Audit and Risk

Committee

Agenda – 01 October 2025

6 Reports

6.1

Risk and Assurance

Information Only - No Decision

Required

|

Report

To:

|

Audit

and Risk Committee

|

|

Meeting

Date:

|

1

October 2025

|

|

Report

Author:

|

Amy

Clarke, Acting Assurance & Improvement Manager

|

|

Report

Authorisers:

|

Joanna

Cranness, People and Wellbeing Manager

|

|

Report

Number:

|

RFNAU25-10-1

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 This report and

attachments outline key risk and assurance activities for Q1 2025/26. Strategic

risks remain prominent, with financial sustainability rated Very High and

recent flooding events underscoring the interconnected nature of

Council’s risk profile.

1.2 Assurance

activities focused on governance and service delivery, with audits such as the

Harakeke CRM review identifying both strengths and areas for improvement.

1.3 A refreshed

reporting format now supports clearer tracking of progress and challenges

across Council’s risk and assurance landscape.

2. Recommendation/s

/ Ngā Tūtohunga

That the Audit and

Risk Committee

1. receives the Risk and Assurance report RFNAU25-10-1.

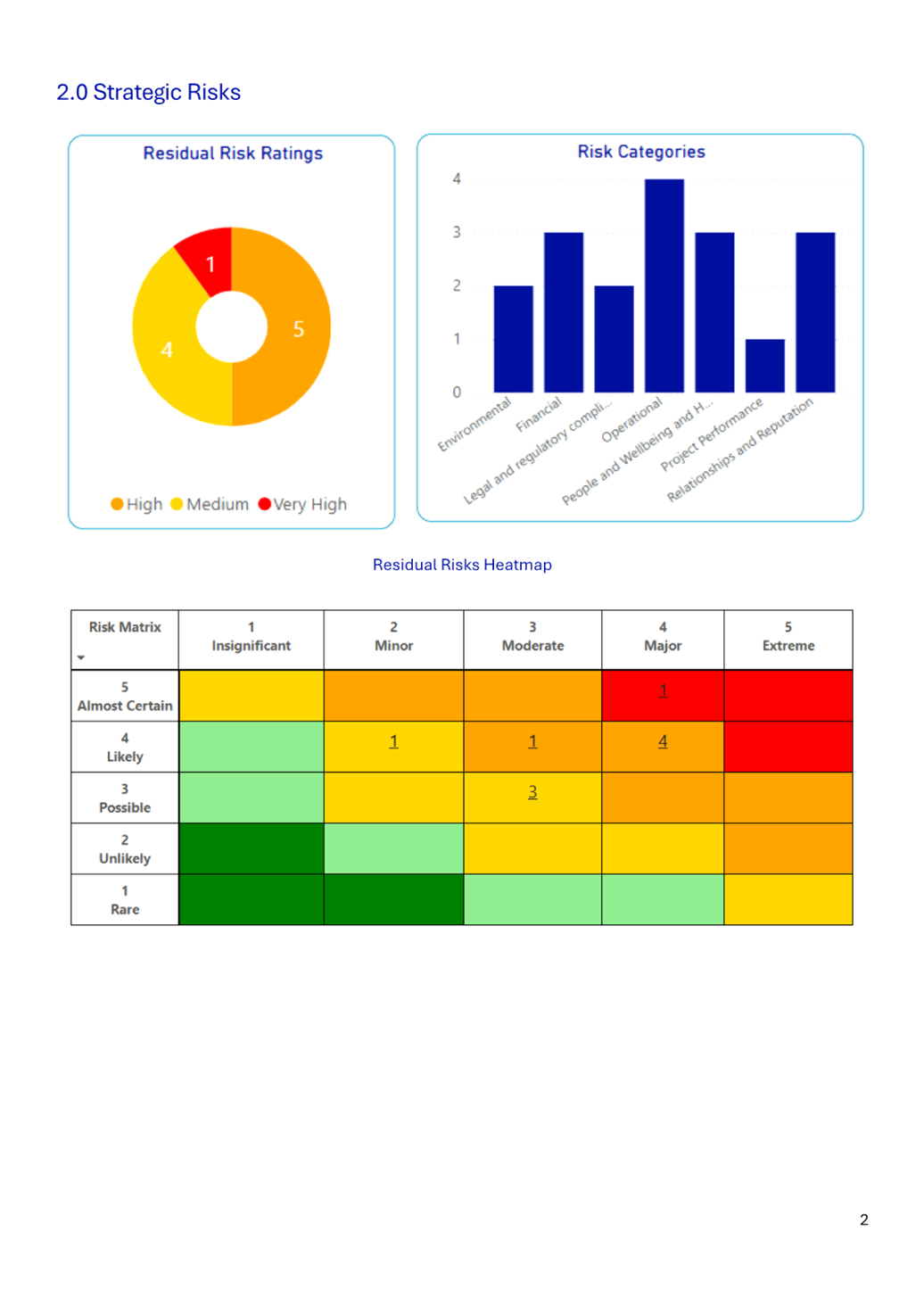

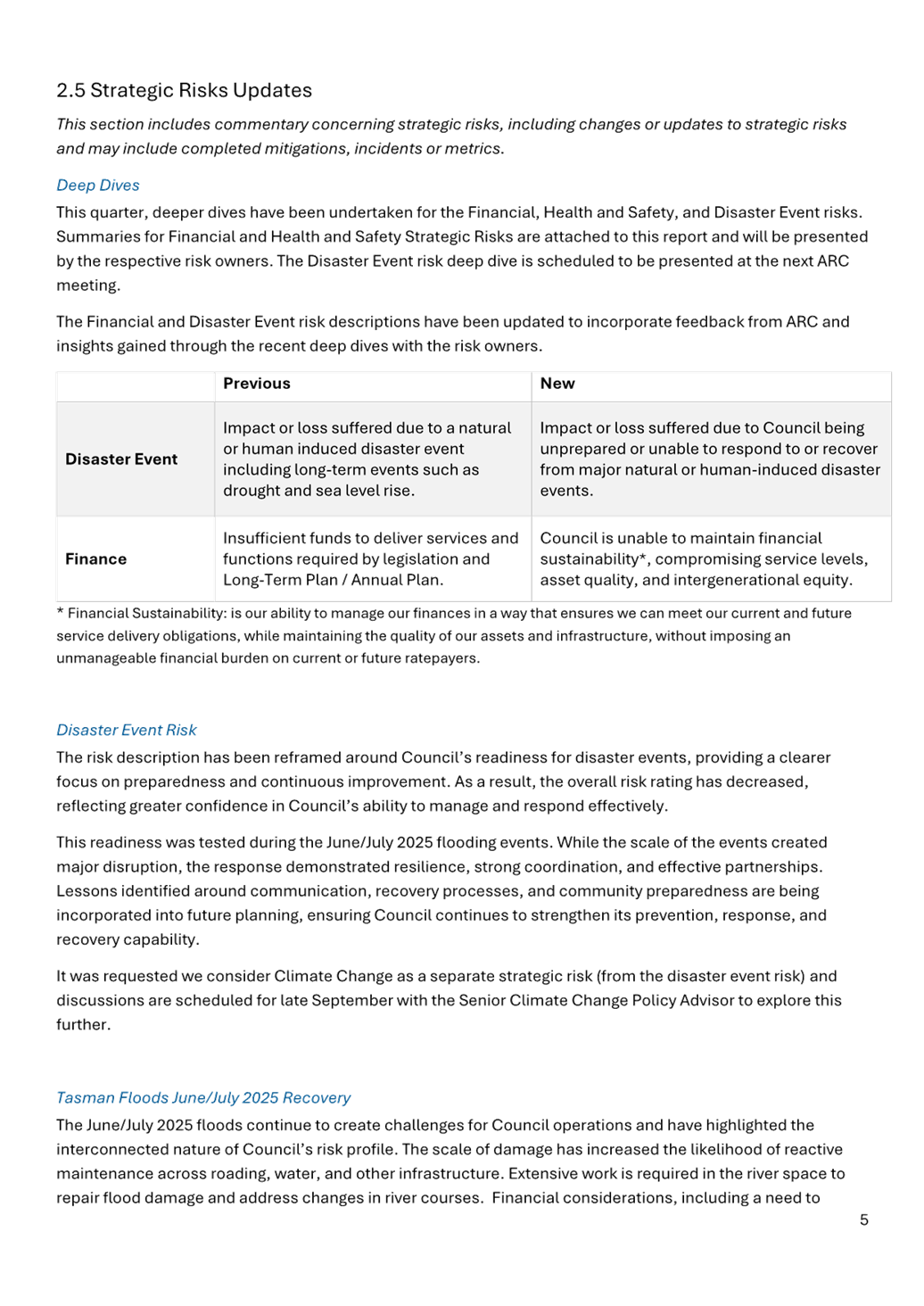

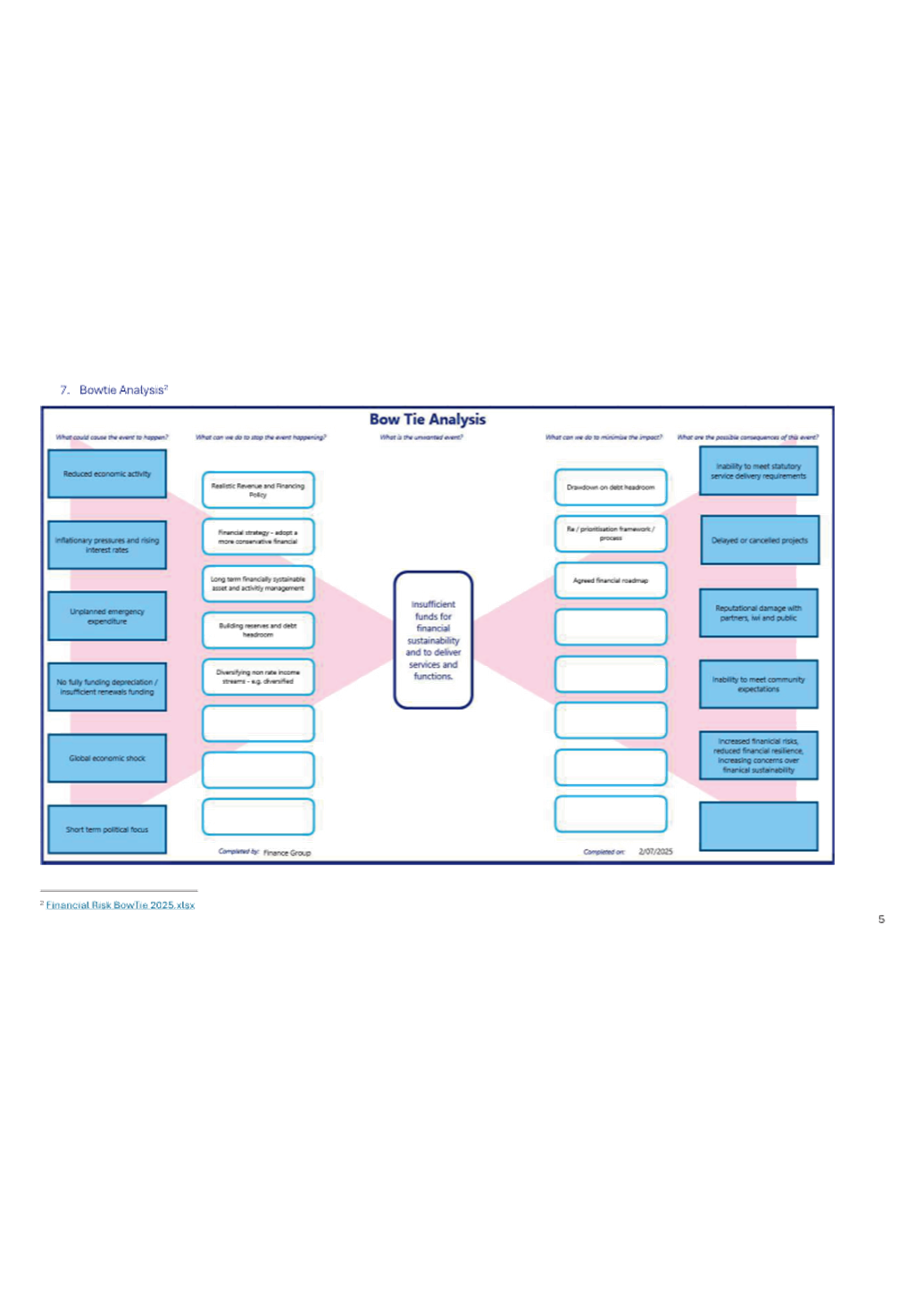

3.1 The Quarterly Risk Report (Attachment

1) for Q1 2025/26 highlights the continued prominence of strategic risks,

particularly financial sustainability, which remains rated as Very High. The

June/July 2025 flooding events were a defining feature of the quarter, testing

Council’s disaster preparedness and highlighting the interconnected

nature of strategic and operational risks. These events have led to increased

infrastructure maintenance needs, financial strain, and broader economic

disruption, reinforcing the importance of resilience-building and sustainable

recovery planning.

3.2 Operational

risks also remain significant. The report notes that many risks are

longstanding and increasingly interlinked, with external stressors such as

extreme weather amplifying vulnerabilities.

3.3 Additionally,

the report introduces improvements in risk reporting through SharePoint and

Power BI, aiming to enhance transparency and reduce manual processes. A

strategic risk review and further deep dives are planned to support ongoing

maturity in risk management.

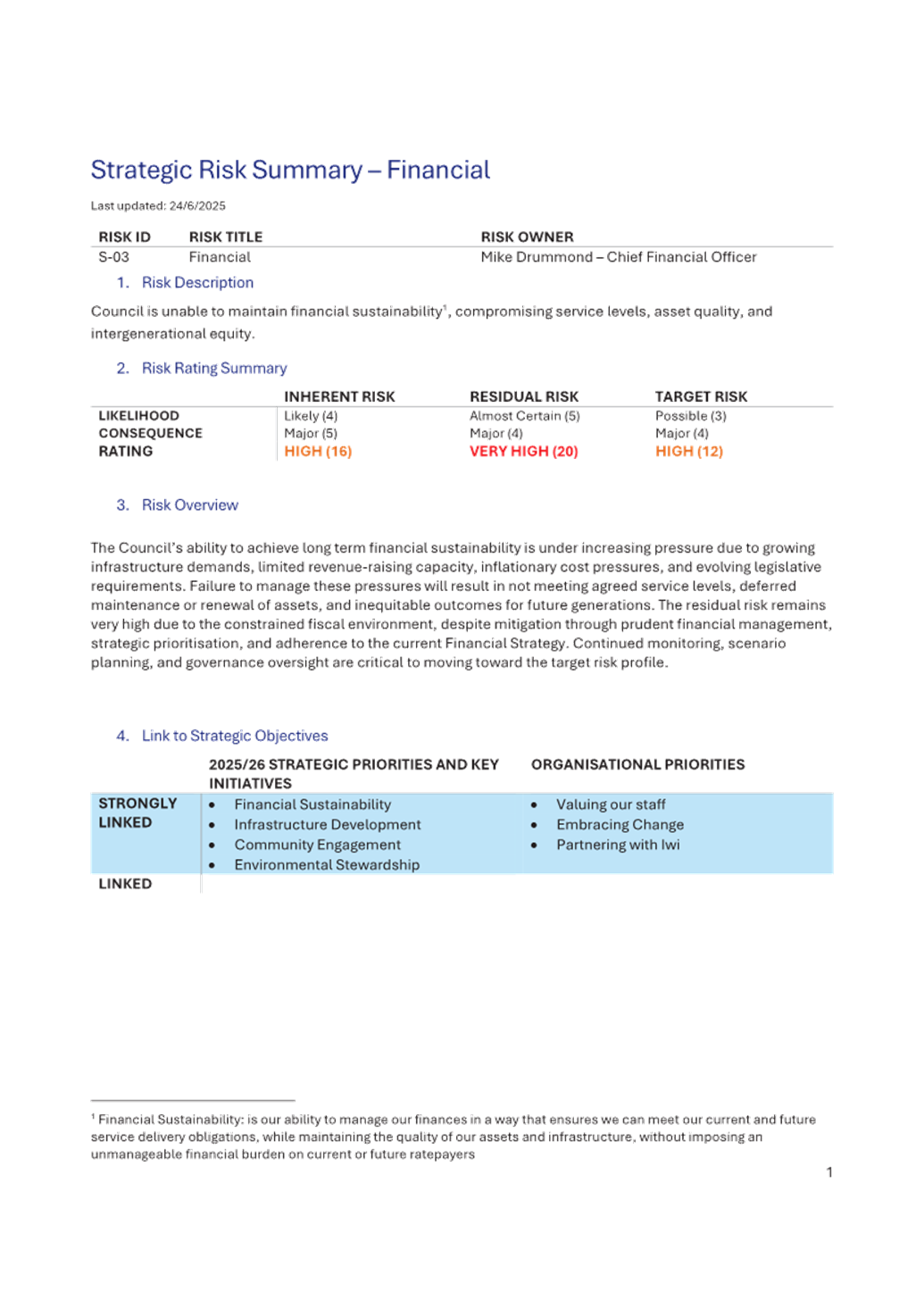

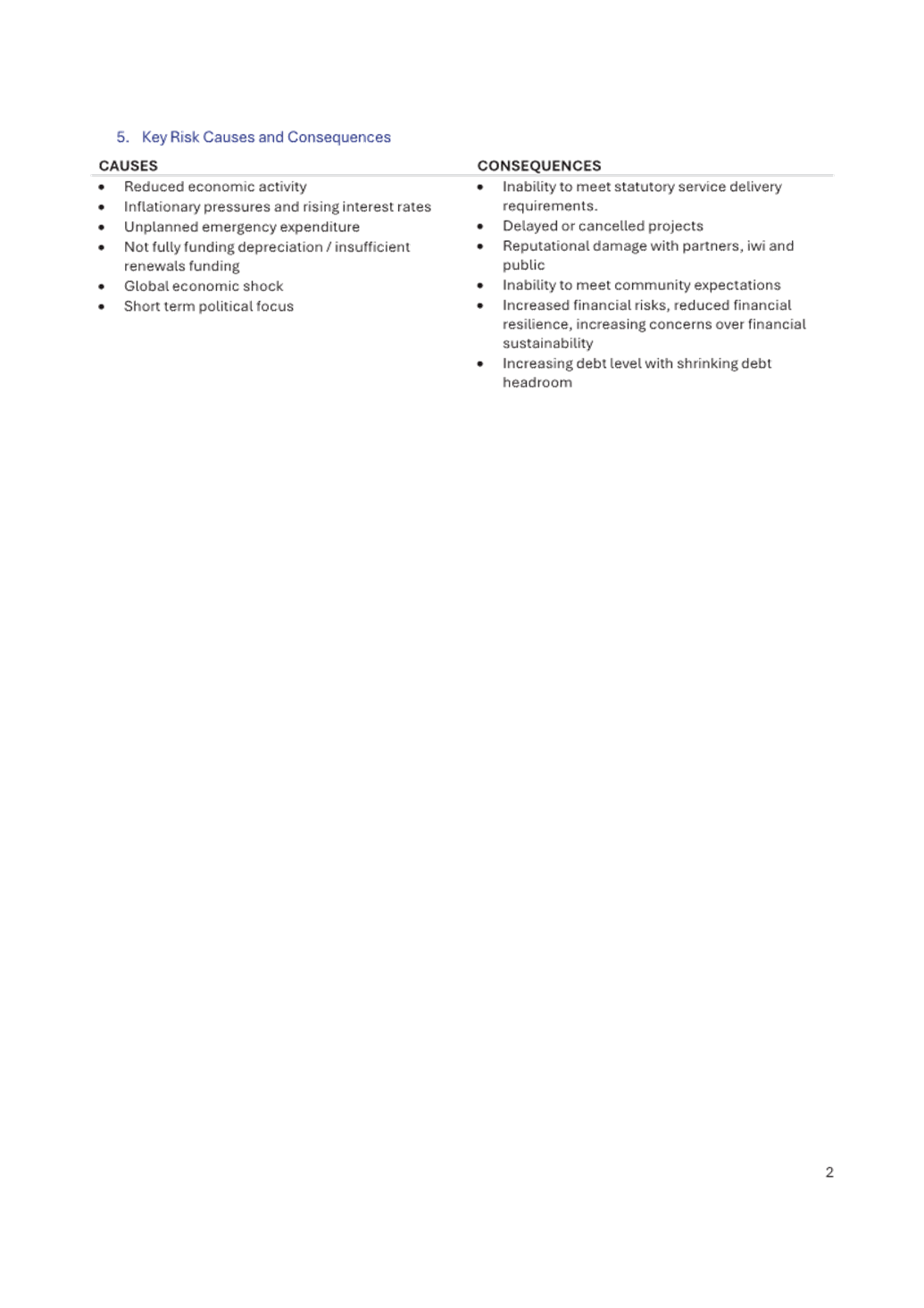

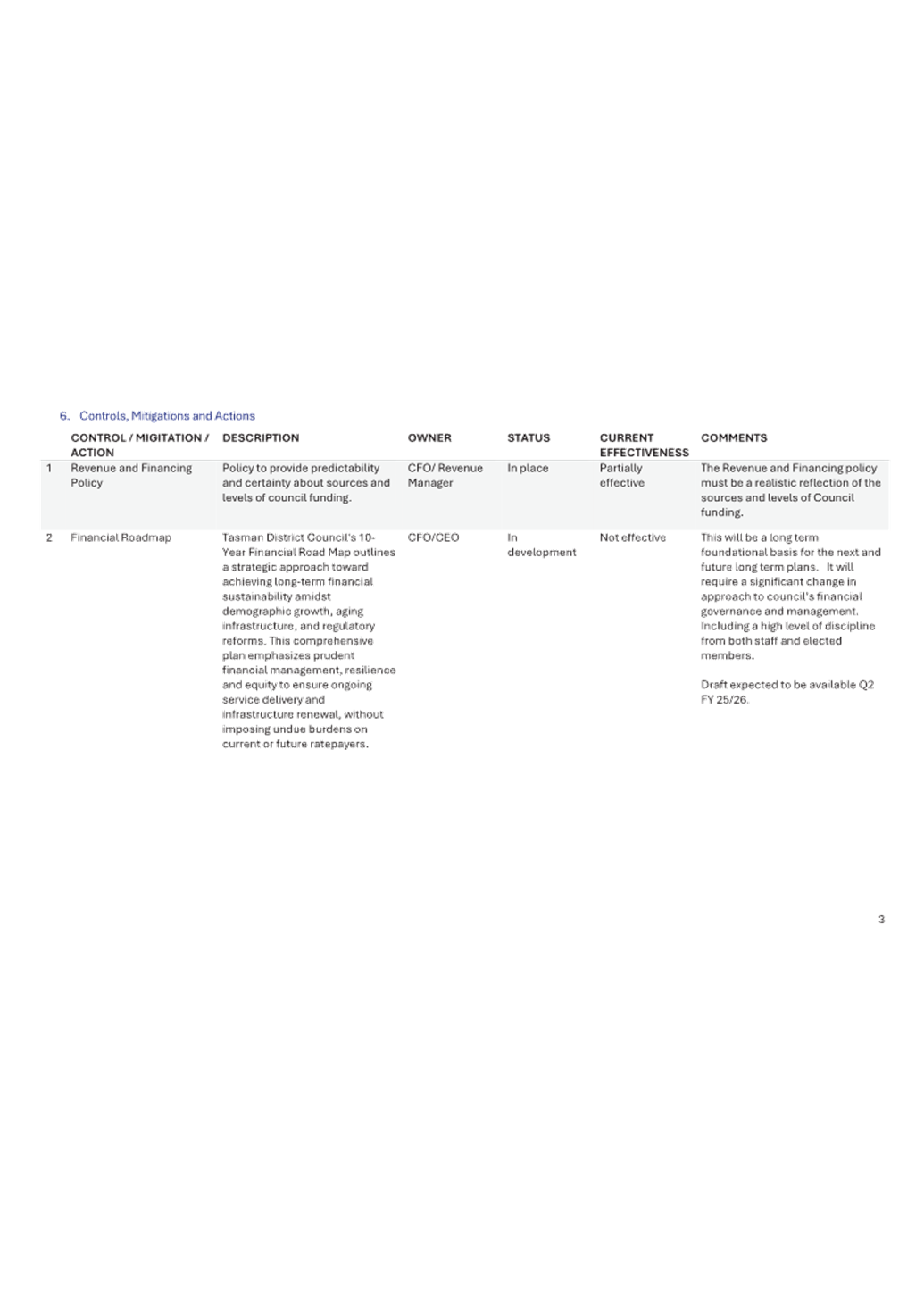

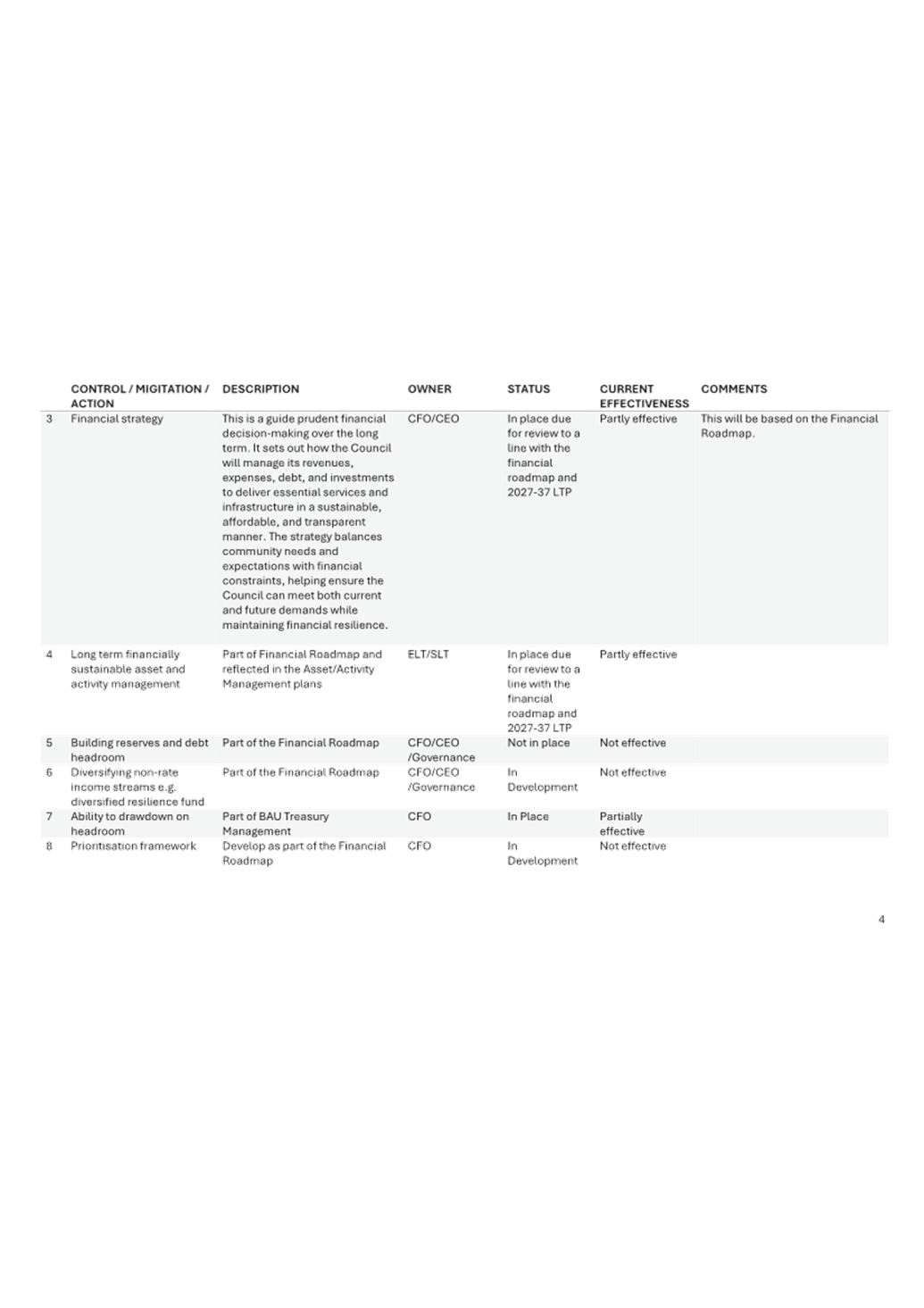

4. Strategic Risks Deep Dives

4.1 In response to a request from the Audit

and Risk Committee, Strategic Risk Owners have been invited to attend ARC

meetings to present and discuss their respective risks. This quarter, the focus

will be on the Financial Strategic Risk (Attachment 2) and Health and

Safety Strategic Risk (Attachment 3). Summaries of each are attached to

provide additional context and background.

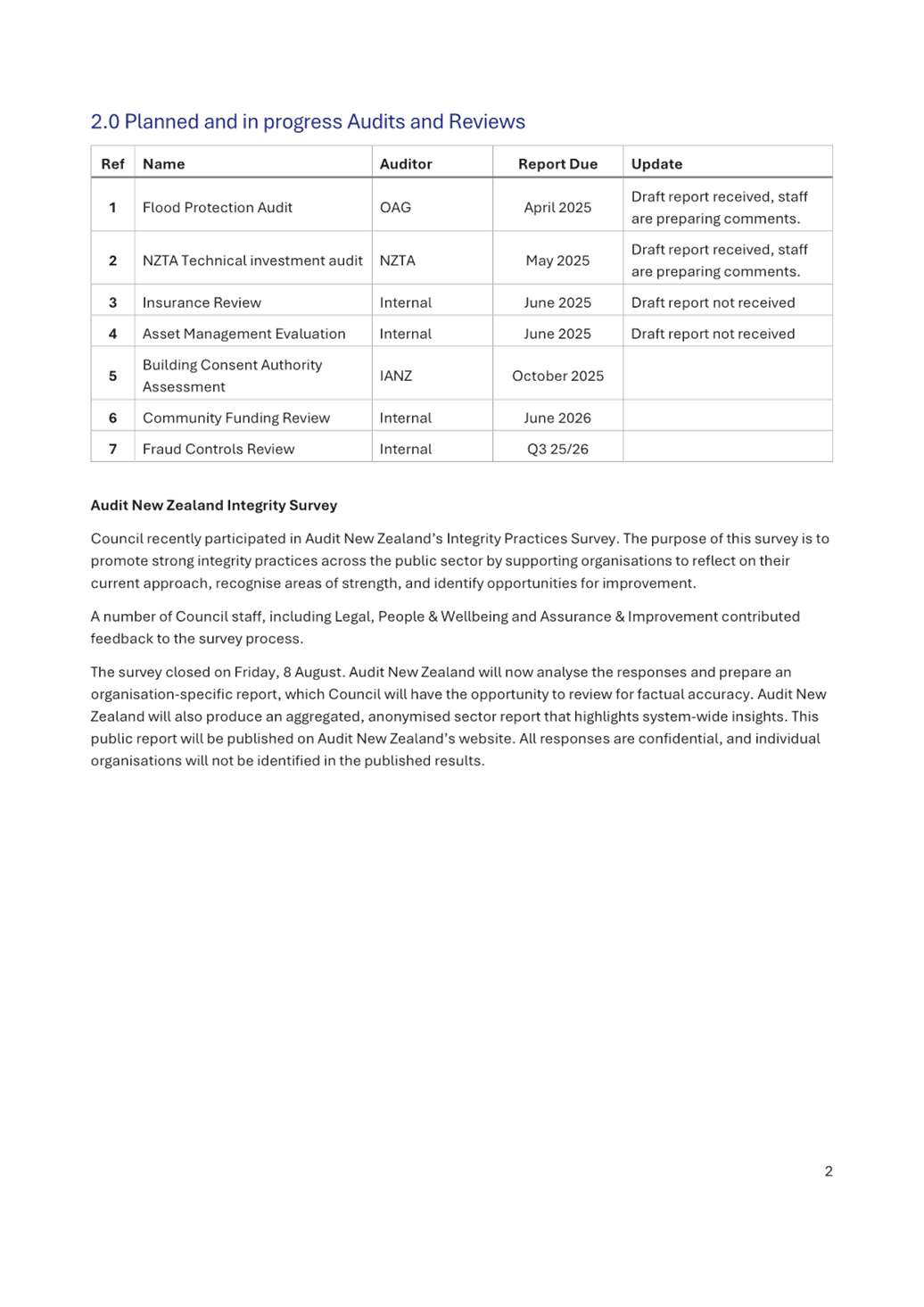

5.1 The Quarterly

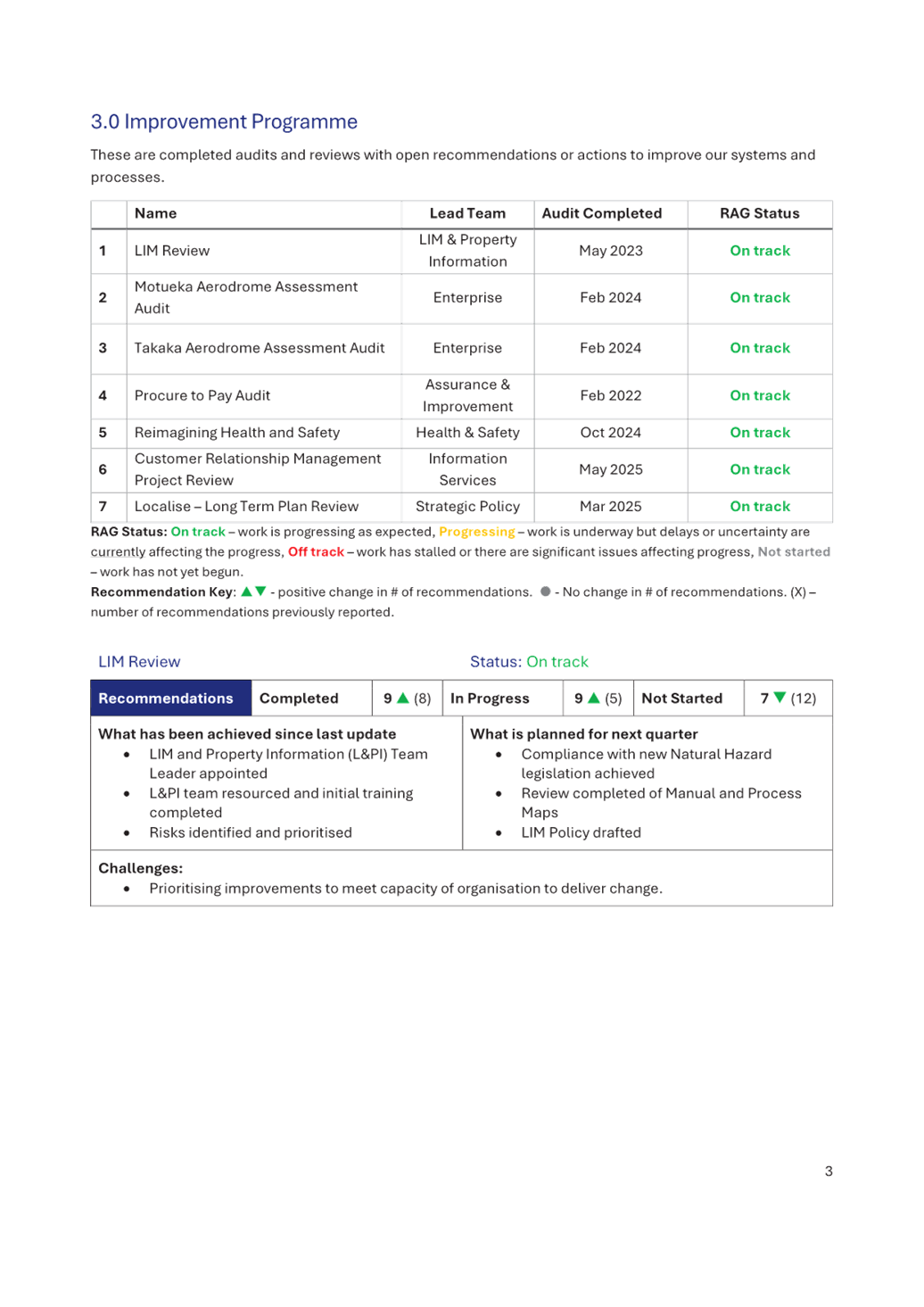

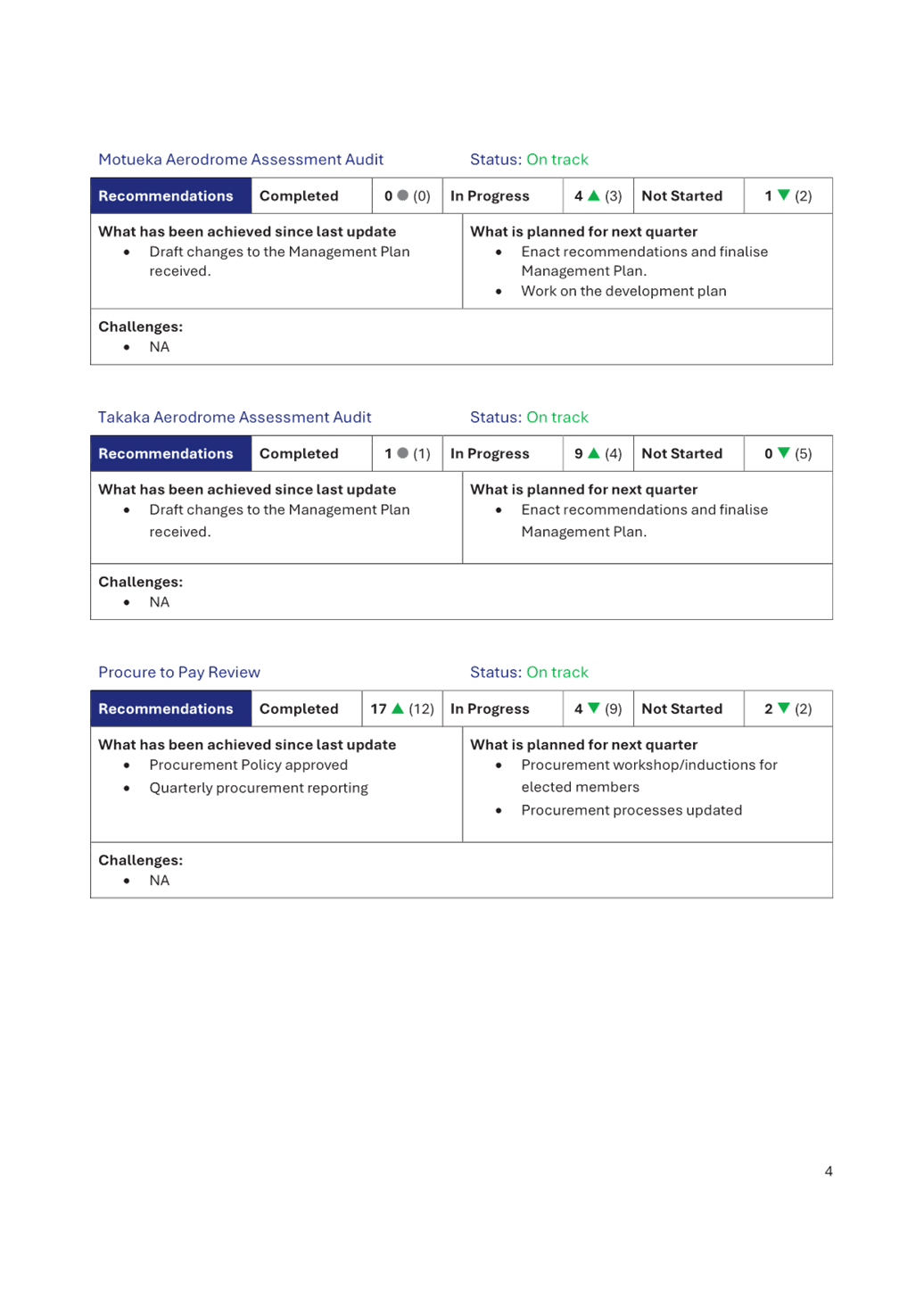

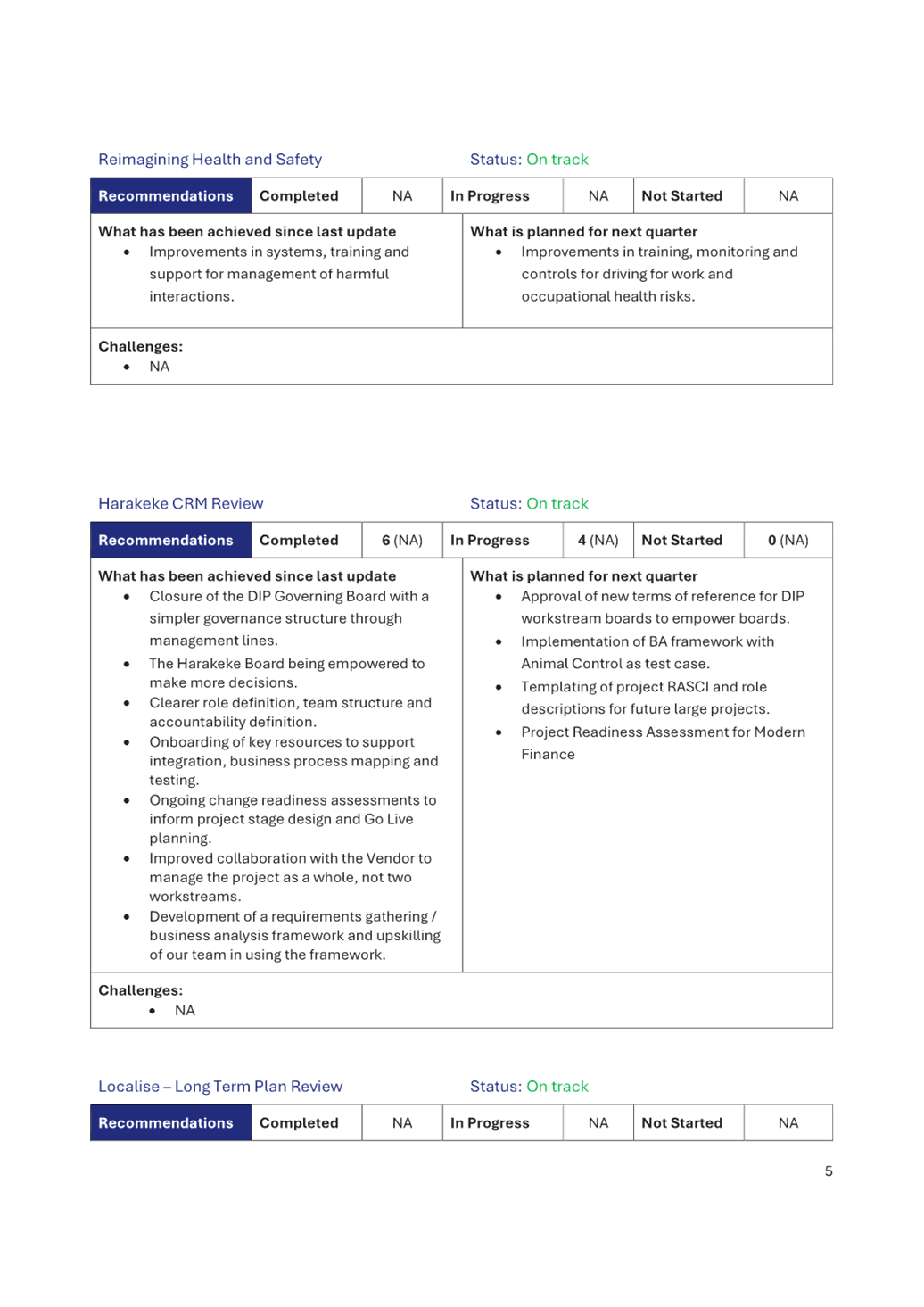

Assurance Report (Attachment 4) for Q1 2025/26 provides an overview of

completed, ongoing, and planned audits and reviews across Council, with a focus

on strengthening governance, systems, and service delivery.

5.2 Key highlights

include the Independent Quality Assurance review of the Harakeke CRM project (Attachment

5), which identified both strong leadership and areas for improvement, and

the ongoing implementation of recommendations from audits such as LIM,

Aerodrome Assessments, and Procure to Pay. The report also outlines upcoming

assurance activities including external audits and an integrity survey led by

Audit New Zealand.

5.3 The attached

report introduces a refreshed format for quarterly Assurance Reporting,

designed to support more efficient circulation and consideration by ELT, ARC,

and, where required, Council.

|

1.⇩

|

Quarterly

Risk Reporting - Q1 25-26

|

6

|

|

2.⇩

|

Financial

Strategic Risk Summary

|

15

|

|

3.⇩

|

Health and

Safety Strategic Risk Summary

|

20

|

|

4.⇩

|

Quarterly

Assurance Reporting - Q1 25-26

|

25

|

|

5.⇩

|

CRM IQA

Review Summary

|

31

|

Audit and Risk Committee Agenda – 01 October 2025

6.2 Internal Audit Charter and Plan

Information Only - No Decision

Required

|

Report

To:

|

Audit

and Risk Committee

|

|

Meeting

Date:

|

1

October 2025

|

|

Report

Author:

|

Amy

Clarke, Acting Assurance & Improvement Manager

|

|

Report

Authorisers:

|

Joanna

Cranness, People and Wellbeing Manager

|

|

Report

Number:

|

RFNAU25-10-2

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 This paper presents an updated Internal

Audit Charter (Attachment 1) and Internal Audit Plan (Attachment 2).

The documents have been developed to reflect current expectations of internal

audit, strengthen alignment with Office of the Auditor-General (OAG) guidance

and ISO standards, and ensure a practical and fit-for-purpose approach

appropriate to Tasman District Council’s size and maturity.

1.2 The Committee is asked to endorse the Charter and Plan, ahead of

them being submitted to Council for final approval.

2. Recommendation/s

/ Ngā Tūtohunga

That the Audit and Risk Committee

1. receives the Internal Audit Charter and Plan report RFNAU25-10-2; and

2. supports the Internal Audit Charter and Internal Audit Plan.

Recommendation to the Tasman District

Council

That the Tasman District Council

1. approves

the Internal Audit Charter and Internal Audit Plan.

3.1 Tasman District Council is committed to

improving its internal assurance and risk management practices. As part of this

effort:

· An updated Internal Audit Charter has been drafted to align with

best practice standards (Office of the Auditor-General, ISO 19011, Institute of

Internal Auditors), while being practical and understandable for a smaller

organisation.

· A new Internal Audit Plan has been developed, based on

Council’s strategic risks, known areas of concern, and available

resources.

3.2 Both documents

support the assurance and oversight role of ARC and Council, while promoting

transparency, accountability, and continuous improvement.

4. Internal Audit Charter

4.1 The revised Internal Audit Charter

replaces the previous version approved in May 2020. While many of the

principles remain aligned, the new Charter reflects improvements in clarity,

structure, and relevance for Tasman District Council today.

4.2 Notable changes include:

4.2.1 Plain English and Practical Focus: The Charter is more

accessible for managers and staff, particularly those unfamiliar with internal

audit concepts.

4.2.2 Updated Roles and Responsibilities: Clearer articulation of

the responsibilities of Internal Audit, the Executive Leadership Team (ELT),

Chief Operating Officer, and ARC.

4.2.3 Strengthened Independence: Dual reporting lines, safeguards,

and professional standards are outlined to ensure objectivity despite

organisational constraints.

4.2.4 Scope and Access Rights: Clarifies Internal Audit’s

authority to access systems, data, and personnel.

4.2.5 Connection to Internal Controls: Explains how internal audit

supports compliance with legislation, regulations, contracts, and external

standards.

4.2.6 Reference to the Three Lines Model: Introduces and explains

the Three Lines Model with a diagram to show the role of internal audit within

wider governance.

4.3 A tracked change

version has not been provided due to significant formatting and structural

differences between the 2020 and 2024 versions.

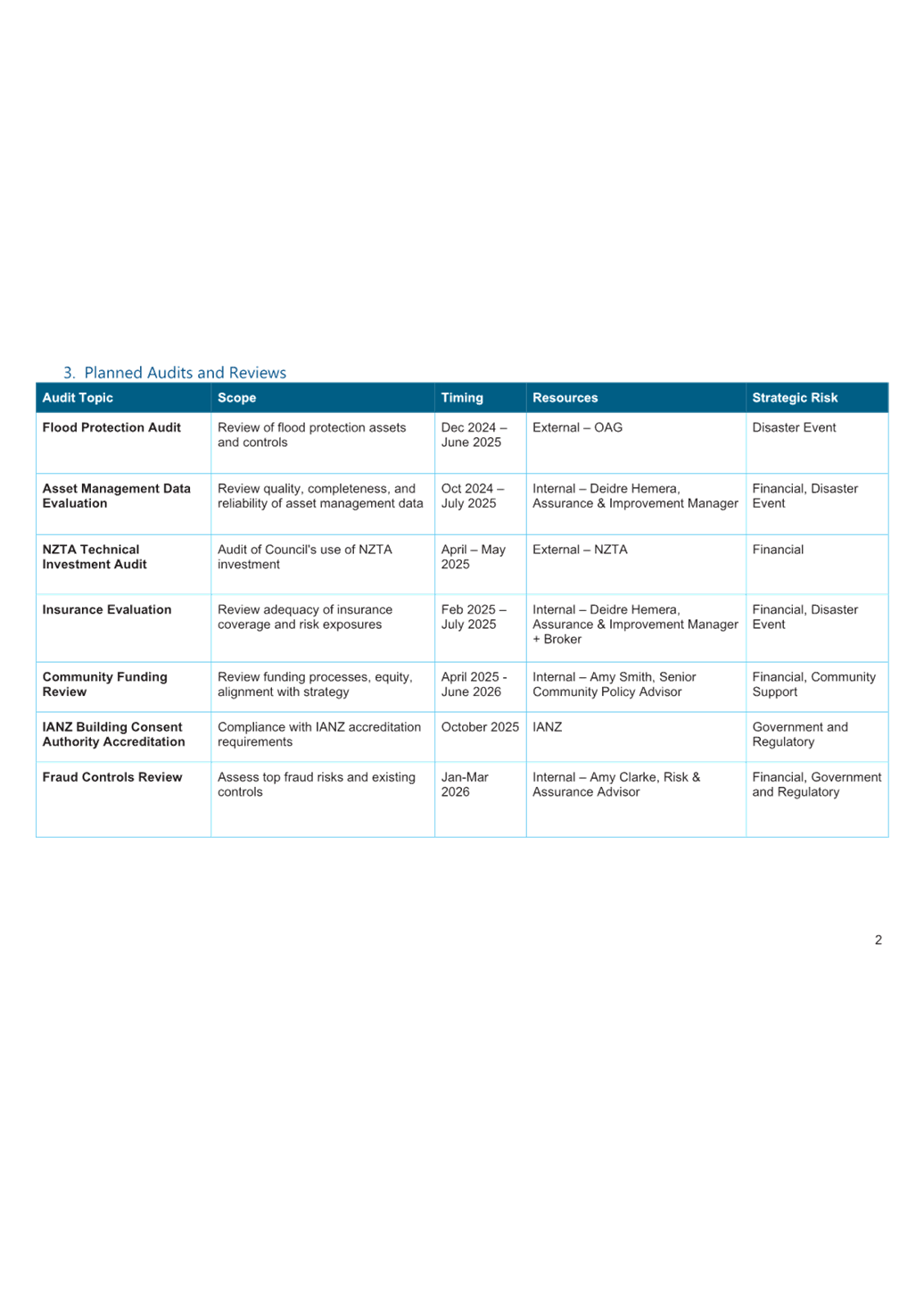

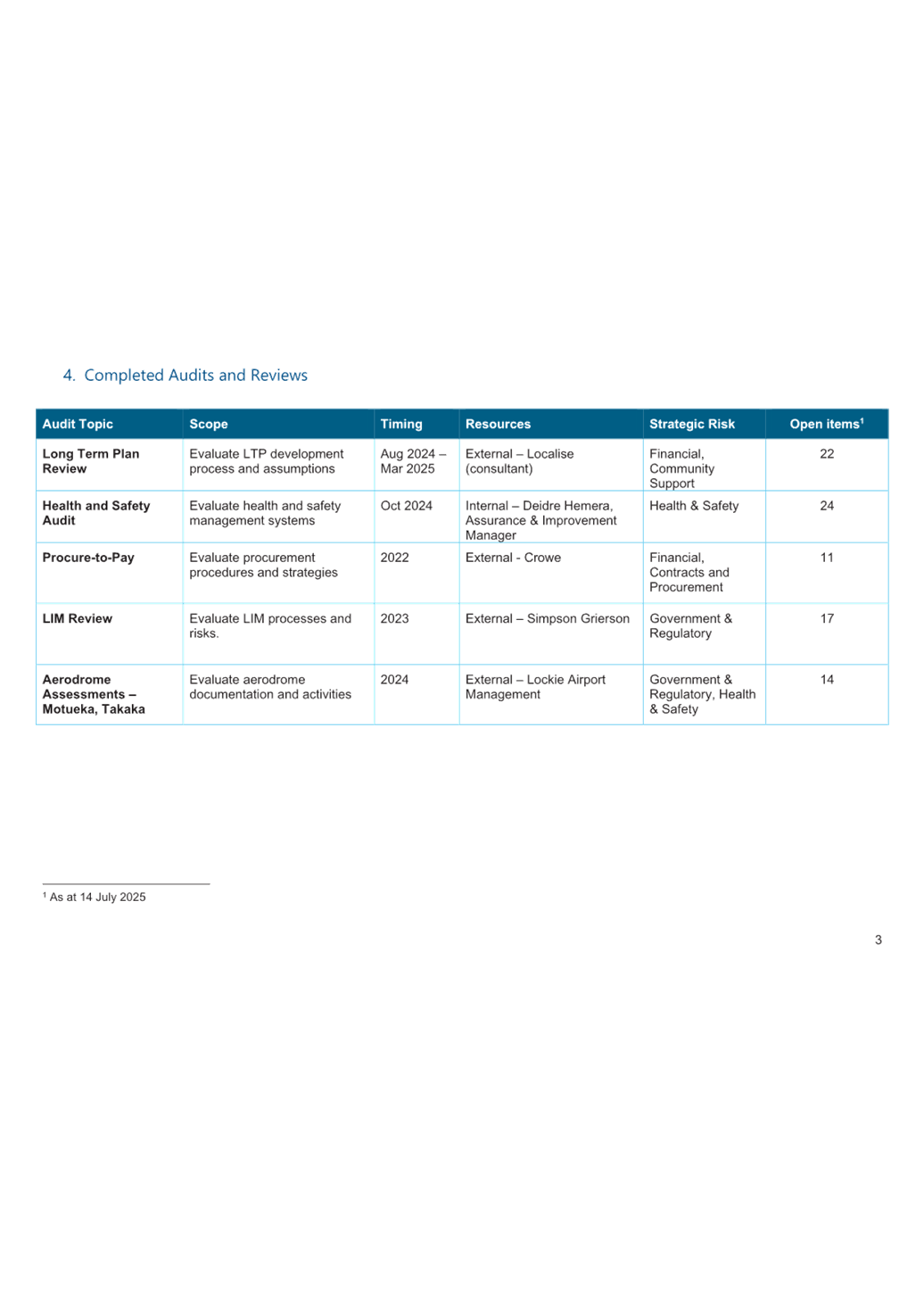

5.1 The attached Internal Audit Plan

outlines the proposed reviews for the 2024–25 and 2025–26 financial

years. The plan reflects:

· Current resource levels, while retaining flexibility to undertake

additional reviews if needed.

· Alignment to strategic risks, with a mapping of audits to

TDC’s top risks (e.g., financial sustainability, disaster event

preparedness, data and systems resilience).

5.2 The audit

approach balances improvement and assurance, and encourages a proactive,

non-punitive culture of learning and accountability.

6.1 Endorsement by the Audit and Risk

Committee is sought at this meeting.

6.2 Council approval will be sought

following ARC endorsement.

6.3 Internal audit

activities will continue as per the approved plan and updates will be reported

back to ARC regularly.

|

1.⇩

|

Internal

Audit Charter - DRAFT

|

37

|

|

2.⇩

|

Internal

Audit Plan - DRAFT

|

42

|

Audit and Risk Committee Agenda – 01 October 2025

6.4 Report on the 2024-2024 Long Term Plan Review

Information Only - No Decision

Required

|

Report

To:

|

Audit

and Risk Committee

|

|

Meeting

Date:

|

1

October 2025

|

|

Report

Author:

|

Pip

Jamieson, Principal Planner - Strategic Policy

|

|

Report

Authorisers:

|

John

Ridd, Group Manager - Service and Strategy

|

|

Report

Number:

|

RFNAU25-10-4

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 This report

provides background to the review of the 2024-2034 Long Term Plan which was

undertaken from August 2024 through to March 2025, a summary of the review

recommendations, and an outline of the plan to address the recommendations.

1.2 The report also

highlights the recommendation to review an appropriate role for the Audit and

Risk Committee in relation to the Long Term Plan.

2. Recommendation/s

/ Ngā Tūtohunga

That the Audit and Risk Committee

1. receives the Report on the 2024-2024 Long Term Plan Review (LTP)

report RFNAU25-10-4; and

2. notes the future Long Term Plan recommendations outlined; and

3. notes the recommendation to review an appropriate role of the Audit

and Risk Committee including an early workshop to establish their role in the

Long Term Plan process for example:

3.1 reviewing

preliminary assumption; and

3.2 reviewing the

draft Consultation Document; and

3.3 reviewing the

supporting documents prior to Audit NZ commencing their review.

3. Purpose

of the Long Term Plan Review

3.1 After the

adoption of the 2024-2034 Long Term Plan (LTP) on 27 June 2024, the Council

engaged the firm Localise to review the LTP documents and process to be able to

improve the design and planning for the next LTP. The objectives of the review

were to:

3.1.1 reflect the community’s aspirations and to manage risk;

3.1.2 enable the Council to consider needs and preferences of

different community groups;

3.1.3 effectively support the Council in strategic decision-making

and civic leadership;

3.1.4 ensure integration and line-of-sight from vision to assets,

services and financial forecasts; and

3.1.5 provide user-friendly narrative with right-sized documentation

that avoids unnecessary low value detail.

4.1 The LTP review

was conducted between August 2024 and March 2025 involving:

4.1.1 compilation of key background information

(legislative requirements, existing processes, documents);

4.1.2 stakeholder surveys, interviews (telephone,

online) with the Motueka and Golden Bay Community Boards, Community

Associations, Youth Council, Chamber of Commerce, Institute of Directors

Regional Committee, Nelson City and Marlborough District Councils, Audit NZ and

Nelson Regional Development Agency;

4.1.3 Te Rūnanga of

Ngāti Kuia, Te Rūnanga o Ngāti Rārua;

4.1.4 staff feedback and an ideas board;

and

4.1.5 workshops with the Council’s

Executive Leadership Team (ELT) and the Council.

4.2 The

review considered four key aspects:

4.2.1 narrative, process design and management;

4.2.2 engagement, consultation and associated

communication;

4.2.3 purpose, strategic direction and

prioritisation; and

4.2.4 documents and key inputs

4.3 Staff

have developed a proposed plan, structure and timeline in order to progress the

recommendations from the review. This has been considered by relevant managers

and the Executive Leadership Team, with the final plan approved and Project

Management Office resource has been engaged to help manage this process.

4.4 Establishment

of the appropriate members for roles on the LTP review project has taken time

as workloads have been adjusted to enable focus on the work.

4.5 The

final plan and structure are outlined under 10.

5.1 The review noted

commitment of the Council, ELT, Managers and Council staff to effective long

term planning, clearly evident genuine community engagement and that the LTP

process is highly intensive requiring substantial effort.

5.2 The Review

identified areas for improvement with the LTP process and documentation:

5.2.1 A highly intensive process requiring

substantial effort and starting late;

5.2.2 uncertainty if the result is commensurate

with the effort required;

5.2.3 engagement information not always fully

integrated into work programmes;

5.2.4 iwi not always being recognised as partners;

5.2.5 not all the key choices in the Consultation

Document being fully considered;

5.2.6 overwhelming and unclear information

presentation with unclear linkage to objectives and financial implications;

5.2.7 unclear role boundaries and

responsibilities;

5.2.8 an unhelpful narrative leading to the

Council not providing vision and strategic priorities;

5.2.9 confusion of the purpose of Activity

Management Plans (assets or activity focused)

5.2.9.1 time consuming to produce and repetitive

content;

5.2.9.2 not always meeting the standard for traditional

asset management plans; and

5.2.9.3 not fully understanding assets resulting in

inappropriate planning and investment.

5.2.10 not fully aligning aspirations with affordability;

5.2.11 hurried preparation of the accompanying documents;

5.2.12 lack of full clarity of the impacts and consequences of

Levels of Service and the measures;

5.2.13 overwhelming activity budget information not always

being considered collectively;

5.2.14 specific financial factors identified were:

5.2.14.1 moving away from a balanced budget;

5.2.14.2 not identifying all of the funding gaps

between LTPs;

5.2.14.3 parameters for budget managers not fully

clarified;

5.2.14.4 exception budgets not always being

reinforced;

5.2.14.5 total budget options not being considered

collectively or linked to strategic objectives; and

5.2.14.6 financial modelling taking time to

develop meaningful options.

6. Key Review Recommendations

6.1 Twenty two

recommendations were made, and grouped around four focuses:

Narratives, process design and

management

6.2 Adaptions to timing of LTP processes,

resourcing, resetting the narrative about LTPs, clearer LTP governance

structures, addressing accountabilities, greater risk management and

partnership with iwi.

Engagement, consultation and associated

communication

6.3 Continuing good outreach, integrating

results of early engagement feedback and improving the process for identifying

key questions in the Consultation Document.

Purpose, strategic direction and

prioritisation

6.4 Clearly engaging and agreeing on the

purpose and benefits of the LTP, undertaking a series of steps early in the new

triennium for the Council visioning and strategy process, mapping activities

against community outcomes and strategic priorities, preparing baseline budgets

to identify underlying financial shortfalls and providing clear guidance and

instructions to budget managers prior to preparing baseline budgets.

6.5 Not entering new costs into first cut

budgets without Executive Leadership Team sign off, identifying and scheduling

key service reviews, Executive Leadership Team and the Council taking a strong

leadership approach in balancing strategic choices and affordability,

developing templates for an ‘activity compendium and workshop

presentations.

Documents and key inputs

6.6 Considering options to improve financial

modelling capability and resourcing, retiring the current Activity Management

Plans to create traditional asset management plans and streamlined activity

statements for all activities, restricting the LTP documents into a shortened

Volume One with Volume Two for rates and financial information and Volume Three

for all the remaining policies and assessments as required.

7. Review Recommendations on the Audit and

Risk Committee

7.1 A recommendation

for greater risk management proposed a workshop be held with the Audit and Risk

Committee to establish their role in the LTP process. Potential areas where the

Committee might be involved are:

7.1.1 reviewing preliminary assumptions; and

7.1.2 reviewing the draft Consultation Document

before it goes to Audit NZ to review.

8. Future Business State Outcomes

8.1 The following

outcomes are anticipated as a result of implementing the recommendations from

the LTP review:

8.1.1 an effective ongoing

process of hearing from the community;

8.1.2 continuous

improvement of reliable, high-quality data and information;

8.1.3 strategic and

systemic asset management;

8.1.4 clear strategic

priorities, budgets and organisational structure;

8.1.5 appropriate revenue

generation and utilisation of resources and expertise; and

8.1.6 clear policies to

ensure work programmes and ways of working across Council will effectively

achieve stated outcomes.

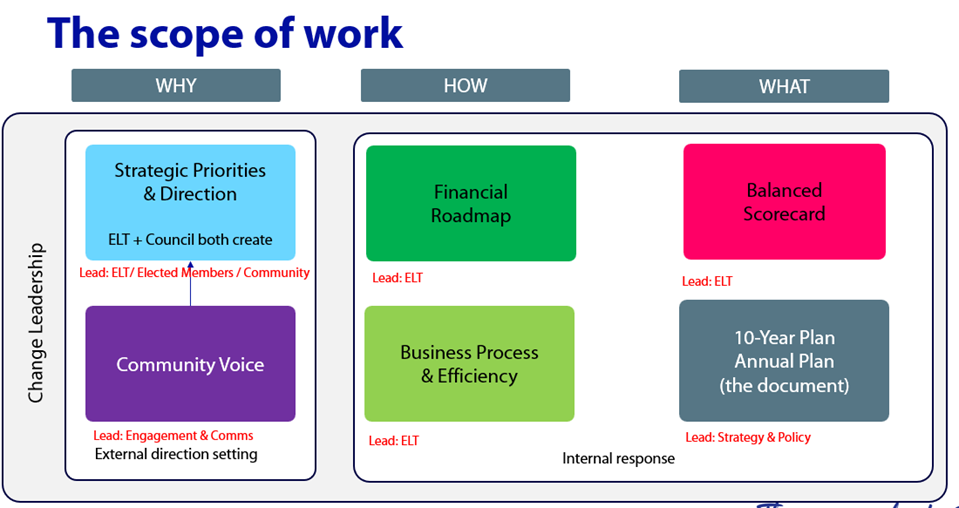

9. Agreed Purpose of the Long Term Plan

9.1 As a result of the LTP review

highlighting the need for the ELT to agree and then communicate clearly, what

the purpose of the LTP is, the following definition was agreed:

A clear line

of sight from community outcomes to priorities, to activities and resourcing.

9.2 It

was also agreed that the aim of implementing the recommendations from the LTP

review could be summarised as a process that delivers a product – with

two focus areas:

9.2.1 a process – cyclical, ongoing process of change,

improvements, and financially sustainable business as usual, that produces -

9.2.2 a product – documentation of a

clear line of sight from community outcomes to priorities, to activities and

resourcing. That includes key objectives and how they are achieved across 10

years, levels of service, key products, financial impacts, and funding

approaches.

10. Plan

to Address Recommendations

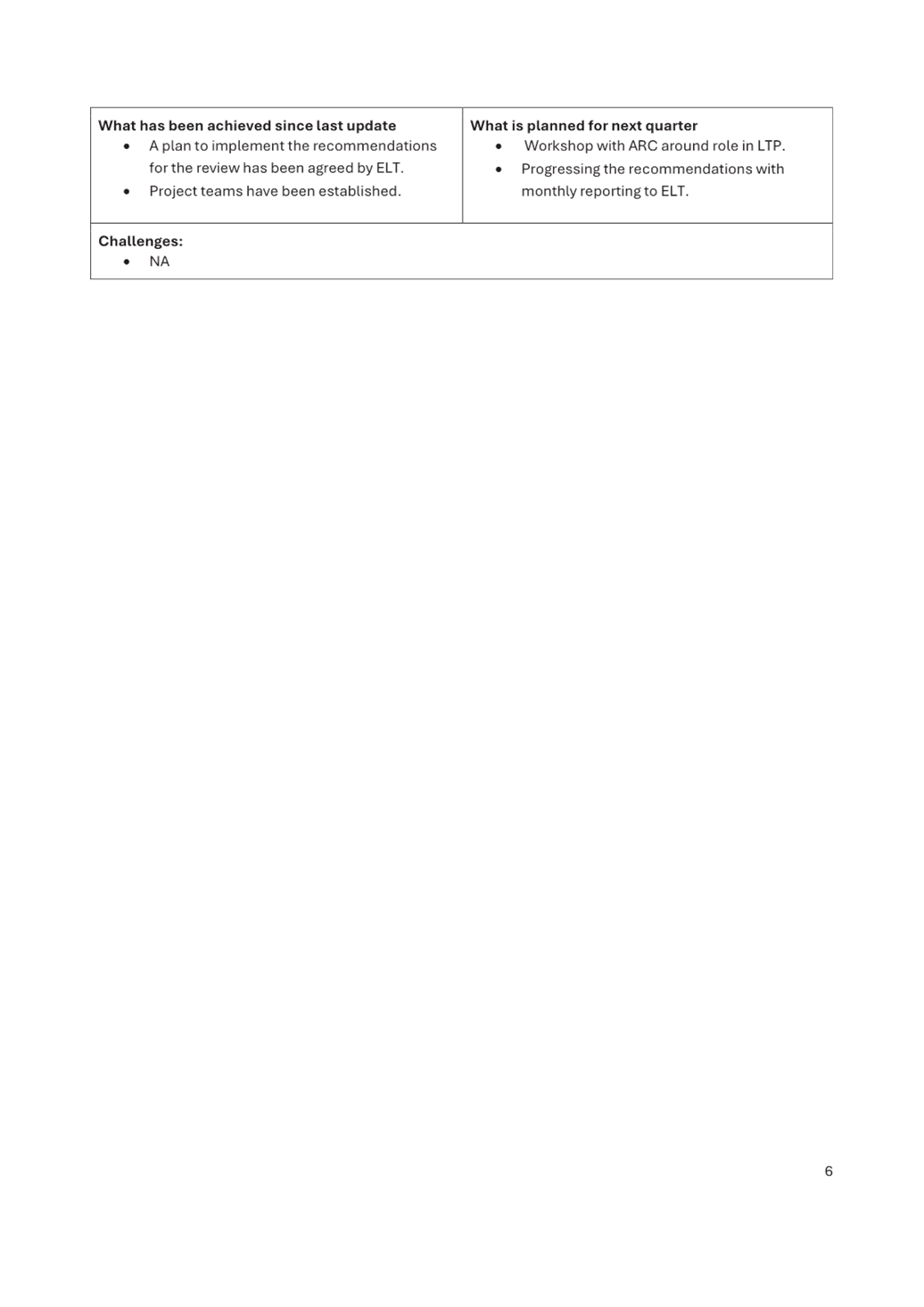

10.1 A plan to implement recommendations from the review

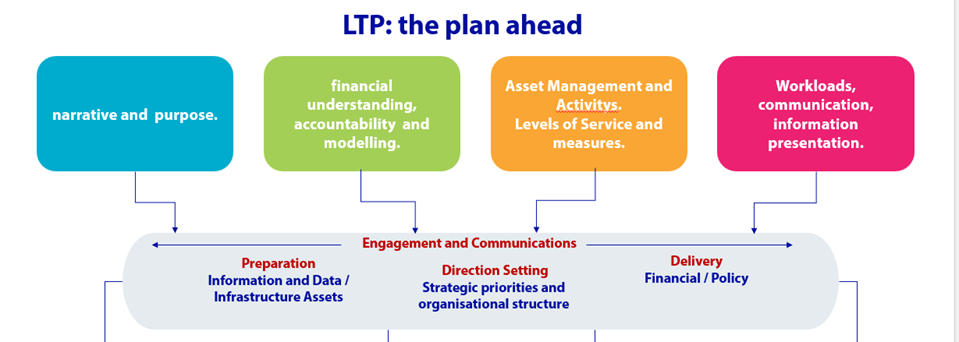

has been agreed by the ELT, addressing four key focus areas:

10.1.1 narrative and unclear purpose;

10.1.2 financial understanding, accountability and

modelling;

10.1.3 asset and activity management, levels of

service and measures; and

10.1.4 workloads, communication and information

presentations.

10.2 Key project teams, each with a project lead, have

been established and their work plans, actions, timelines have been

confirmed. The project teams are:

10.2.1 Infrastructure Planning;

10.2.2 Delivery;

10.2.3 Directions;

10.2.4 Information and Data; and

10.2.5 Engagement and Communications, which is to

be considered and integrated across all the project teams work.

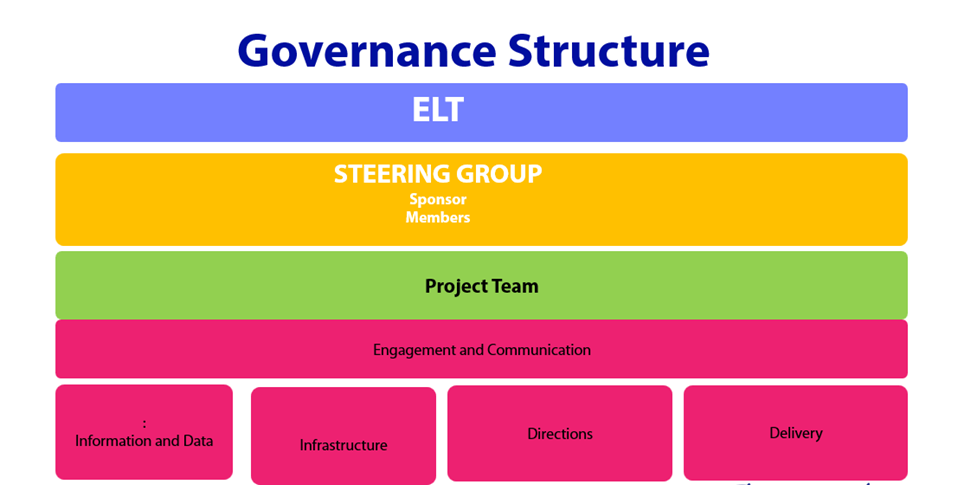

10.3 A project team, steering group and a sponsor have been established

with agreed terms of reference and a dedicated project manager from the

Projects Management Office has been assigned to manage the actions of each

project team, report to project team meetings, the LTP Review Steering Group,

and to administer Project and Steering Group meetings.

10.4 Progress of the LTP Review is now considered as one

of the six programmes of work within the Council’s key portfolio

“Planning the Future”.

10.5 The progress of this portfolio is reported to the ELT monthly along

with the other three portfolios (Financial Roadmap, Digital Improvement

Program, Local Water Done Well).

11.1 Monthly reporting to the ELT on the progress of the

Planning the Future portfolio (including the LTP) will continue.

11.2 The

recommended workshop with the Audit and Risk Committee regarding their role in

the LTP has been scheduled for 1 October 2025 with a focus on:

11.2.1 the Audit and Risk Committee’s role

with Audit NZ;

11.2.2 risk assessment and management;

11.2.3 review of the preliminary assumptions; and

11.2.4 review of the draft

Consultation Document before it goes to Audit NZ to review.

11.3 Following

the workshop staff will incorporate feedback into a draft terms of reference

and prepare reporting for future Audit and Risk Committee meetings as

appropriate.

|

1.⇩

|

Long Term

Plan Review Report Final April 2025

|

66

|