final version of the IPN.

|

|

3.

|

Do nothing and remain with the 2019 Joint

Nelson Tasman IPN

|

There are no advantages with this option.

|

The 2019 IPN contains outdated data and

is inconsistent with national guidance.

Misalignment with current TDC practice of

applying most update-to-date data to inform building platform and/or land

levels.

Applying the 2019 IPN may understate the

inundation risk, in particular exposing low-lying coastal developments to

inundation earlier than expected (due to not taking

into account national guidance on updated sea-level rise data and vertical

land movement).

Does not provide a clear and defensible

basis for decision-making and increases Council’s legal and

reputational risk.

|

7.2 Option 1 is recommended.

8.1 The IPN is

non-statutory guidance that supports implementation of the RMA, the BA, and

relevant polices and rules in the TRMP. Aligning the IPN with current national

guidance and the best available information provides a clear and defensible

basis for decision-making and reduces Council’s legal and reputational

risk.

8.2 The update to

the IPN has been prepared, and feedback sought and considered in accordance

with the requirements of the Local Government Act 2002.

8.3 On 15 January 2025, the National Policy

Statement for Natural Hazards (NPS-NH) came into force with immediate

application to resource consent decision-making. The

NPS-NH sets out a balanced way for councils to manage natural hazard risks in

new developments, based on the level of risk involved. The

IPN 2026 provides a methodology for mitigating inundation hazards to reduce the

level of risk, consistent with the objective of the NPS-NH.

9. Iwi

Engagement / Whakawhitiwhiti ā-Hapori Māori

9.1 In addition to the broad community

engagement process, feedback on the draft IPN 2025 was directly sought through

the Post Settlement Governance Entities. No feedback was received.

10. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

10.1 Overall, staff consider the decision to adopt the

IPN 2026 is of low/medium significance.

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Low

|

The IPN has been in

place since 2019 and much of the development industry is familiar with the

practice note.

Feedback was sought

from the community and development sector, with amendments made to the IPN to

address feedback points where appropriate.

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Low-Medium

|

The updated IPN may impact on

present or future generations in a minor way, for example the cost of

construction of increased building platform levels will mean higher build

costs which may be passed on through rent and indirect charges from a

business using the building. Conversely the cost of not raising ground or

building platform levels could be considered a negative impact on present or

future generations, if buildings become inundated in future storm events

putting life and property at risk.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Low

|

The IPN can be reviewed at any

time. Future reviews of the IPN could take place following climate change

adaptation work or further updates to national guidance.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

N/A

|

No

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

Low

|

The IPN will not

impact the level of service provided by the Council. The IPN will provide

clarity on Council’s approach to setting minimum ground or building

platforms.

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

Low

|

The IPN will not

impact on Council’s debt, level of rates charged or Council’s

financial capacity.

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

N/A

|

N/A

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

N/A

|

N/A

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

N/A

|

N/A

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

Low

|

The IPN does not

require particular considerations relating to TMOTW.

|

11. Communication

/ Whakawhitiwhiti Kōrero

11.1 Consultation on the

proposed update has been completed (as detailed in Sections 4 and 9), and minor

amendments to the IPN are recommended in response to the feedback received. The

five stakeholders who provided feedback have been made aware of this report and

the proposed responses to their feedback.

11.2 Following adoption of the IPN 2026, the website will be updated and

the IPN made available. Stakeholders will be informed of the update through

emails and sector newsletters.

12.1 There is an ongoing risk

that developers and landowners will see the IPN 2026 causing increased costs

due to higher building platform or ground level requirements (as a result of

national guidance regarding sea-level rise). However, this risk can be effectively

mitigated through proactive engagement with the development sector, coupled

with clear communication that highlights the long-term benefits of resilience,

including reduced recovery costs and enhanced sustainability of developments.

12.2 Adoption of the IPN 2026

reduces Council’s legal and reputational liability by ensuring that

decisions on minimum ground and building platform levels are based on the most

up‑to‑date national guidance and best available technical

information, providing a clear and defensible basis for resource and building

consent decisions. By applying the updated IPN, the Council avoids the

potential future costs and liability that could arise if developments are

affected by inundation and it is found that Council did not follow current

guidance or use the best information available.

13. Climate

Change Considerations / Whakaaro

Whakaaweawe Āhuarangi

13.1 Adopting the IPN 2026 strengthens Tasman’s

ability to manage, adapt and respond to climate related risks. The Tasman

Climate Action Plan (2024-2027) has a short-term action 2(a)(ii) for regulatory

activities (resource and building consenting) to continue to account for

inundation and sea level rise based on Ministry for the Environment guidance

and apply the 'Inundation Practice Note’ for setting minimum ground and

floor levels for subdivision, new buildings, and major alterations. Updating

the IPN document is in accordance with the Tasman Climate Action Plan.

14. Alignment

with Policy and Strategic Plans / Te Hangai ki ngā aupapa Here me ngā

Mahere Rautaki Tūraru

14.1 Adoption of the IPN 2026 supports the Long-Term

Plan’s strategic priorities, particularly ‘Strong resilient and

inclusive communities’, and ‘Enabling positive and sustainable

development’.

14.2 Numerous provisions in the TRMP require natural

hazard considerations. The IPN 2026 provides a methodology and approach to

setting appropriate resilient ground and building platform levels to mitigate

the effects of natural hazards. The IPN 2026 also assists with the

Council’s administration of the Building Act 2004 by providing the

methodology and approach for determining whether a hazard notice is required

for a development.

15. Conclusion

/ Kupu Whakatepe

15.1 The IPN is a standardised

methodology to determine minimum ground and/or building platform levels for

development exposed to inundation (freshwater and coastal). It is an important

tool to assist in mitigating inundation hazards.

15.2 Consultation on the

proposed update has now been completed and minor amendments to the IPN are

recommended in response to the feedback received.

15.3 Council consideration and adoption of the IPN 2026

is now required to complete the process.

16. Next

Steps and Timeline / Ngā Mahi Whai Ake

16.1 Following adoption of the IPN 2026, the website will be updated and

the IPN made available. Stakeholders will be informed of the update through

emails and sector newsletters.

|

1.⇩

|

Tasman

Inundation Practice Note 2026

|

73

|

|

2.⇩

|

Feedback

received, staff responses and recommended amendments to IPN

|

117

|

Strategy Finance and

Performance Committee Agenda – 19 March 2026

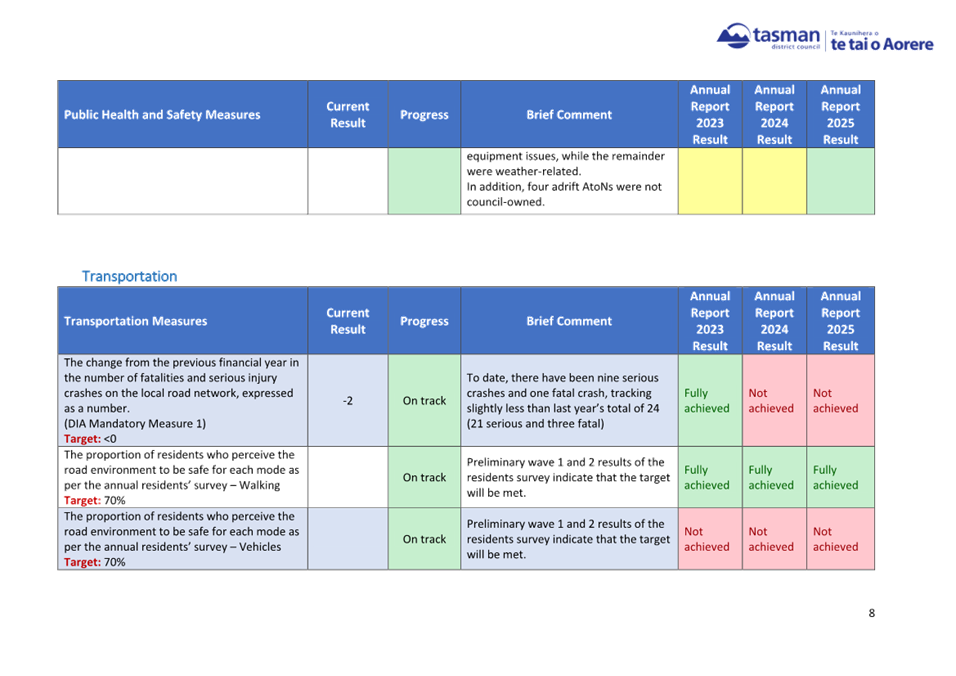

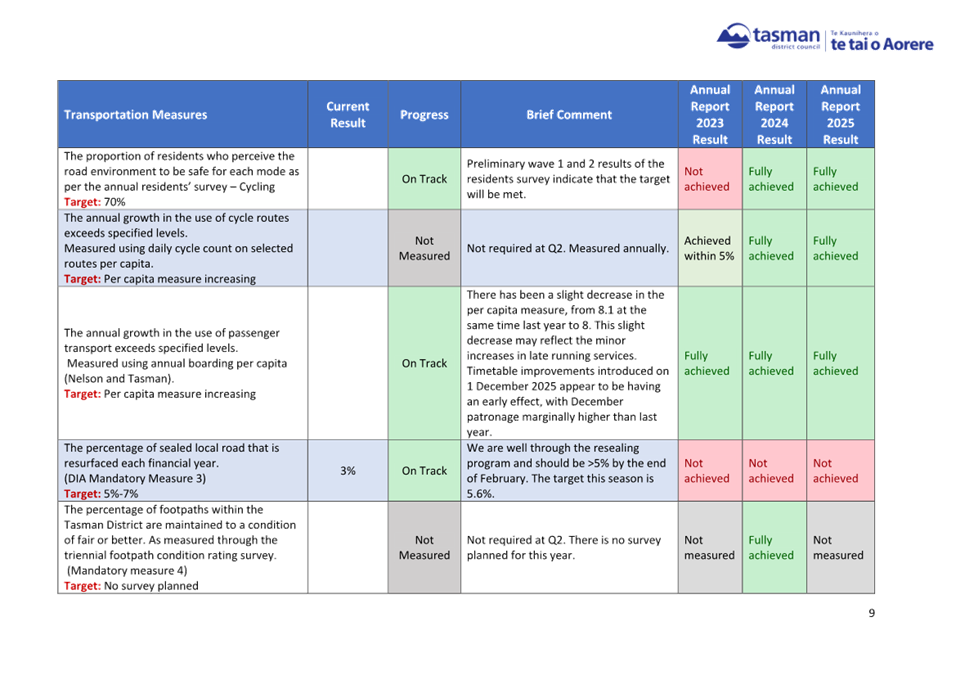

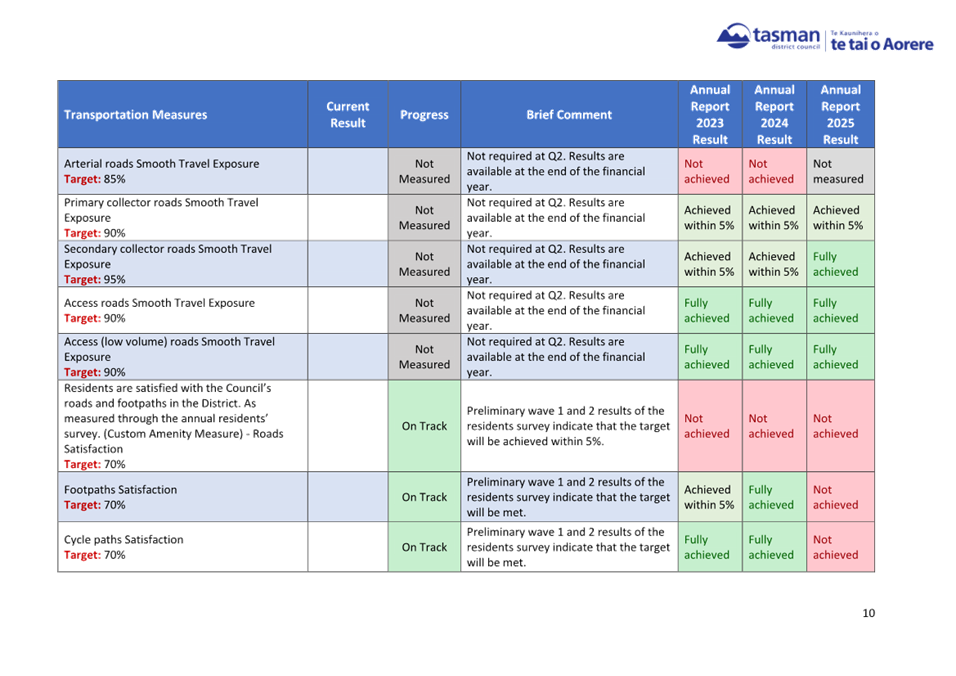

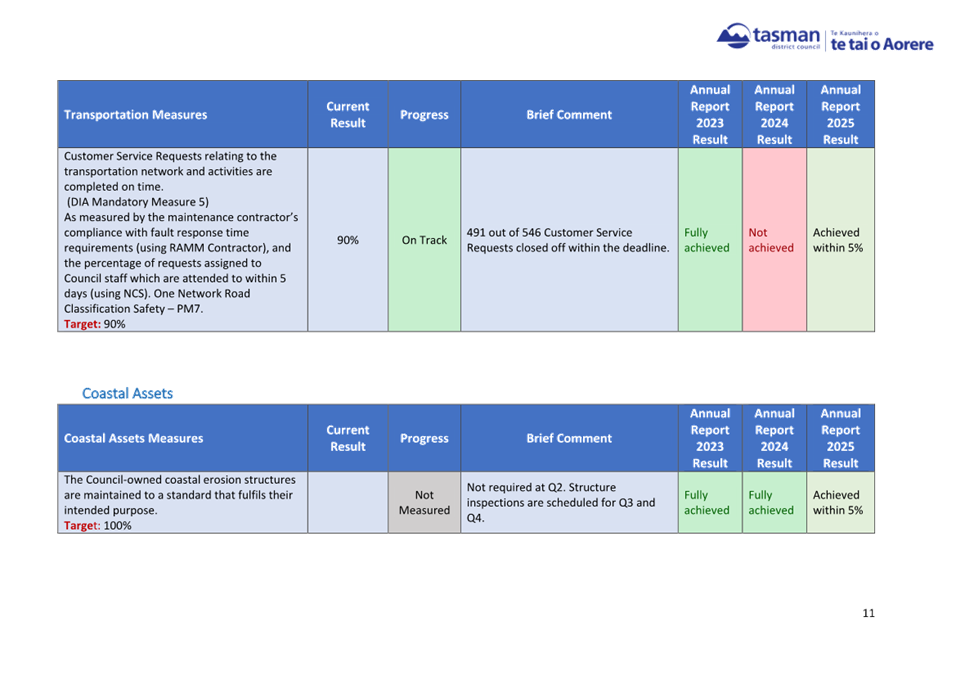

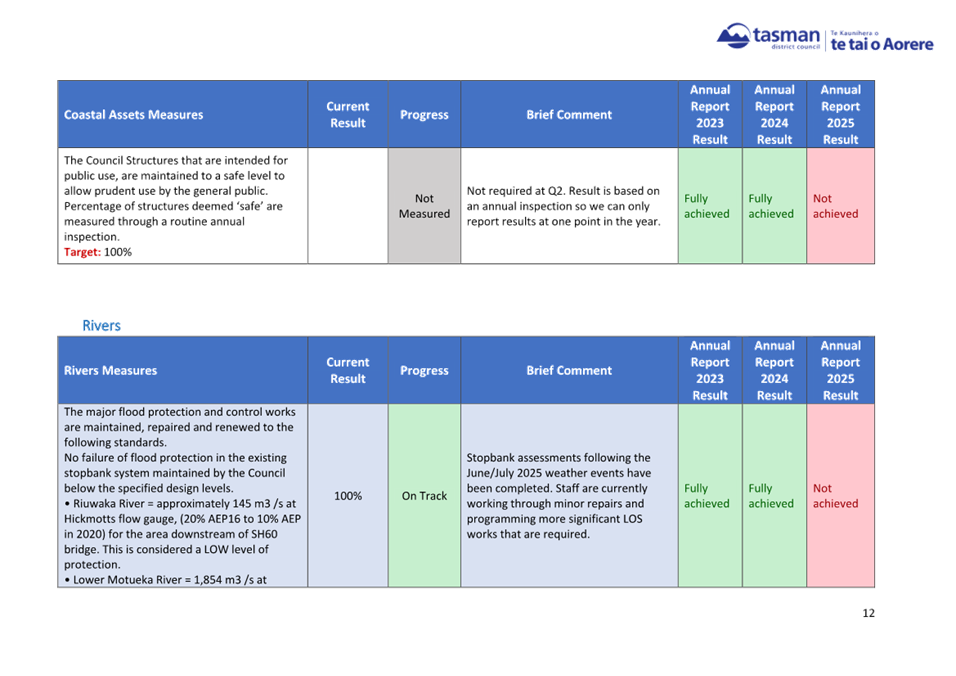

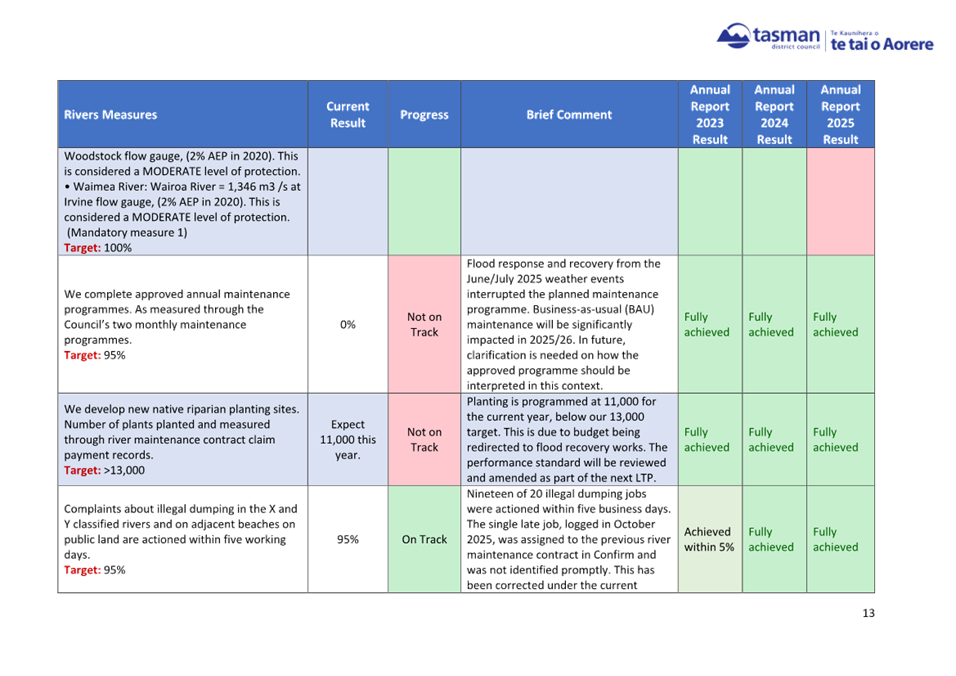

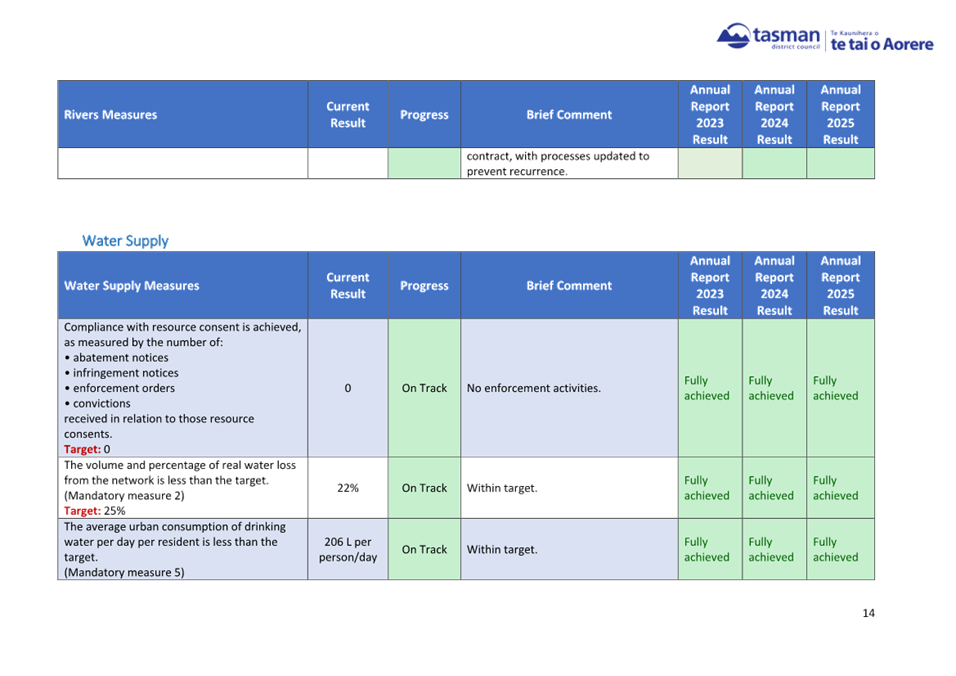

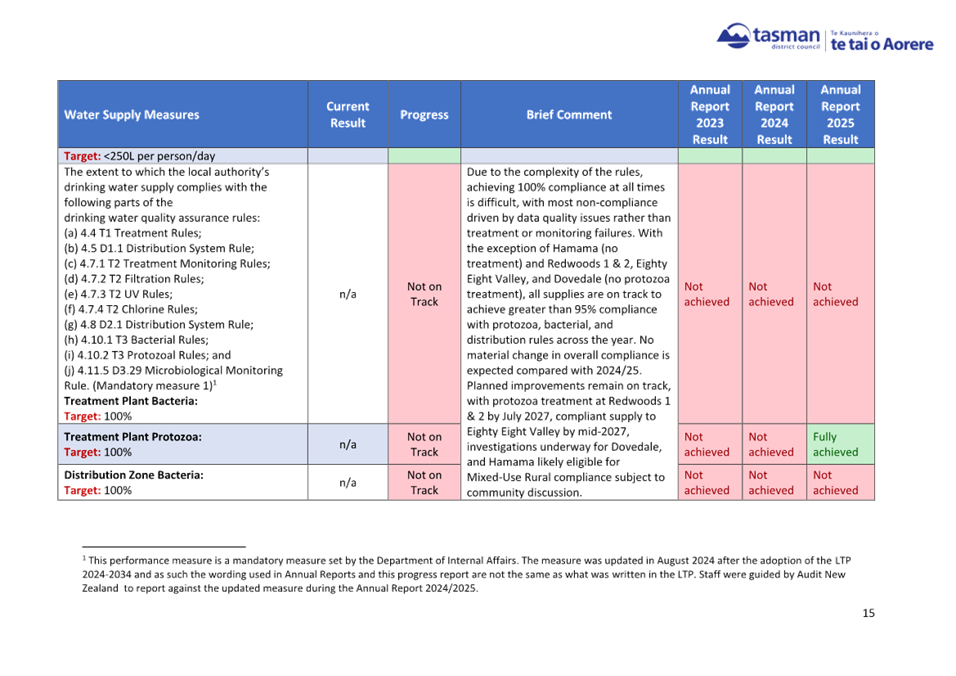

7.5 Six-Month Performance Measure Progress Report

2025/2026

Information Only - No Decision

Required

|

Report

To:

|

Strategy

Finance and Performance Committee

|

|

Meeting

Date:

|

19

March 2026

|

|

Report

Author:

|

Emily

Garland, Graduate Community Policy Advisor

|

|

Report

Authorisers:

|

Sue

McLean, Kaiwhakahaere ā Rōpū – Te Pae Rautaki Ahumoni |

Group Manager - Strategy & Finance

|

|

Report

Number:

|

RSFP26-03-3

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 This

report summarises the six-month progress (July to

December 2025) against the Levels of Service Performance Measures set in

Tasman’s 10-Year Plan 2024-2034 (LTP). The

Council measures its service performance each year using a core set of

indicators set in the LTP.

1.1 As this is the six-month progress,

results are indicative of the Council’s Performance Measure results only

for 2025/2026. The final results will be presented in the Annual Report

2025/2026, scheduled to be adopted in October 2026.

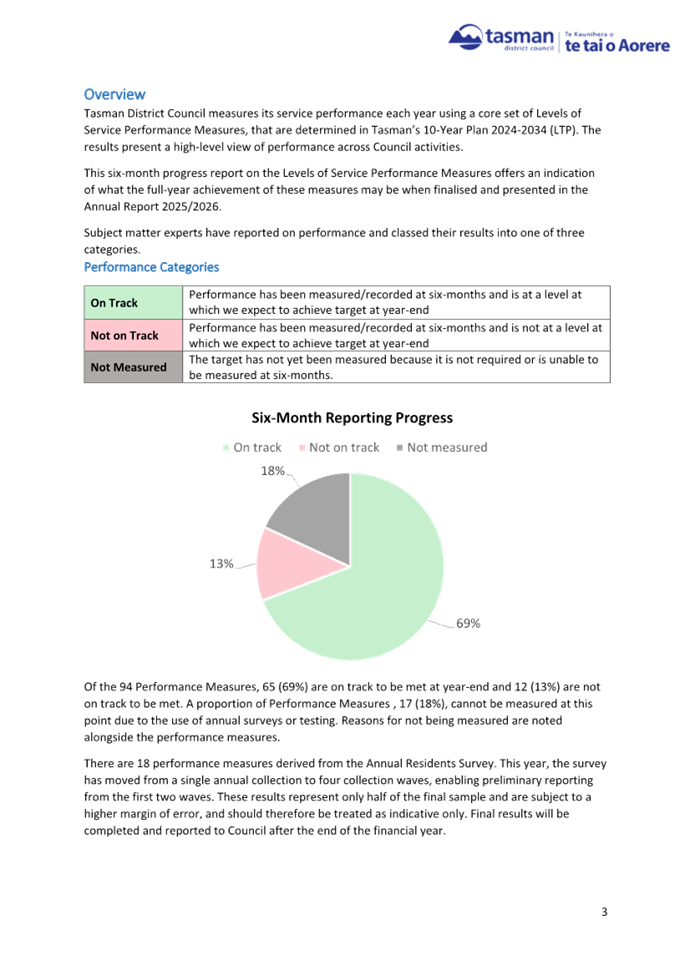

1.2 Of the 94 Performance Measures, 65 (69%)

are on track to be met by year end, and 12 (13%) are not on track to be met. A

proportion of Performance Measures, 17 (18%), cannot be measured at this point

due to the use of annual surveys or testing.

1.3 The full Progress Report is provided in Attachment

1.

2. Recommendation/s

/ Ngā Tūtohunga

That the Strategy Finance and Performance Committee

1. receives the Six-Month Performance Measure Progress Report

2025/2026 RSFP26-03-3.

3.1 Relevant

staff have reported on the progress in achieving their Performance Measure

targets, set in LTP 2024-2034.

3.2 Staff

were asked to classify performance in one of three categories:

3.2.1 On Track - Performance has been measured at six months

and is at a level where the target is expected to be achieved by year end.

3.2.2 Not on Track - Performance has been measured at six

months and is not at a level where the target is expected to be achieved by

year end.

3.2.3 Not Measured - The target has not yet been measured, as

it is either not required or cannot be measured at the six-month point.

3.3 As this is an interim report,

results are indicative only of Council’s Performance Measure outcomes for

2025/2026. Final results will be reported through the Annual Report 2025/2026,

scheduled for adoption in October 2026.

3.4 Of the 94 Performance Measures, 65 (69%)

are on track to be met and 12 (13%) are not on track at this point in the year.

A further 17 measures (18%) are unable to be measured at six months due to

their reliance on annual surveys[1]

or testing. These reasons are noted within the full Progress Report in Attachment

1.

3.5 The

12 measures that are currently not on track are primarily due to weather

impacts, resourcing pressures, and regulatory complexity. Staff are monitoring

these measures and intervening where possible.

3.6

By comparison, of the 94 measures in the Annual Report

2024/2025, Council fully achieved or achieved within 5% a total of 70

Performance Measures (74%). Twenty‑two measures (23%) were

not achieved, and two were unable to be measured.

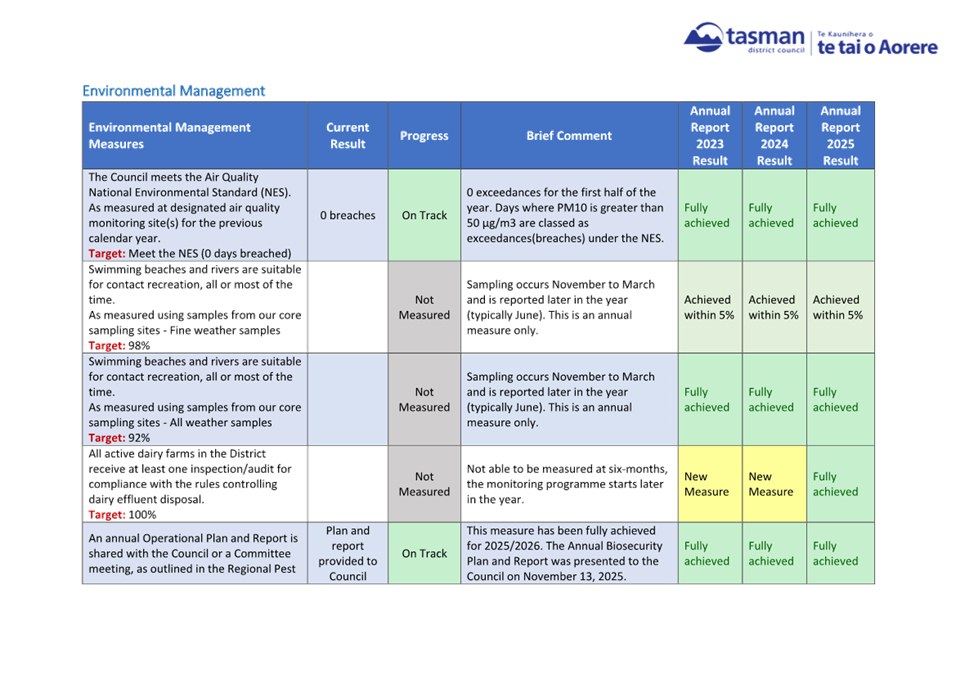

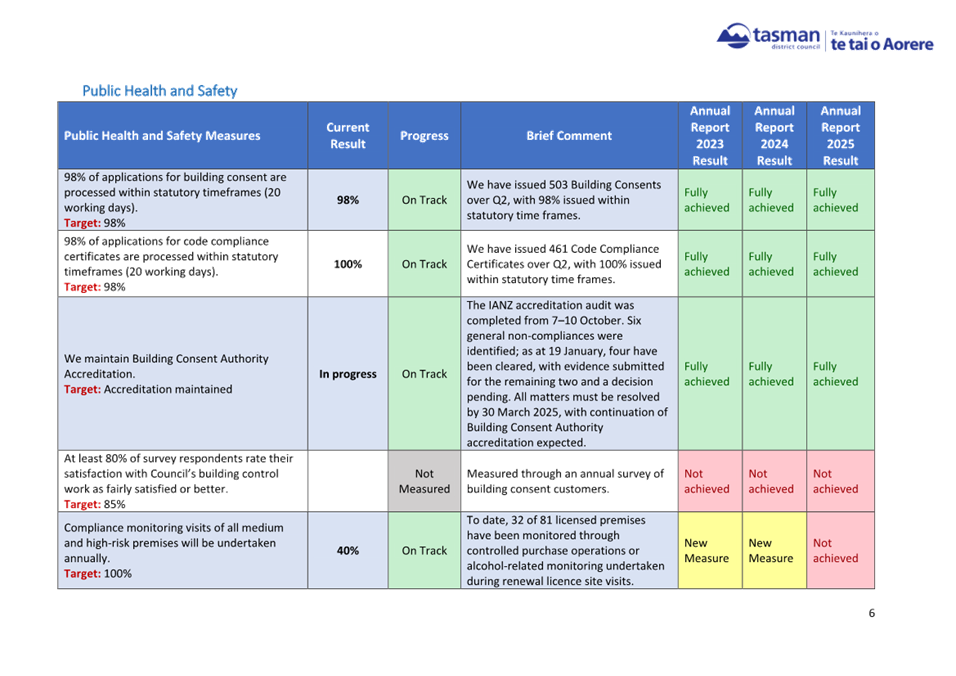

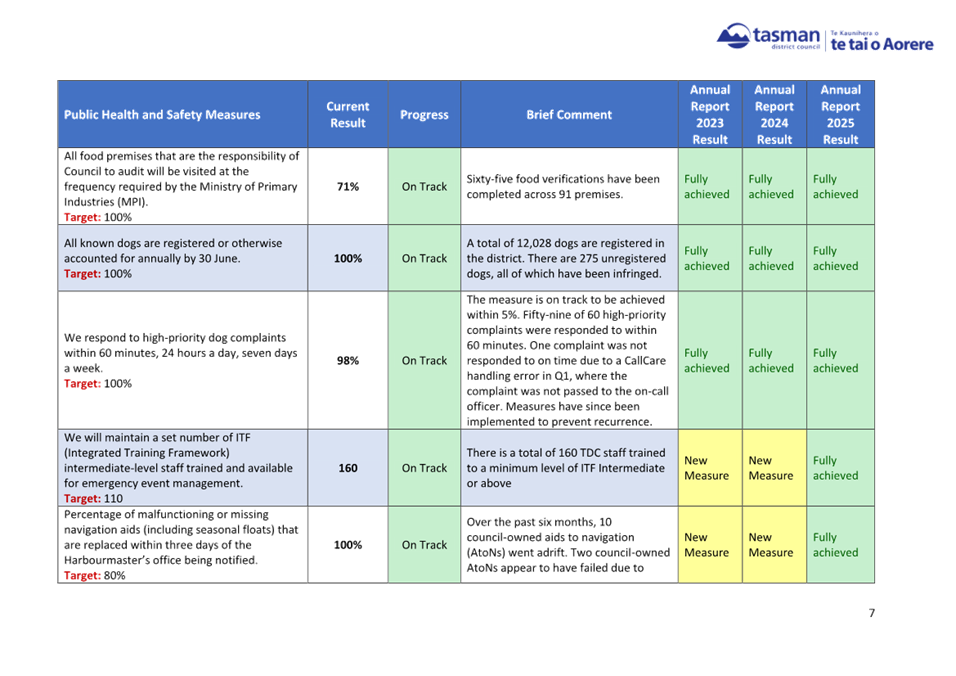

4. Measures

Not Meeting Target

4.1 Twelve Performance Measures are not on

track to be met. These are outlined in the following table by Group of

Activity:

|

Performance

Measure

|

Current

Result

|

Progress

|

Brief

Comment

|

AR 2025

Result[2]

|

|

Environmental

Management

|

|

Consent applications are

processed within statutory timeframes (where

they exist) - Non-notified consents

Target: 100%

|

71%

|

Not on Track

|

This is a slight decrease

from Q1 (79%), which was anticipated due to delays in allocating consents to

planners. Performance remains consistent with previous years, and the

appointment of two new senior planners in March is expected to improve

results going forward.

|

Not

achieved

|

|

Consent applications are

processed within statutory timeframes (where

they exist) - Limited notified consents

Target: 100%

|

0%

|

Not on Track

|

One limited‑notified

decision was issued in Q2 and was partly granted, with no appeals. Due to its

complexity and a two‑day hearing, the consent did not meet statutory

timeframes.

|

Not

achieved

|

|

Rivers

|

|

We complete

approved annual maintenance programmes. As measured through the

Council’s two monthly maintenance programmes.

Target: 95%

|

0%

|

Not on Track

|

Flood

response and recovery from the June/July 2025 weather events disrupted the

planned maintenance programme, which will not be completed as scheduled.

Maintenance activity is now focused on recovery in affected areas. The annual

maintenance programme was completed in each of the previous three financial

years.

|

Fully

achieved

|

|

We develop

new native riparian planting sites. Number of plants planted and measured

through river maintenance contract claim payment records.

Target: >13,000

|

Expect 11,000

this year.

|

Not on Track

|

Planting is

programmed at 11,000 for the current year, below our 13,000 target. This is

due to budget being redirected to flood recovery works. The performance

standard will be reviewed and amended as part of the next LTP.

|

Fully

achieved

|

|

Water Supply

|

|

The extent to

which the local authority’s drinking water supply complies with the

following parts of the

drinking

water quality assurance rules:

(a) 4.4 T1

Treatment Rules;

(b) 4.5 D1.1

Distribution System Rule;

(c) 4.7.1 T2

Treatment Monitoring Rules;

(d) 4.7.2 T2

Filtration Rules;

(e) 4.7.3 T2

UV Rules;

(f) 4.7.4 T2

Chlorine Rules;

(g) 4.8 D2.1

Distribution System Rule;

(h) 4.10.1 T3

Bacterial Rules;

(i) 4.10.2 T3

Protozoal Rules; and

(j) 4.11.5

D3.29 Microbiological Monitoring Rule. (Mandatory measure 1)[3]

Treatment

Plant Bacteria:

Target: 100%

|

n/a

|

Not on Track

|

Due to the

complexity of the rules, achieving 100% compliance at all times is difficult,

with most non‑compliance driven by data quality issues rather than

treatment or monitoring failures. With the exception of Hamama (no treatment)

and Redwoods 1 & 2, Eighty Eight Valley, and Dovedale (no protozoa

treatment), all supplies are on track to achieve greater than 95% compliance

with protozoa, bacterial, and distribution rules across the year. No material

change in overall compliance is expected compared with 2024/25. Planned

improvements remain on track, with protozoa treatment at Redwoods 1 & 2

by July 2027, compliant supply to Eighty Eight Valley by mid‑2027,

investigations underway for Dovedale, and Hamama likely eligible for Mixed‑Use

Rural compliance subject to community discussion.

|

Not

achieved

|

|

Treatment

Plant Protozoa:

Target: 100%

|

n/a

|

Not on Track

|

Fully

achieved

|

|

Distribution

Zone Bacteria:

Target: 100%

|

n/a

|

Not on Track

|

Not

achieved

|

|

Planned

service interruptions do not exceed 8 hours, as required by section 25 (4) of

the Water Services Act 2021.

As measured through the Maintenance Contract reporting.

Target: <8 hours

|

8.2 hours

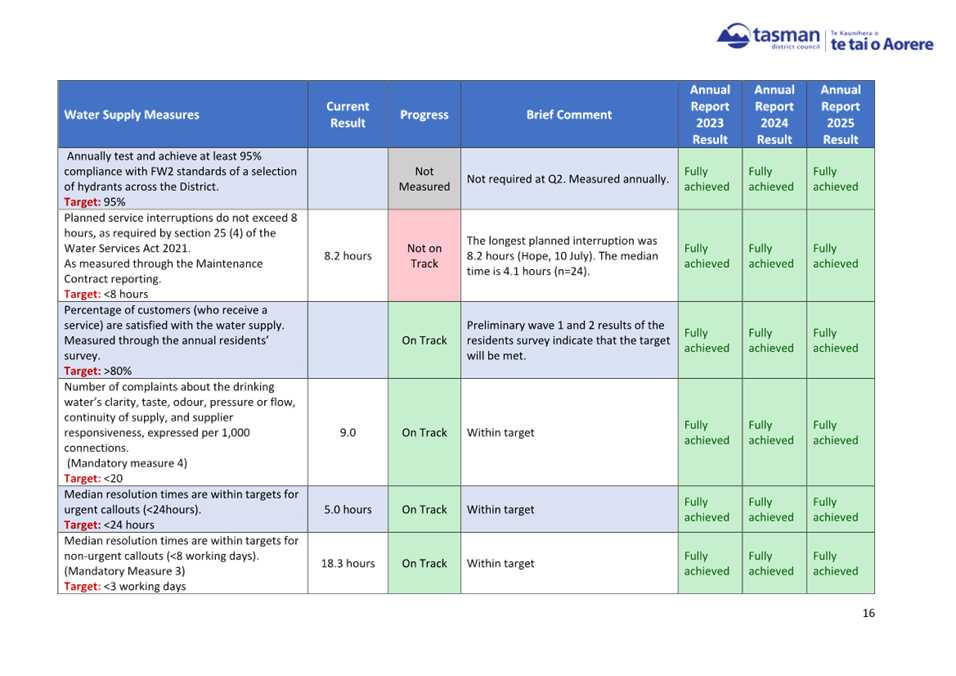

|

Not on Track

|

The longest

planned interruption was 8.2 hours (Hope, 10 July). The median time is 4.1

hours (n=24).

|

Fully

achieved

|

|

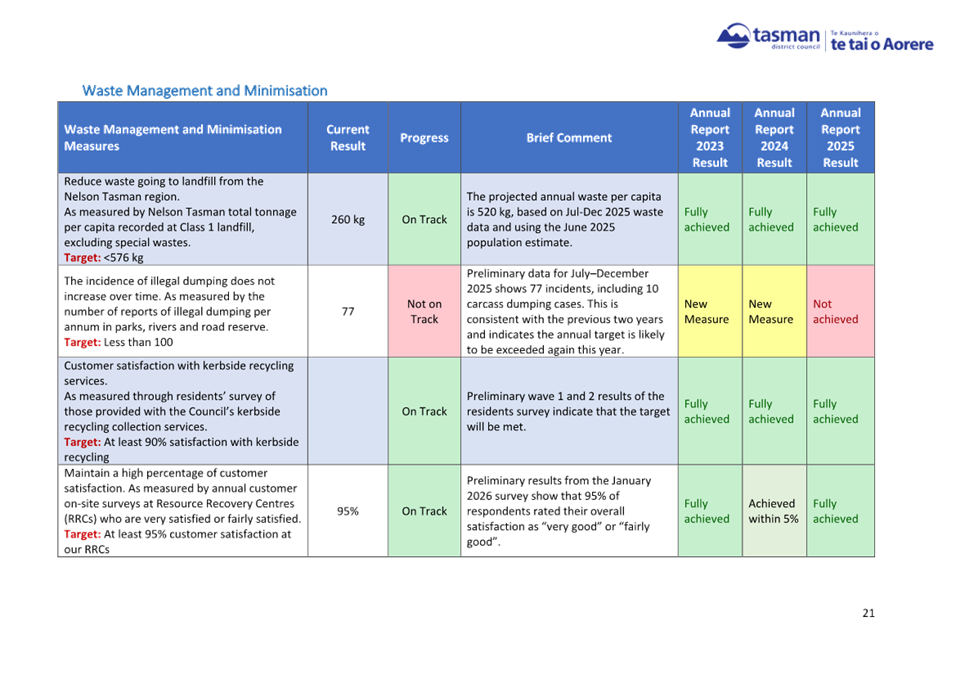

Waste

Management and Minimisation

|

|

The incidence of illegal