Notice

is given that an ordinary meeting of the Tasman District Council will be held

on:

|

Date:

Time:

Meeting

Room:

Venue:

Zoom

conference link:

Meeting ID:

Meeting Passcode:

|

Thursday 8 May 2025

9.30am

Tasman Council Chamber

189 Queen Street, Richmond

https://us02web.zoom.us/j/86304018904?

863 0401 8904

042580

|

|

Tasman

District Council

Kaunihera

Katoa

AGENDA

|

MEMBERSHIP

|

Mayor

|

Mayor T King

|

|

|

Deputy Mayor

|

Deputy Mayor S Bryant

|

|

|

Councillors

|

Councillor C Butler

|

Councillor M Kininmonth

|

|

|

Councillor G Daikee

|

Councillor C Mackenzie

|

|

|

Councillor B Dowler

|

Councillor K Maling

|

|

|

Councillor J Ellis

|

Councillor B Maru

|

|

|

Councillor M Greening

|

Councillor D Shallcrass

|

|

|

Councillor C Hill

|

Councillor T Walker

|

(Quorum 7 members)

|

|

|

Contact Telephone: 03 543 8400

Email: Robyn.Scherer@tasman.govt.nz

Website: www.tasman.govt.nz

|

Tasman District

Council

Agenda – 08 May 2025

AGENDA

1 Opening, Welcome, KARAKIA

2 Apologies

and Leave of Absence

|

Recommendation

That apologies be accepted.

|

3 Public

Forum

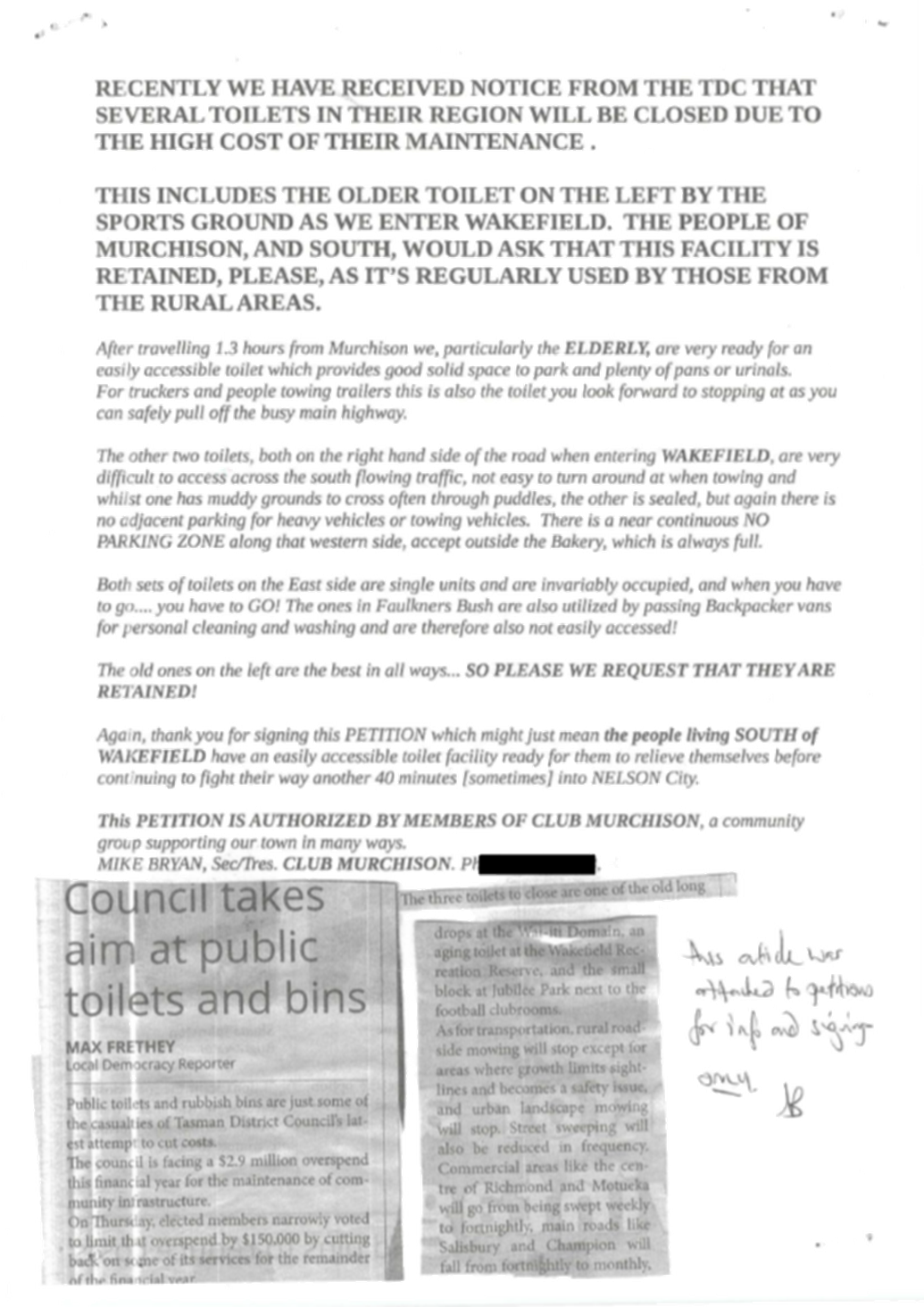

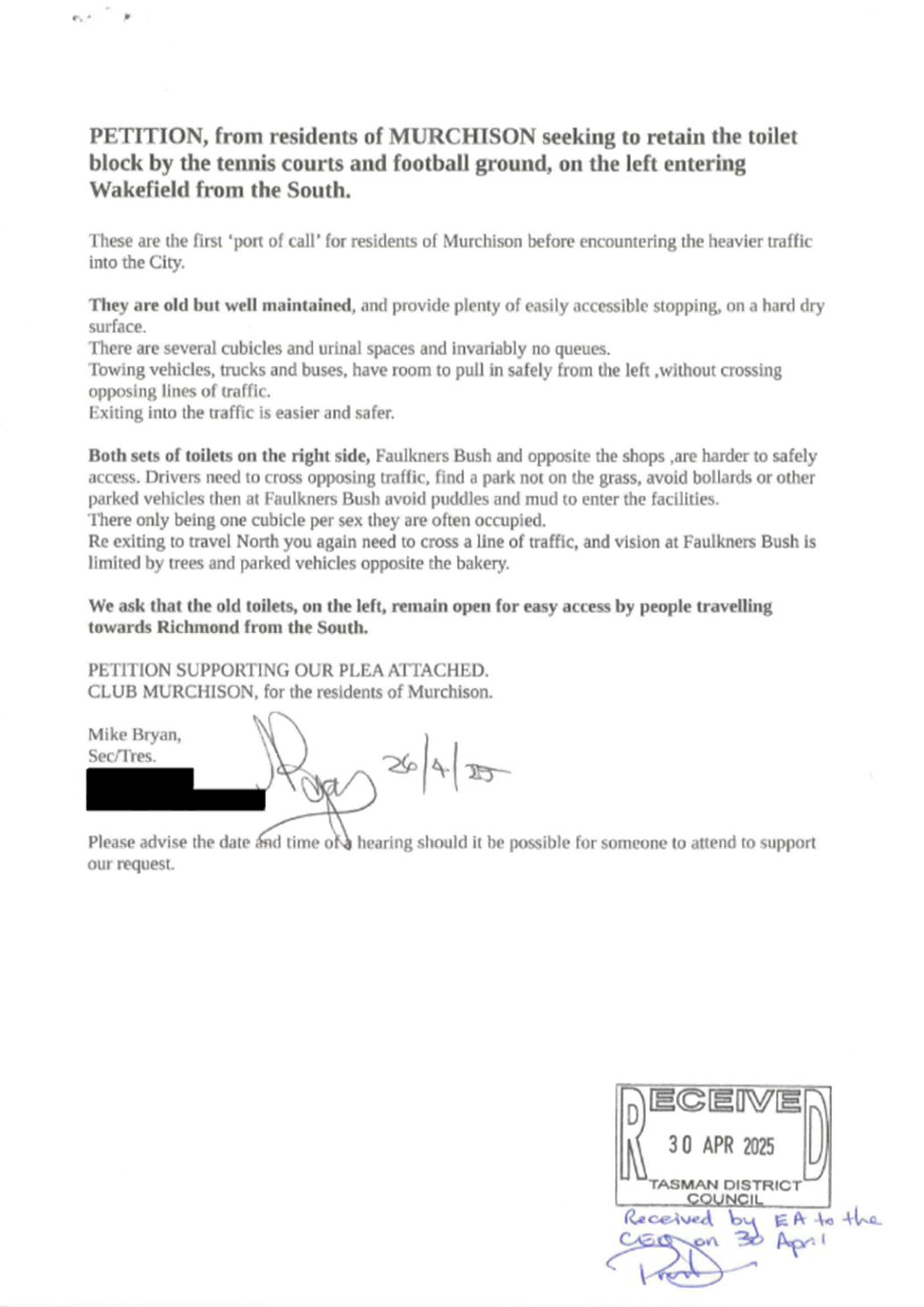

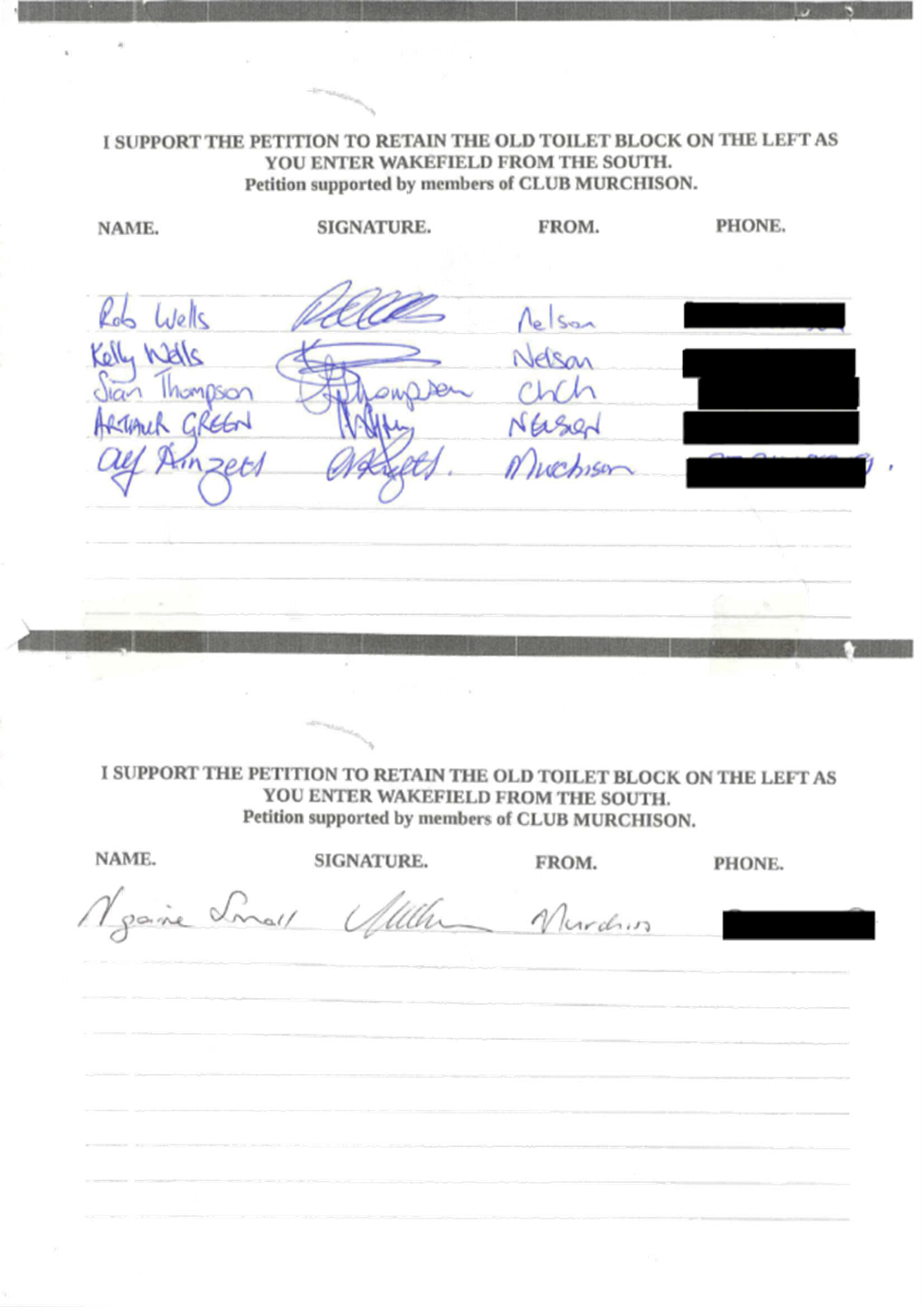

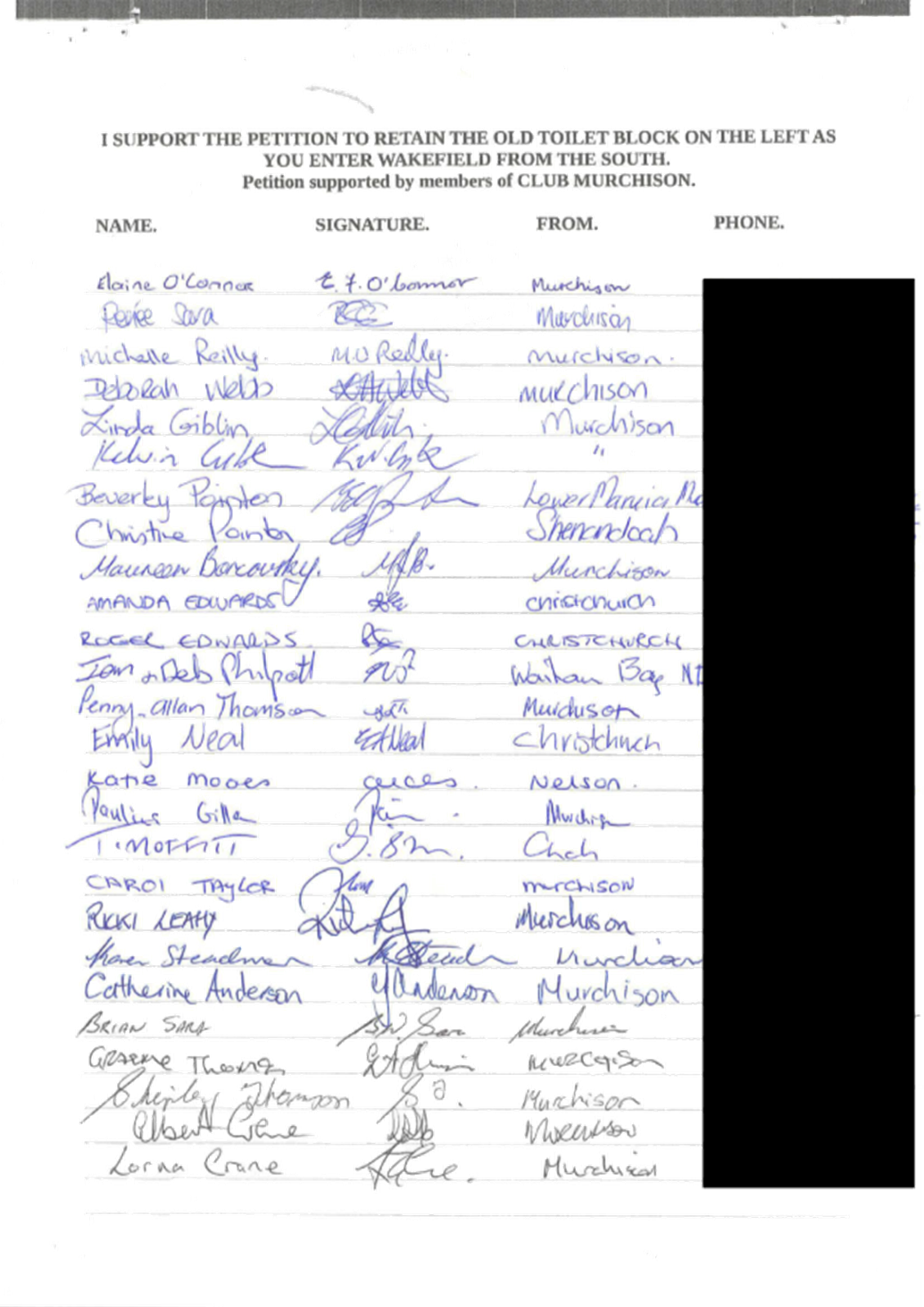

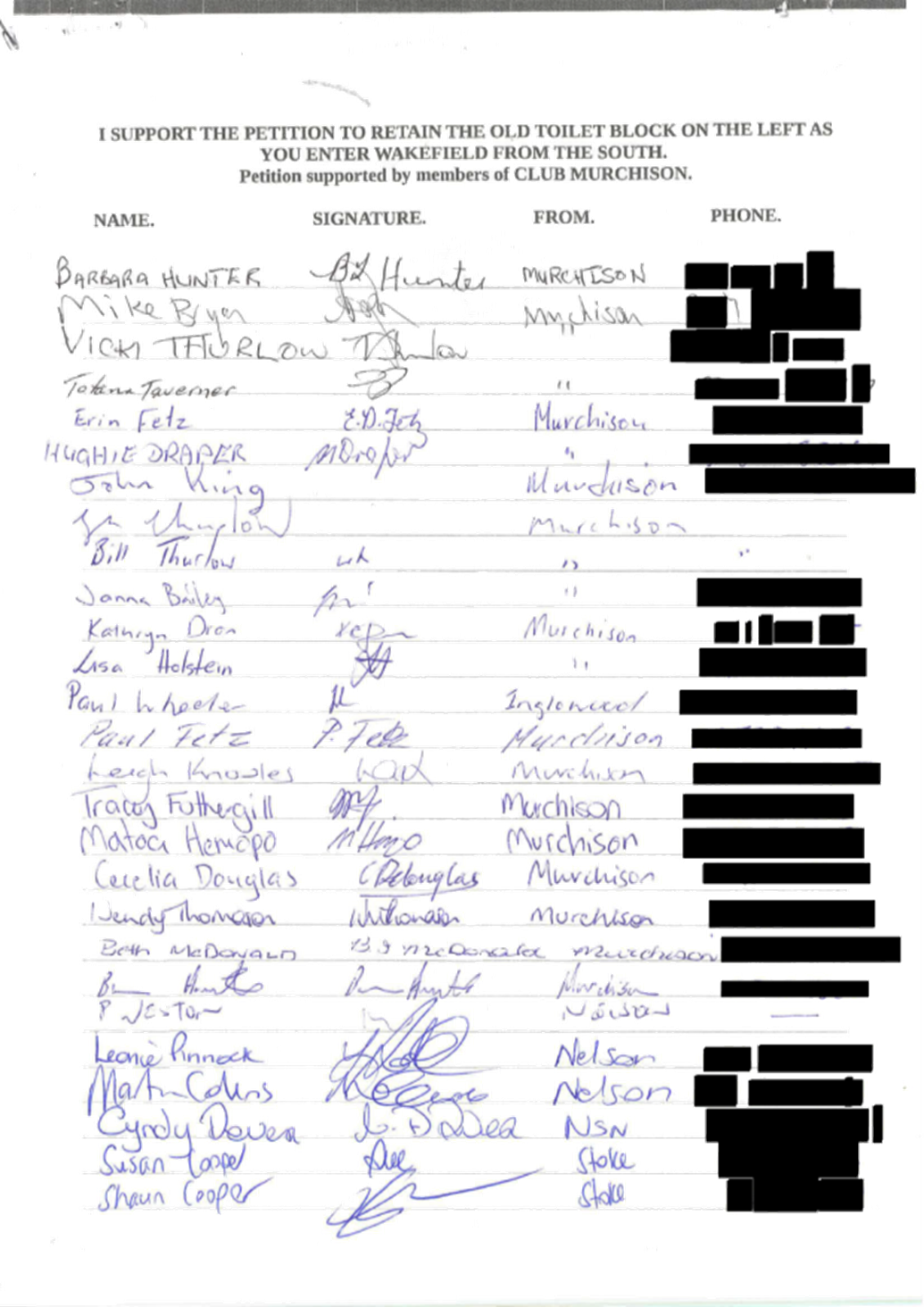

3.1 Presentation of Petition - Murchison Community

Members - Concerns regarding the closure of toilets at Wakefield.............................................................. 5

4 Declarations

of Interest

5 LATE

ITEMS

6 Confirmation

of minutes

|

That the

minutes of the Tasman District Council meeting held on Thursday, 27 March

2025, be confirmed as a true and correct record of the meeting.

|

|

That the

minutes of the Tasman District Council meeting held on Thursday, 17 April

2025, be confirmed as a true and correct record of the meeting.

|

|

That the

minutes of the Tasman District Council meeting held on Wednesday, 30 April

2025, be confirmed as a true and correct record of the meeting.

|

|

That the

confidential minutes of the Tasman District Council meeting held on Thursday,

27 March 2025, be confirmed as a true and correct record of the meeting.

|

|

That the confidential

minutes of the Tasman District Council meeting held on Thursday, 17 April

2025, be confirmed as a true and correct record of the meeting.

|

7 Reports

7.1 Revocation of Community Infrastructure Consideration

of Operational Cost Savings 2024/2025 decision of 27 March 2025 Council meeting................................................................... 11

7.2 Quarterly Financial Report - to 31 March 2025..... 15

7.3 2024/25 Forecast Overspend................................ 26

7.4 Hamama Water Supply - Approval for Renewal

Expenditure............................................................ 35

7.5 Chlorination Exemption for Upper Tākaka

Water Supply..................................................................... 41

7.6 Wakatū Non-Vesting Option.................................. 47

7.7 Tapawera Community Hub Location..................... 54

7.8 Lower Queen Street Bridge Upgrade - Temporary

Bypass Considerations.......................................... 67

7.9 Amendments to Delegations Register................... 91

7.10 Section 17A Service Delivery Review - Community Facilities................................................................ 122

7.11 2025 Tasman District Council Election - Order of Candidate

Names

on Voting Documents and Electoral System for 2028 Election........................................................ 149

7.12 Local Government Act 2002 - Section 17A Review Policy.................................................................... 154

7.13 Local Government Funding Agency Nominating Councils................................................................ 166

7.14 Chief Executive's Update..................................... 219

7.15 Mayoral Update Report........................................ 224

7.16 Annual Plan 2025/2026 Consultation Document Report................................................................... 227

8 Confidential

Session

Nil

9 CLOSING

KARAKIA

Tasman District

Council

Agenda – 08 May 2025

3 Public

Forum

3.1

Presentation of Petition

- Murchison Community Members - Concerns regarding the closure of toilets at

Wakefield

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

8

May 2025

|

|

Report

Author:

|

Elaine

Stephenson, Governance Manager

|

|

Report

Authorisers:

|

|

|

Report

Number:

|

RCN25-05-1

|

1. Public

Forum / Te Matapaki Tūmatanui

Deputy Mayor Stuart Bryant will present a

petition on behalf of Murchison community members supporting the retention of

the old toilet block, on the left entering Wakefield from the South.

The petition, consisting of 59 signatures,

together with supporting information, is attached as Attachment 1.

|

1.⇩

|

Murchison

Community petition regarding Wakefield toilets

|

6

|

Tasman District

Council

Agenda – 08 May 2025

Tasman District Council Agenda – 08 May 2025

7 Reports

7.1

Revocation of Community

Infrastructure Consideration of Operational Cost Savings 2024/2025 decision of

27 March 2025 Council meeting

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

8

May 2025

|

|

Report

Author:

|

Leonie

Rae, Chief Executive Officer

|

|

Report

Number:

|

RCN25-05-2

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 To

revoke part of the previous decision made at the 27 March 2025 Tasman District

Council meeting - Community Infrastructure Consideration of Operational Cost

Savings 2024/2025 [CN25-03-16].

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 A

late report was presented to the 27 March 2025 Council meeting proposing

Community Infrastructure operational cost savings to reduce forecasted

over-expenditure in the maintenance budget. The late item agenda for that

report can be found here.

2.2 The

minutes of the 27 March Council meeting record the

decision as:

7.7 Consideration of Operational Cost

Savings 2024/2025

CN25-03-16

That the

Tasman District Council

1.

receives the Report on Community Infrastructure

Consideration of Operational Cost Savings 2024/2025, RCN25-03-12; and

2.

notes that for the Waters and Wastewater activity the frequency of routine

monitoring will only be reduced where compliance with water regulations is not

compromised; and

3.

notes that reducing routine maintenance in the Waters and Wastes activity may

realise circa $10,000 savings in 2024/25; and

4.

notes that there is little opportunity to reduce levels of service in the Waste

Management and Minimisation activity without incurring additional costs next

year and that increasing gate charges is not recommended; and

5.

approves the following levels of service reductions in Reserves and Facilities

activity for the remainder of the 2024/2025 year:

5.1

the removal of Rubbish Bins from Reserves, potentially saving $229,000 per

annum; and

5.2

reducing the cleaning frequency of 14 public toilets saving $75,000 per annum;

and

5.3

the temporary closure of three public toilets and the discretion to temporarily

close more on a seasonal basis if identified as low use, saving $12,000 per

annum; and

5.4

reducing annual bedding displays (planting) in formal gardens saving $84,000

per annum; and

5.5

reducing conservation shrub maintenance saving $159,000 per annum; and

6.

approves reducing the levels of service within the Transportation activity for

the remainder of the 2024/2025 year as follows:

6.1

reduce the frequency of street sweeping across all urban areas potentially

saving $30,000; and

6.2

pause rural roadside mowing except for safety/critical sightlines potentially

saving $90,000; and

6.3

reduce the urban landscape mowing potentially saving $2,500.

2.3 The

rationale for the resolutions is contained in that report (CN25-03-16).

2.4 Following

discussions with staff and elected officials the recommendation is that the

Council rescinds part of the previous decision of the Council, being

resolutions 5.1 to 5.5.

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman

District Council

1. receives

the Revocation of Community Infrastructure Consideration of Operational Cost

Savings 2024/2025 decision of 27 March 2025 Council meeting report,

RCN25-05-2; and

2. revokes the following part of the previous decision

(CN25-03-16), made at the 27 March 2025 Council meeting regarding Community

Infrastructure Consideration of Operational Cost Savings 2024/2025:

That the Tasman District

Council

…

5. approves

the following levels of service reductions in Reserves and Facilities activity

for the remainder of the 2024/2025 year:

5.1 the

removal of Rubbish Bins from Reserves, potentially saving $229,000 per annum;

and

5.2 reducing

the cleaning frequency of 14 public toilets saving $75,000 per annum; and

5.3 the

temporary closure of three public toilets and the discretion to temporarily

close more on a seasonal basis if identified as low use, saving $12,000 per

annum; and

5.4 reducing

annual bedding displays (planting) in formal gardens saving $84,000 per annum;

and

5.5 reducing

conservation shrub maintenance saving $159,000 per annum; and

…

3. notes that the Reserves and Facilities activity will

absorb these costs and continue to make operational decisions to reduce ongoing

costs.

4.1 Following discussions with elected officials and staff, it

has been decided to revoke resolution 5.1 to 5.5 from the late report 7.7

presented at the Council meeting on 27 March 2025, titled “Consideration

of Operational Cost Savings 2024/2025”.

4.2 The

rationale is considered that the wording of this part of the resolution was not

clear enough to ensure that the elected members had a clear understanding of

the effect of this decision. This is partly because the cost savings were on a

‘per annum’ basis as opposed to being an indication of actual

costs.

4.3 This

confusion has been echoed by parts of the community.

4.4 Further

work has also been undertaken which indicates that the expected savings for the

current financial year are not as significant as indicated in the previous

report.

5. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

5.1 The Facilities and Reserves team will

continue to evaluate potential cost savings across their activities as part of

standard operational management.

5.2 Achieving any cost reductions will

require enhanced oversight of services, including adjustments to service levels

such as the frequency of toilet cleaning based on seasonal demand.

6.1 The Council has the option to either

rescind part of the previous decision or continue with the resolutions as

passed.

6.2 Rescinding part of the previous decision

is recommended.

7.1 The Council has the legal ability to

rescind part of the previous decision made.

7.2 It is noted that the decision to rescind

is not an inconsistent decision for the purposes of section 80 of the Local

Government Act 2002. This is because it is revoking that decision as opposed to

acting in an inconsistent manner with it.

8. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

8.1 The previous decision contained in the

minutes (CN25-03-16) generated significant interest in the community. The

rescinding part of that decision is likely to garner similar interest and,

based on the feedback received, be supported by the community.

9. Communication

/ Whakawhitiwhiti Kōrero

9.1 Following this decision a statement will

be provided on the Council’s social media channels.

10.1 The rescinding of this decision will create

additional financial pressure that the activity will need to manage carefully.

11. Conclusion

/ Kupu Whakatepe

11.1 It is recommended that the Council rescind part of its previous

decision on the basis that the previous resolution was not sufficiently clear

and the proposed cost savings may not be able to be recognised.

Nil

Tasman District

Council

Agenda – 08 May 2025

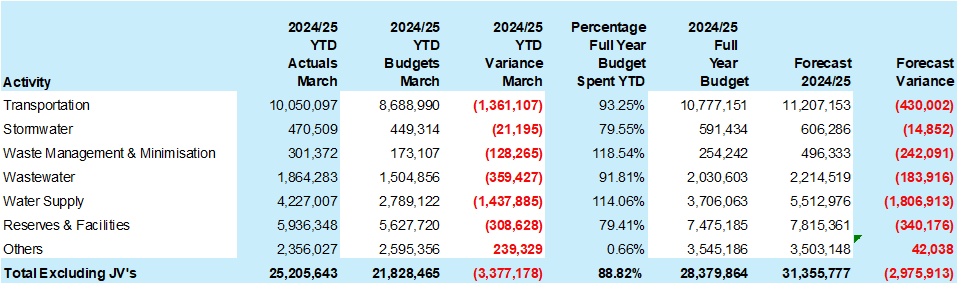

7.2 Quarterly Financial Report - to 31 March 2025

Information Only - No Decision

Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

8

May 2025

|

|

Report

Author:

|

Paul

Egan, Management Accounting Manager

|

|

Report

Authorisers:

|

Mike

Drummond, Chief Financial Officer

|

|

Report

Number:

|

RCN25-05-3

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 This financial

report provides an update on key financial information for the nine months

ending 31 March 2025.

1.2 The scope of this financial report

excludes revenue and expenditure from joint operations, as well as the share of

associates’ surplus or deficit. This approach ensures a focused analysis

on the financial results of the core operations of the Council. Amounts related

to joint operations and associates will be consolidated and included in the

2024/25 Annual Report.

1.3 As of 31 March 2025, the accounting

deficit is $4.7 million higher than budgeted, primarily due to increased

maintenance expenditure, depreciation and amortisation, which outweigh

favourable variances in employee and other expenses.

1.4 We are still forecasting an unfavourable

variance in borrowing costs of $2.3 million by year-end. Reported borrowing

costs have been impacted by credit interest error that will come out on

consolidation at year end.

1.5 Overall, we anticipate a circa $6.5

million increase to the 2024/2025 budgeted year-end deficit position. This will

need to be debt-funded and will impact rates and borrowing costs for the

2025/2026 Annual Plan budget. Typically, deficits are funded at the activity

level over the following three to five years. This funding matter is being

addressed in the 2024/25 Forecast Overspend report being presented at this

meeting.

1.6 Overall revenue

is tracking close to budget, with higher operating subsidies, water rates, but

lower development contributions, reserve financial contributions, and forestry

revenue.

1.7 The balanced

budget benchmark that includes some capital related income but focuses on

funding of operating expenditure is at 90% year to date, versus an Annual Plan

budget benchmark of 96%.

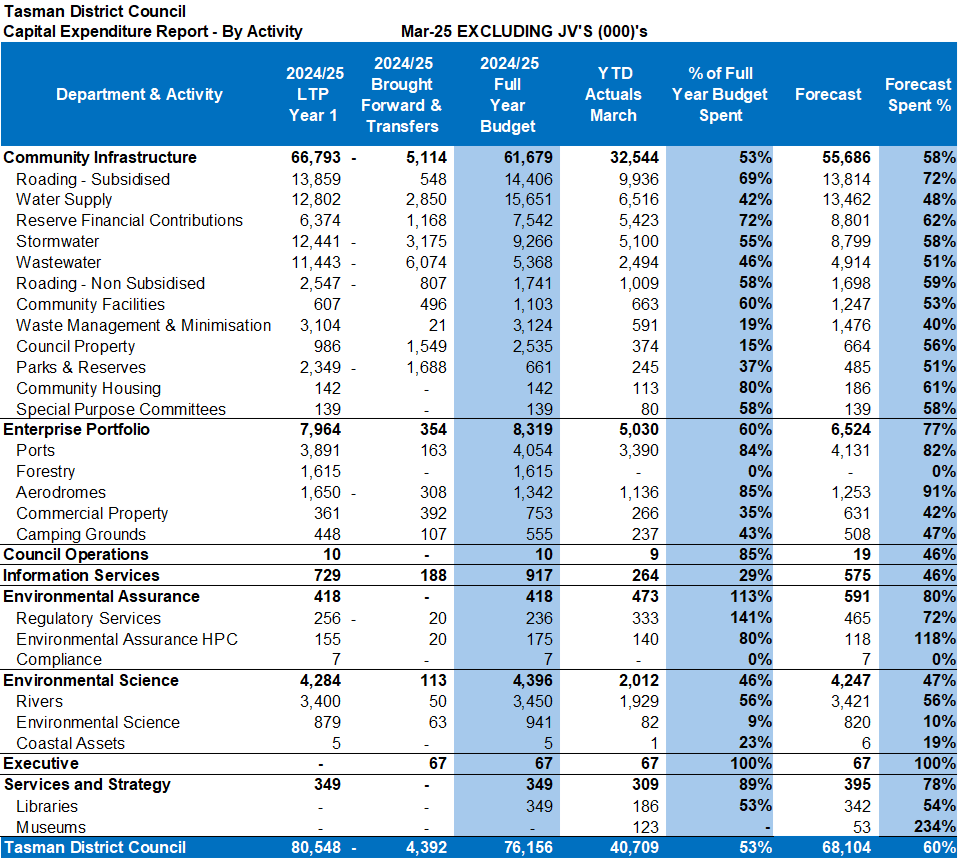

1.8 Capital

expenditure is $40.7 million at 53% of full year budget of $76 million. It

appears unlikely the full year budget can be achieved.

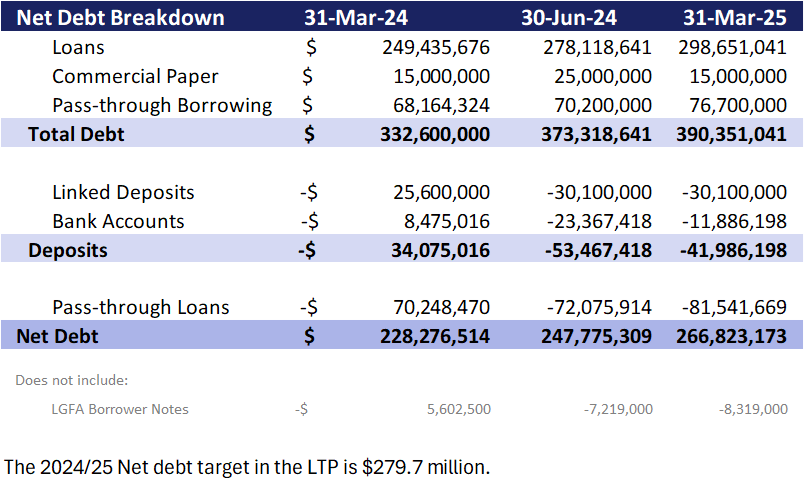

1.9 Net debt is at

$266.8 million versus the Long Term Plan (LTP) estimate for 2024/25 of

$279.7 million.

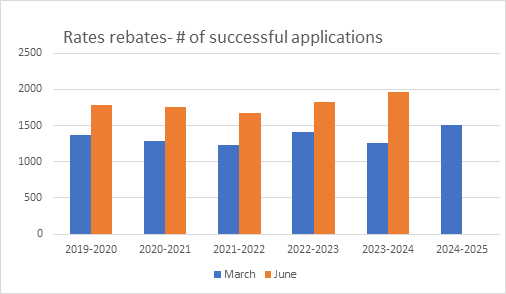

1.10 While receivables, rates arrears and dishonoured

direct debit rates payments are consistent with recent years, the level of

successful rates rebate applications year to date is higher than the previous

five years. Staff continue to promote the Rates Rebate Scheme.

2. Recommendation/s

/ Ngā Tūtohunga

That the Tasman District Council

1. receives the Quarterly Financial Report - to 31 March 2025 report, RCN25-05-3.

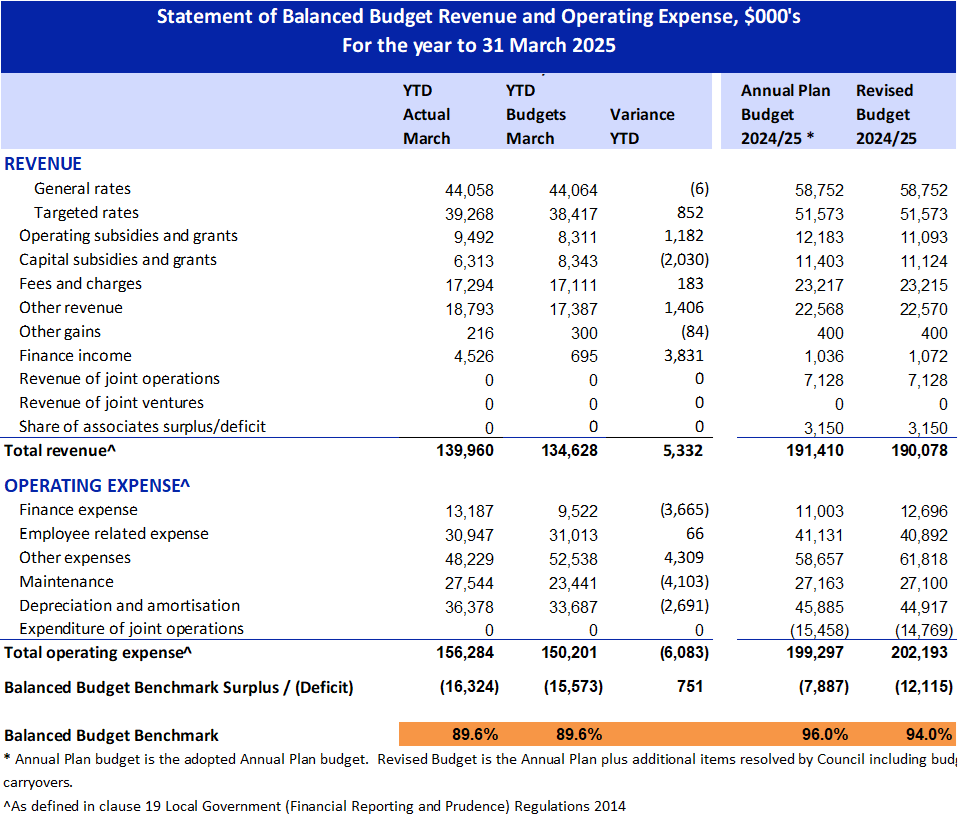

3.1 Balanced

Budget benchmark

3.1.1 The balanced budget benchmark is part of a suite of benchmarks

as defined in the Local Government (Financial Reporting and Prudence)

Regulations 2014. These benchmarks are included in the Council’s Annual

Reports, Annual Plans and Long Term Plans.

3.2 The official balanced budget benchmark

includes capital subsidies and grants as operational income, significantly

reducing the budgeted and reported operational deficit (by $6.3 million). This

overstates the percentage of operating expenditure covered by revenue, removing

the capital subsidies from the balanced budget calculations would reduce the

expenditure coverage percentage to a much lower 86%.

3.3 The

balanced budget benchmark amounts are detailed below to provide an indication

of reporting.

3.4 Loan funded operating expenses impact

the balance budget benchmark. Year to date, they were $3.5 million, of which $3

million related to the Digital Innovation Programme, with most of the rest

being for the Tasman Resource Management Plan (TRMP) and Saxton Field.

The budget for loan funded operating expense for the 2024/25 year is $9.25

million, however, $3.17 million, related to the museum storage facility, has

been deferred.

3.5 The level of depreciation that is funded

impacts the balanced budget benchmark. Funded depreciation is an expense

related to the wearing out of Council assets. It is considered when calculating

rates and the funds collected are used to fund the renewal of assets.

Approximately 75% of depreciation expense is included in these calculations,

meaning less is recovered, increasing the likelihood some operating expenses

will need to be funded from debt.

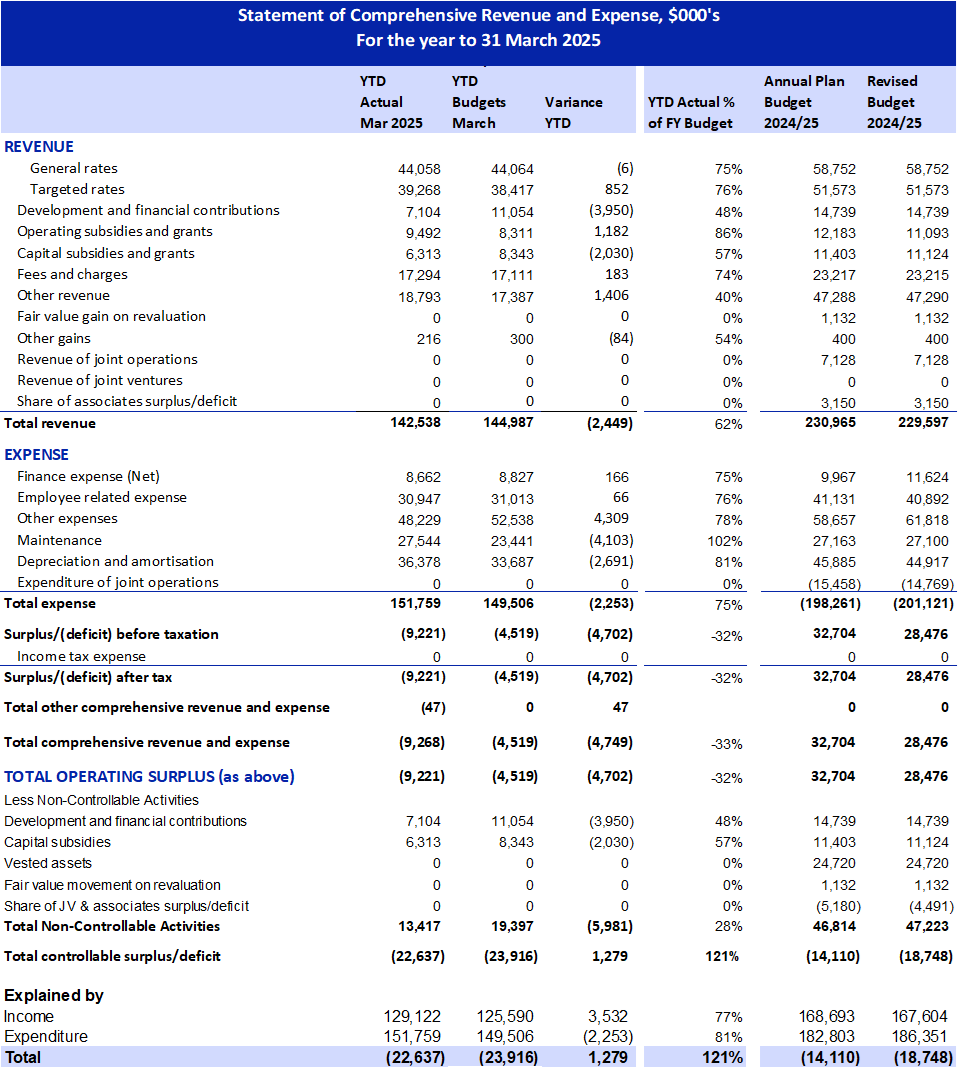

Statement of Comprehensive Revenue and

Expense

Areas of key

variance are elaborated below.

Maintenance Analysis

4.1 As

indicated in the previous reports, maintenance expenditure is continuing to

track over budget. It is expected to end the year approximately $3 million over

budget, given the latest forecasts. This over expenditure estimate excludes

Joint Operations.

4.2 Water Supply, Transportation and Reserves and Facilities are the

main areas of forecast overspend.

Year to date Revenue

4.3 Development

and Financial Contributions are tracking at about half the level for the same

period in the previous two years. With the increase in Development Contribution

charges from 1 July 2024, some developers prepaid their development

contributions in the 2023/24 year under the Council’s once paid always

paid policy.

4.4 Fees

and Charges continue to track slightly ahead of budget, with Building Assurance

and Resource Consents performing better than budget, however, Waste Management

& Minimisation are down due to reduced volumes.

4.5 Other

Revenue is $1.4 million net ahead due to a mix of factors, including dividend

income due to the change in timing in payment of the Infrastructure Holdings

Limited (IHL) dividend. Lease related income is higher, as are Joint

Operations related distributions, with offsets from lower forestry income due

to lower log prices and revised harvesting programmes.

Finance Expense (Net)

4.6 After

making an adjustment of circa $1 million for interest related to Joint

Operations, the Net correct Finance expense variance is approximately

$1,166,000 unfavourable to budget year to date. The timing of capital

expenditure, and higher interest income will increase the net expense. This is

expected to be a $2.3 million unfavourable position at year end.

Depreciation and Amortisation

4.7 With

the higher-than-expected increase in asset valuations at the end of 2023/24,

the budgeted depreciation and amortisation in the Annual Plan/Long Term Plan is

considerably less than current actuals. Year to date depreciation and

amortisation is $2.7 million over budget and is expected to end the year

over $4 million over budget. The increase in property, plant and equipment as a

result of the revaluations has resulted in significant increases in the draft

2025/26 Annual Plan depreciation budgets.

4.8 The

depreciation expense recognises the consumption and wearing out of tangible

assets over their life, the reported value of the asset reduces by this amount.

The depreciation is included with the rest of the expenses in the financial

statements and rates calculations. In simple terms, the costs of the Council

including an amount of depreciation - are what rates and other income of

Council need to cover to achieve a balanced budget.

4.9 This

funding from rates and other income sources covers the depreciation expense

bringing cash into the Council. In general, this cash is used to fund the

repayment of borrowing incurred in purchasing the assets.

4.10 Asset

revaluations are required under financial reporting standards, and they more

accurately reflect the value, and likely replacement costs of longer life

assets, than their historic cost. Upwards revaluations increase the

depreciation expense, increasing the rates (and other income) required, where

they do exceed the cost of debt servicing, they create a reserve that moderates

the rates impact when renewal does need to

occur.

5. Capital Expenditure by Activity

5.1 The LTP financial budgets assume that

the full capital works programme will not be delivered in its entirety each

year. This historical under-delivery is factored into the forecast net debt

levels and finance costs.

5.2 Changes to the capital programme -

notably the changes approved in the 24 October 2025 Tasman District

Council meeting, and to the Lower Queen Street Bridge Project related changes

in the 13 February 2025 Tasman District Council meeting, lead to

re-phasing and re-prioritisation. These changes in capital expenditure are

reflected in the transfers shown in the table below, with some items being

brought forward and others being rephased to future years.

5.3 Year-to-date

expenditure is 53% of the budget three quarters of the way through the year. It

is, however, sitting at 60% of latest forecast spend. While a ramp up of the

expenditure is expected in the last quarter, a material carry forward into the

2025/26 financial year is also expected. To avoid a carry forward on the

current budget, capital expenditure would have to average approximately $11.8

million per month for April to June 2025. This appears unlikely given the

monthly average expenditure to March is $4.5 million, and the consistent

history of underspent capital budgets in previous years.

5.4 The consistent

capital budget underspends and carry forwards appear to have several causal

factors that include:

5.4.1 An annual cycle of

releasing work.

5.4.2 The multi-year

nature of many projects.

5.4.3 The complexity of

being able to proceed on a project, where there are issues, such as acquiring

land, obtaining resource consents, due process, design changes, external

funders input, and dependencies on other projects finishing first.

5.4.4 Changes to

priorities due to growth, and growth predictions, needed land availability, and

overall budget constraints.

5.5 The organisation needs to

further consider developing a realistically deliverable capital works programme

that incorporates increased efficiencies, this would potentially require

additional focused resources. The Council has indicated through the draft Annual

Plan process that it is not in favour of additional resources currently. Given

the current financial environment including an increasing operational deficit,

the Council is incentivised to avoid increasing debt through capital

expenditure and to defer such expenditure into future years. This approach

needs to be communicated to and understood by the community.

5.6 Budget, spend

and forecast by activity is summarised in the table on the next page.

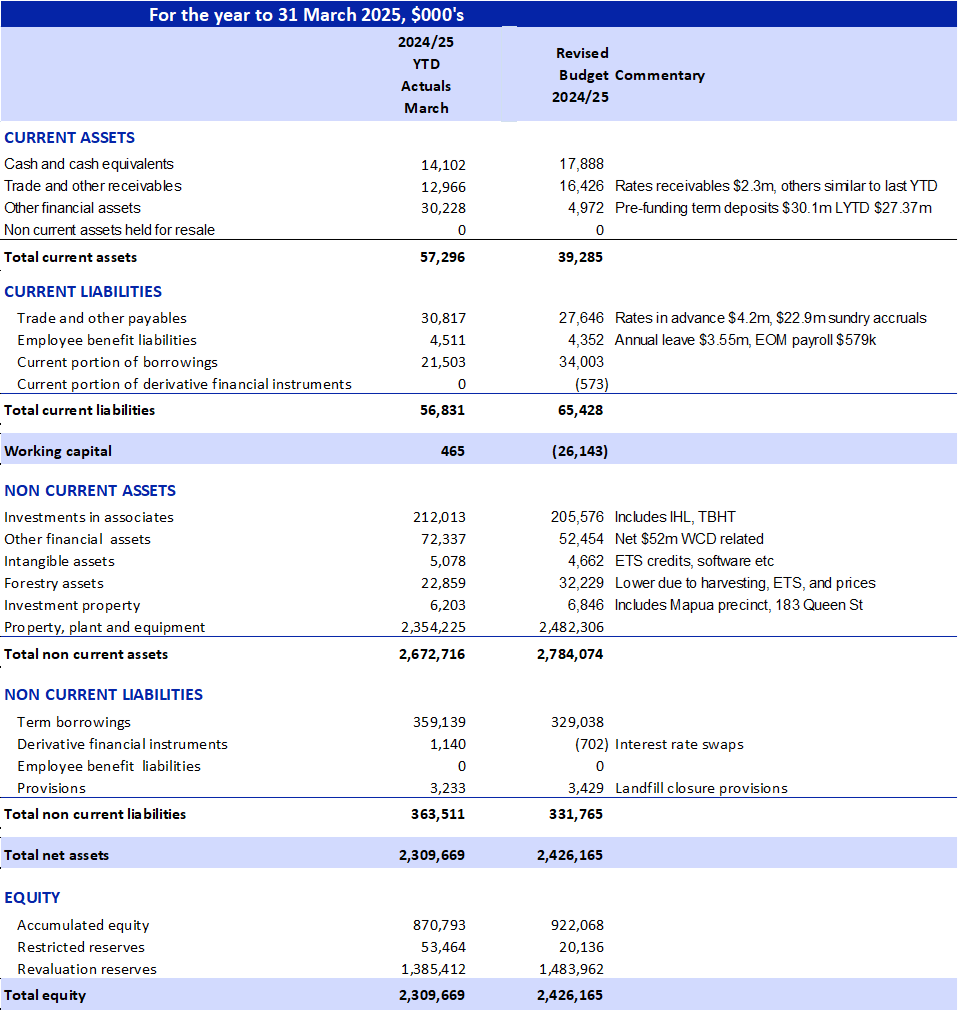

6. Statement of Financial Position (Balance

Sheet)

6.1 The

Statement of Financial Position

7. Net Debt and External Debt

7.1 The Treasury report, that will be

presented at the next Council meeting, will have more detail and analysis in

this area.

7.2 On 31 March 2025, the Council's total

debt of $390.3 million was unchanged from 31 December 2024, and its Net

Debt stood at $266.8 million against a policy limit of $295.1 million

(160% of forecast annual revenue).

7.3 The Pass-through Loans are Shareholder

advances to Waimea Water Limited for funding the Waimea Community Dam. These

loans are excluded in calculating the Council’s Net Debt position. They

are included in assessing the Council’s borrowing from the Local

Government Funding Agency (LGFA) and the LGFA covenants.

7.4 The linked deposits are the Council

pre-funding its April 2025 LGFA loan repayments. This pre-funding is part

of our Treasury borrowing strategy.

Breakdown of net debt

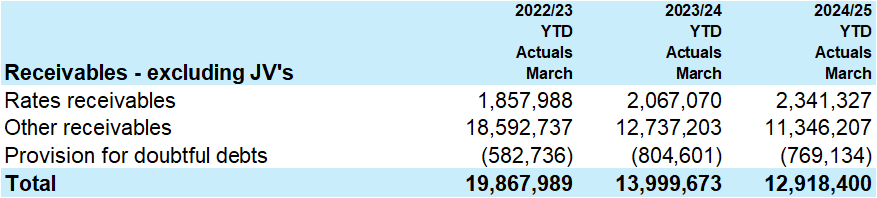

8.1 Rates

receivables are like previous years after allowing for rates income increases.

Other receivables are down on previous years, due largely to reduced forestry

income.

8.2 The receivables

summary is set out below:

Rates

Receivables

8.3 The

number of rates rebate applications are significantly up this year, with the

approval of 240 more rebates than at the same point last year (2023/24),

totalling an extra $200,000 of savings for low-income ratepayers. If this trend

continues, we anticipate over 2,000 successful applications by the end of June.

8.4 While

the Council covers the administration costs of the Rates Rebate scheme the

rebates themselves are refunded to the Council by Central Government.

8.5 The

rates team is proactive in this area and will be sending a letter to previous

applicants who have not yet applied this year, encouraging them to submit their

applications before the end of the rating year.

Other

Receivables

8.6 This includes all other items,

accounting accruals, fees and charges, infringements, forestry debtors, amounts

due from NZTA, development contributions, reserve financial contributions, and

interest receivable etc.

8.7 The $1,400,000 decrease in other

receivables is mostly due to the movement in accounting accruals compared to

March 2024. These accruals are for income such as NZTA, water, refuse and

interest on investments.

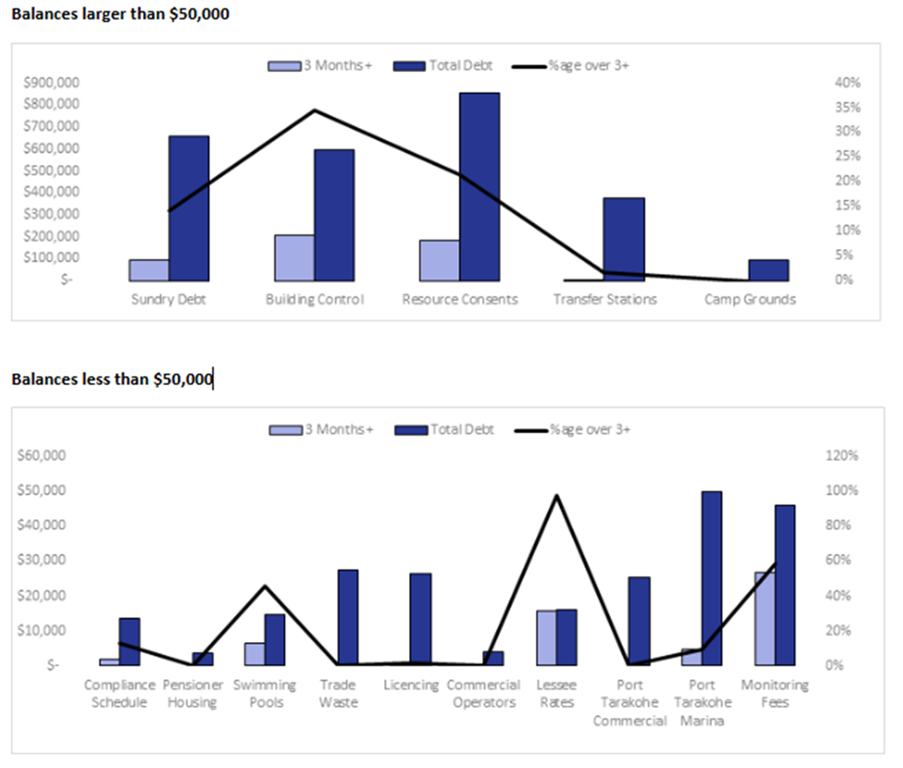

8.8 The following graphs compare debt that

is older than three months with the total debt for each part of the Council.

These have been separated between balances over $50,000 and balances under

$50,000 for scaling purposes to provide a meaningful graph of the smaller

balances.

8.9 The ten largest debts exceeding three

months in age amount to $332,000. These are primarily concentrated in Building

Control ($110,000 from four debtors) and Resource Consents ($106,000 from two

debtors). Additionally, there are two sundry debts totalling $66,000 and one

instance of unpaid monitoring charges ($35,000). Active recovery action is

underway for all these debts. The remaining balance of $15,000 pertains to

outstanding community lessee rates on charging.

Nil

Tasman District

Council

Agenda – 08 May 2025

7.3 2024/25 Forecast Overspend

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

8

May 2025

|

|

Report

Author:

|

Matthew

McGlinchey, Financial Performance Manager

|

|

Report

Authorisers:

|

Mike

Drummond, Chief Financial Officer

|

|

Report

Number:

|

RCN25-05-4

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 To

gain approval for $6.4 million in unbudgeted rates funded operational expenditure

in the 2024/2025 Annual Plan year. Noting that the Council passed a resolution

on 30 April 2025 to partly fund this offset forecast overspend by the sale of

$3.0 million of unencumbered emissions trading scheme (ETS) credits.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 The

Council expects to be an overall $6.4 million overspent on operational costs in

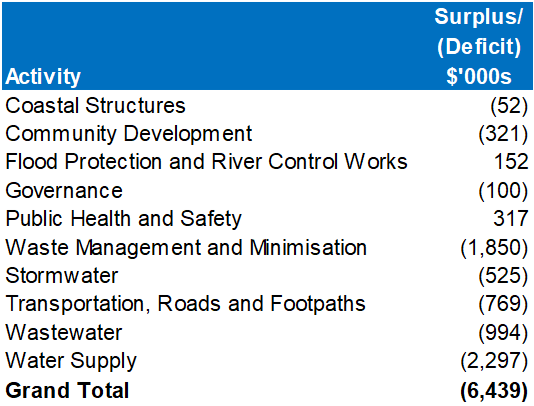

the 2024/2025 financial year. Table 1 illustrates where the material overspends

will occur. Noting that some activities have an overall surplus forecast.

2.2 An

increase in interest rates and maintenance costs in the Community

Infrastructure area are the main drivers of the forecast expenditure overspend.

2.3 The

Council’s level of borrowing ($309 million gross debt at 31 March 2025)

means that relatively small movements in interest rates can have a significant

impact on finance costs. Those cost pressures are concentrated in

infrastructure activities which have the bulk of the Council debt.

2.4 Funds

collected via targeted rates and/or fees and charges for one activity cannot be

used in another activity. The only exception is the General Rate and the

Uniform Annual General Charge (UAGC) which can be used for any activity.

2.5 Staff have made every effort to try to mitigate the planned

overspend. A business review process has been undertaken to review levels of

service and find operational cost savings. This work has been significant and

has occurred over the last six months. The work has also fed into the draft

Annual Plan 2025/2026 process.

2.6 Selling

further unencumbered ETS to the value of $3.0 million prior to 30 June 2025,

will mean the year end deficit could be reduced to $3.4 million. This remaining

$3.4 million will be loan funded and is proposed to be recovered over five

years at approximately $700,000 per annum commencing from the 2026/2027 Annual

Plan year.

Table 1

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman

District Council

1. receives

the 2024/25 Forecast Overspend report RCN25-05-4; and

2. notes

the forecast underspends in the following activities:

2.1 Flood

Protection and River Control work $152,000

2.2 Public

Health & Safety $317,000; and

3. approves the forecast unbudgeted operational

expenditure in the following activities:

3.3 Coastal Structures $52,000

3.4 Reserves and Facilities $321,000

3.5 Governance $100,000

3.6 Waste Management and Minimisation $1.85 million

3.7 Stormwater $525,000

3.8 Transportation, Roads and Footpaths $770,000

3.9 Wastewater $995,000

3.10 Water Supply $2.3 million; and

4. confirms

the sale of approximately $3 million of unencumbered emissions trading scheme

credits prior to 30 June 2025, subject to professional

advice on staging the sales to achieve the best overall price.

5. delegates

to the Chief Executive Officer and Chief Financial Officer the authority to

enter into the sale of the unencumbered emissions trading scheme credits and

sign any associated document required to give effect that sale; and

6. approves

the allocation of the proceeds of the proposed $3.0 million emissions trading

scheme sales against debt financing costs as follows:

6.11 Reserves and Facilities $500,000

6.12 Transportation, Roads and Footpaths $500,000

6.13 Wastewater $1.0 million

6.14 Water Supply $1.0 million; and

7. approves use of Waste Disposal Levy funding for transport of

recyclable materials, public place recycling, development of waste policy and

diversion of hazardous waste from landfill; and

8. approves

that the final 2024/2025 Operational deficit, forecast to be $3.4 million is

financed through additional borrowing and repaid over the following five years

commencing in 2025/2026.

4.1 In September of this financial year,

staff became aware that it was most likely that the Council would be overspent

in certain activity areas because of higher than budgeted maintenance and

interest costs.

4.2 If overspends are expected to occur and

there is no offsetting underspend, then staff are required to get this

unbudgeted expenditure approved by the Council, in line with the

Council’s delegations. Noting that this approval is required prior to the

overspend occurring.

4.3 Staff expect the overspend of existing

annual budgets to start occurring in May 2025.

4.4 Staff have made every effort to try to

mitigate the planned overspend. A business review process has been undertaken

to review levels of service and find operational cost savings. This work has

been significant and has occurred over the last six months. This work has also

fed into the draft Annual Plan 2025/2026 process.

4.5 Despite these measures, the Council

still expects to be in an increased forecast deficit position compared to the

Long Term Plan (LTP) budget operational deficit as at 30 June

2025.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 There are several activities that will have unbudgeted expenditure,

i.e. will be overspent as at 30 June, and a number that will be underspent. The

next part of this report explains what the high-level drivers are for the

overspend at the activity level.

Coastal Structures - Forecast $52,000 over budget

5.2 Coastal Structures Maintenance $24,000:

The maintenance budget overspend was driven by unexpected repairs needed for

coastal structures. Severe weather conditions caused more damage than

anticipated, necessitating unbudgeted maintenance work.

5.3 Debt financing costs of $24,000: The

higher interest costs were a result of higher interest rates on existing loans

than were budgeted.

Parks and Reserves Forecast $321,000 over budget

5.4 Debt financing costs of $60,000: The

higher interest costs were a result of higher interest rates on existing loans

than were budgeted.

5.5 Unbudgeted maintenance costs $240,000:

The increase in expenditure is partly due to the increase in the number of

reserves the Council has to maintain. There has been an increase of

approximately 102 hectares of reserve area since July 2020. Maintenance for

these areas has now been included in the Annual Plan 2025/2026 budget.

Building - forecast surplus of $317,000

5.6 Additional revenue in the building area.

Staff were conservative in the Long Term Plan (LTP) given the economic climate.

Fees collected in this space have been higher than what was budgeted.

Flood Protection and River Control Works – forecast

surplus of $152,000

5.7 Debt financing costs of $101,000: The

higher interest costs were a result of higher interest rates on existing loans

than were budgeted.

5.8 Additional Gravel Sales of $250,000:

Offsetting the higher interest rates was the collection of gravel income over

and above budget expectations.

Governance – forecast deficit of

$100,000

5.9 SOLGM (Taituarā) subscriptions

$104,000: No budget was allowed for in the LTP for this, because of a budgeting

error. This has been corrected in the 2025/2026 Annual Plan. This provides an

avenue to build off sector advice and is very beneficial to Tasman District

Council.

Waste Management and Minimisation - forecast deficit of $1.85 million

5.10 Debt financing costs of $388,000: The higher

interest costs were a result of higher interest rates on existing loans than

were budgeted.

5.11 The kerbside collection closed account is funded by

a targeted rate and some charges for commercial recycling. We are forecasting a

$580,000 deficit for this account, largely due to an inadvertent error in not

including funding for the Material Recycling Facility (MRF) in the Long Term

Plan 2024/2034 ($300,000), additional collection costs due to an agreed

extension of the existing contract ($100,000), additional legal and procurement

costs ($140,000) and reduced commercial revenue ($70,000).

5.12 The Resource Recovery

Centre (RRC) closed account is largely funded by gate fees and we are

forecasting a $820,000 deficit in this account. This is due to a decrease in

net revenue from waste received ($485,000), increased reactive maintenance

($140,000, 100% increase), routine maintenance ($125,000, 234%) and site

operations ($100,000, 8%). The reduction in net revenue is largely due to a 45%

drop in revenue at Richmond RRC, increased reactive maintenance largely due to

compactor and waste bin repairs and routine maintenance due to contractual

obligations and good asset management limiting savings budgeted in the LTP.

5.13 The illegal dumping and

hazardous waste activity is funded by the General Rate and we are forecasting a

$70,000 deficit. This is largely driven by increased illegal dumping collection

and disposal costs ($33,000 and $10,000) and costs to identify illegal dumping

offenders ($26,000).

5.14 The waste minimisation

account is fully funded by the central government Waste Disposal Levy and is

forecast to conclude the year on budget. We are proposing to fund transport of

recyclable materials, public place recycling, development of waste policy and

diversion of hazardous waste from landfill from this account and this was not

previously budgeted.

Stormwater - forecast deficit of

$525,000

5.15 Debt financing costs of $428,000: The higher

interest costs were a result of higher interest rates on existing loans than

were budgeted.

5.16 Miscellaneous Costs $97,000: Reactive

maintenance costs from maintaining waterways are higher as well as insurance

costs that will mean an unbudgeted overspend occurs.

Transportation, Roads and Footpaths -

forecast deficit of $770,000

5.17 Debt financing costs of $392,000: The higher

interest costs were a result of higher interest rates on existing loans than

were budgeted.

5.18 Landscape maintenance (street trees and planted

garden beds) costs of $200,000. It is noted that this budget was reduced by 50%

in the LTP, compared to previous year.

5.19 Litter bin clearing $240,000 – The funding

was inadvertently removed from the LTP for this activity. Discontinuing work

this financial year is not considered a valid option and no consultation has

occurred on what would be a significant change in level of service to the

community if the Council removed the litter bins.

Wastewater - forecast deficit of

$995,000

5.20 Debt financing costs of $875,000: The higher

interest costs were a result of higher interest rates on existing loans than

were budgeted.

5.21 Maintenance $242,000: The Wastewater activity has a

forecast over-expenditure of $242,000 and this is primarily due to the

increased reactive maintenance that has occurred to date.

5.22 It is noted that if sewer blockages continue at the

same rate as experienced to date, then the forecast over-expenditure will be

realised. However, if it reduces then the forecast deficit should reduce as

well.

Water Supply - forecast deficit of $2.3

million

5.23 Debt financing costs of $380,000: The higher

interest costs were a result of higher interest rates on existing loans than

were budgeted.

5.24 Water Maintenance $1.8 million: Higher reactive

maintenance costs have been incurred throughout the year. Around 80% of this

forecast overrun is in the Water Supply activity and primarily because of the

increased level of reactive maintenance.

5.25 The inadvertent removal of around $523,000

funding in the Long Term Plan 2024/2034 for routine monitoring and maintenance

has also contributed to the over-expenditure. This funding has been reinstated

in the Annual Plan 2025/2026.

Sale of the unencumbered ETS credits

5.26 ETS

Market Conditions - The ETS market does go through periods of increased

volatility and then can go through periods where it is a bit more composed. It

is always hard to look forward and see where we may be or what the dynamic

would look like in a few months. The Jarden Group (an independent investment

and advisory group) have advised the Council in April:

“that for example, NZUs

in the mid $50s now have surprised many. The weakness at the moment appears to

be driven by the apparent oversupply of NZUs and the volume that is sitting in

the stockpile overhanging the market. First auction of the year declined with

no bids and there are plenty of foresters selling to raise funds which has kept

pressure on the price.”

5.27 Other

advice from PF Olsen suggests:

“prices have tended to

be subdued from Jan to April and pick up from May onwards. While we cannot

guarantee that prices will rally again as of this May, the historic trend

suggests they are likely to. For this reason, our recommendation would be to

hold off selling NZUs till, say, mid-May and then start selling in 10k

increments over a month or two to average out any spot price fluctuations.”

5.28 For

these reasons, staff recommend that the actual sale timetable be agreed with

professional advisors with a clear view to sell prior to 30 June 2025, but

still subject to professional advice on staging the sales to achieve the best

overall price.

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

6.1 The Council is expecting to be overspent

by a net $6.4 million at the end of this financial year. This can be reduced to

$3.4 million by selling $3.0 million of unencumbered ETS credits before 30 June

2025.

6.2 This will mean that over the following

five years, the Council will have to rate for an additional $3.4 million

(plus interest) to fund this year’s increased operational deficit.

6.3 While this will create additional rating

pressure in future years, it will mean the Council can spread the impact out

over five years rather than rating for the full $3.4 million in the 2025/2026

year.

6.4 Repaying the deficit over five years

will result in a higher net debt figure for the Council than initially planned.

This revised figure for 2025/2026 will be included in the Council's approval of

the final Annual Plan 2025/2026 scheduled for the Council meeting on 25 June

2025.

6.5 The Council has already committed to

selling $3.0 million of unencumbered ETS credits overseen by the Enterprise

Activity to seed fund a Diversified Resilience Fund. This proposal to sell a

further $3.0 million of unencumbered ETS credits will leave few credits

available for future use.

7.1 The options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Approve the overall $6.4 million

rates funded over expenditure and approve the sale of $3.0 million of

unencumbered ETS credits before 30 June 2025.

|

The Council will not breach the

expenditure rules set out in its delegation register.

The essential work carried out that

caused budgets to be exceeded will be funded.

The sale of ETS credits reduces the

future impacts on rates increases.

|

It creates a precedent that unbudgeted

expenditure will be approved.

Overspending the approved budgets will

impact the Council’s goodwill and confidence within the community

|

|

2.

|

Decline to approve the $6.4 million rates

overspend and decline to approve the sale of $3.0 million of unencumbered ETS

credits before 30 June.

|

The Council will breach the staff

delegation register and have unauthorised and unbudgeted expenditure.

The Council would need to provide clear

direction around what to stop operational spending on in May and June 2025 to

ensure it does not overspend the total budget by 30 June 2025. This approach

would not be a realistic option.

|

The delegation register was created as a

mechanism to allow staff to gain approval for overspends. Not approving would

suggest that the delegation register needs to be amended.

The Council will breach the delegation

register. At this stage of the financial year, it would be impossible not to

overspend.

|

7.2 Option 1 is recommended.

8.1 A key enabling document that Tasman

District Council has is the delegations document. This is where the Council

agrees what delegations are given to the Chief Executive and staff. The Chief

Executive is obligated to ensure that Council staff operate within those

delegations.

8.2 At present, Tasman District Council will

breach those delegations for having unbudgeted and unauthorised expenditure

unless the Council approves the additional funding requested in this report.

8.3 This report ensures that the additional

expenditure is appropriately authorised, and funding agreed.

9. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

9.1 Staff have assessed the significance of

most of the decisions proposed in this report. The significance of the combined

set of changes including the authorisation of additional unbudgeted expenditure

is considered to be medium.

9.2 No formal engagement is proposed as the

elected members can rely on their knowledge of the views and preferences of

their communities in making a decision.

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Medium

|

Generally low but

some members of the community with a particular interest in Council finances

will have a higher interest.

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the community

in the present or future?

|

Yes

|

The Annual Plan for

2025/2026 and the following four financial years will increase rates to

recover the $3.5 million rates overspend and additional interest

payments.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

No

|

The Annual Plan for

2025/2026 and the following four financial years will increase rates to

recover the $3.5 million rates overspend and additional interest

payments.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

No

|

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

No

|

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

medium

|

The impacts of

repaying the $3.5 million deficit over the following five years will raise

rates approximately 0.5% per annum.

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

No

|

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

No

|

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

No

|

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

No

|

|

10. Communication

/ Whakawhitiwhiti Kōrero

10.1 The Council anticipates issuing a press release

regarding this item and the decision at the conclusion of the meeting.

11.1 The recommendation to approve unbudgeted operating

expenditure, if approved, mitigates the risk of spending an amount higher than

the authorised 2024/25 budget.

11.2 There

is a risk that the sale of ETS credits is delayed or does not achieve the

financial outcome sought. To mitigate this risk the actual sale timetable will

be discussed and be agreed with our professional advisors with a clear view to

sell prior to 30 June 2025, but subject to professional advice on staging the

sales to achieve the best overall price.

12. Climate

Change Considerations / Whakaaro

Whakaaweawe Āhuarangi

12.1 The overall impact if any on climate resilience and

adaptation is likely to be minor.

13. Alignment

with Policy and Strategic Plans / Te Hangai ki ngā aupapa Here me ngā

Mahere Rautaki Tūraru

13.1 The Council is attempting to deliver on its vision Thriving

and Resilient Tasman Communities and the strategic priorities in the LTP

2024-2034. This approval will ensure it is very transparent around breaches to

its delegation document and ultimately its Financial Strategy.

14. Conclusion

/ Kupu Whakatepe

14.1 By agreeing to the annual budget overspends and

allowing staff to mitigate the overspends by selling ETS credits, the Council

will ensure it remains within its Council approved delegations while mitigating

the financial impact on ratepayers.

15. Next

Steps and Timeline / Ngā Mahi Whai Ake

15.1 Staff anticipate issuing a press release regarding

this item and the decision at the conclusion of the meeting.

15.2 Proceed to engage with our advisors and move to sell the

unencumbered ETS credits to release $3.0 million of additional funds to partly

offset the forecast overspend.

Nil

Tasman District

Council

Agenda – 08 May 2025

7.4 Hamama Water Supply - Approval for Renewal

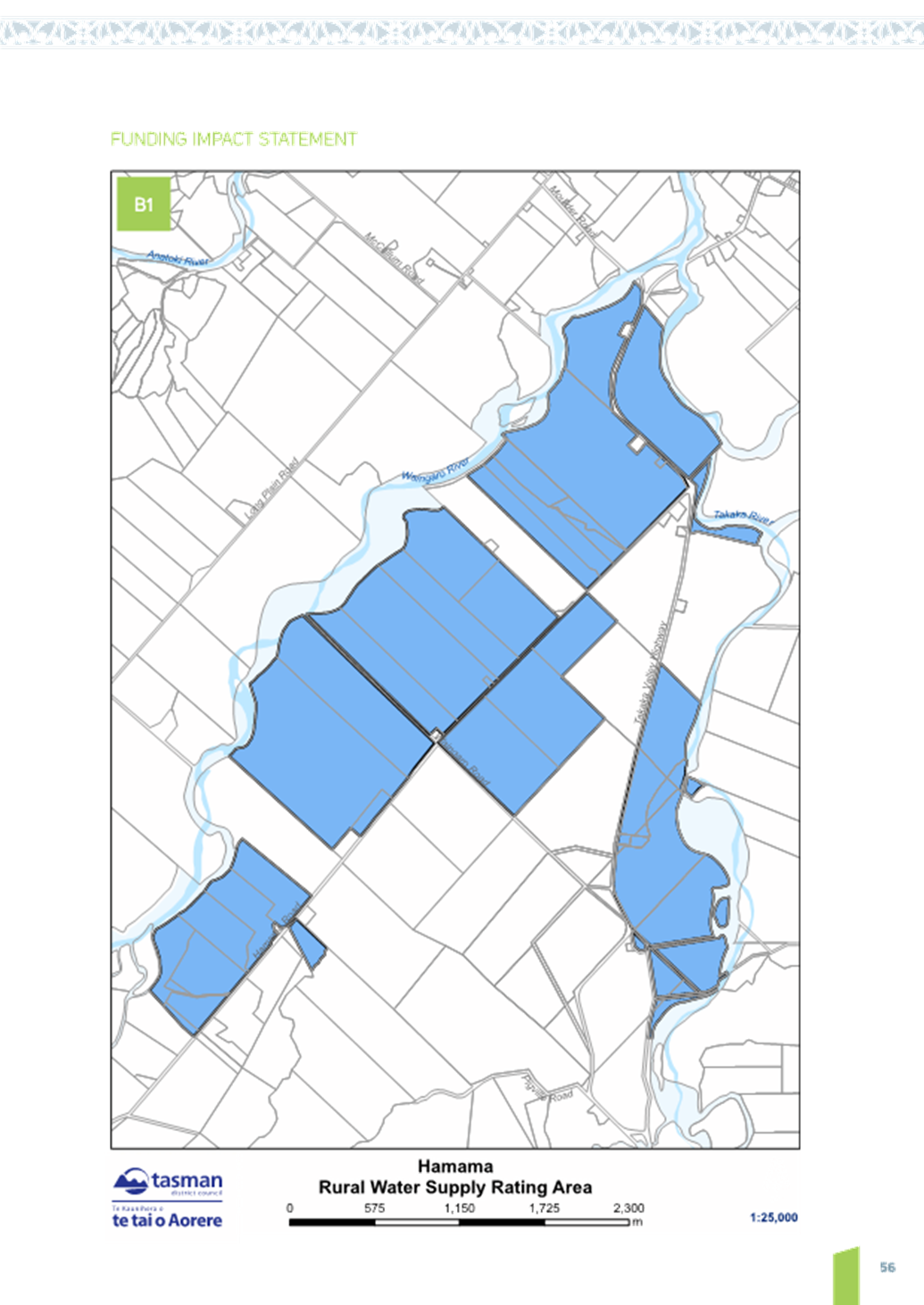

Expenditure

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

8

May 2025

|

|

Report

Author:

|

Carl

Botha, Team Leader-Water Supply; Mike Schruer, Waters and Wastes Manager;

Matthew McGlinchey, Financial Performance Manager

|

|

Report

Authorisers:

|

Richard

Kirby, Group Manager - Community Infrastructure

|

|

Report

Number:

|

RCN25-05-5

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 The

purpose of this report is to seek approval from the Council for unbudgeted

expenditure related to a section of pipe renewal in the Hamama Water Supply

Scheme.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 The

Hamama Water Supply Scheme operates as a closed account, which is managed by

the Hamama Water Supply Committee. The Council's involvement is primarily to

collect the rates on behalf of the Committee.

2.2 The

account balance as at 1 July 2024 was $56,720, and none of this has been spent

since 1 July 2024.

2.3 The

Hamama Water Supply Committee has proposed a pipe renewal project that will

cover approximately 200 metres, with an estimated cost of $20,000. Currently,

there is no budget allocated in the Long-Term Plan 2024/2034 for this specific

project. However, the Committee wants to utilise some of its account balance to

fund the project. As a result, this expenditure will not directly impact the

Hamama Water Supply rates.

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman District Council

1. receives the Hamama Water

Supply - Approval for Renewal Expenditure report, RCN25-05-5; and

2. approves

unbudgeted Capital expenditure of $20,000 from the Hamama Water Supply account balance of $56,720; and

3. notes

that the Hamama Water Supply Committee has not confirmed when the expenditure

will be incurred, so $20,000 will be allocated as a spend in the 2024/2025

financial year and any outstanding funding from 2024/2025 will be included in

the carry forward report for 2025/2026.

4.1 The Hamama Water Supply Scheme includes

old water supply pipes that were installed in 1959. The Committee has

systematically renewed these pipes as needed, particularly when there is an

increase in failures in specific sections of the network.

4.2 The current project involves renewing a

200-metre section of pipeline, which is connect to a 600-metre section that was

previously renewed. This section that is being renewed is part of the main

pipeline from the storage tanks and prior to any connections, therefore, it is

the main supply to the community.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 Context

5.1.1 The Hamama Water Supply scheme has ageing infrastructure,

specifically the old water supply pipes installed in 1959. These pipes have

been prone to failures, necessitating systematic renewals to increase the

reliability of the water supply to the community.

5.2 Proposed

Action

5.2.1 The Hamama Water Supply Committee has requested approval to

renew a 200-metre section of the trunk main that is connected to a previously

renewed 600-metre section. This section of trunk main renewal is essential to

maintain the integrity of supply from the storage tanks and before any

connections to the community.

5.2.2 The Committee has not confirmed the timing of this work so it

is unclear what expenditure will occur in 2024/25 and whether some or all of it

will be incurred in 2025/2026.

5.3 Rationale

5.3.1 Infrastructure integrity: Renewing this section of the

pipeline will enhance the reliability and efficiency of the water supply

system, reducing the risk of failures and ensuring a consistent water supply to

the community.

5.3.2 Financial viability: The project is financially viable as the

Hamama Water Supply Committee has requested that some of the account balance of

$56,720 be utilised to fund the $20,000 renewal. The account balance is a

consequence of under expenditure in previous years and has been funded from

Hamama Water Supply rates so there is no need to increase rates to recover this

cost.

5.3.3 Community impact: Ensuring a reliable water supply is critical

for the well-being of the community, and this project will reduce the risk of

further disruptions.

5.4 Conclusion

5.4.1 The proposed pipe renewal project is a necessary investment in

the Hamama Water Supply Scheme's infrastructure. By utilising the account

balance, the project can be completed without impacting the rates for Hamama,

ensuring both financial prudence and community benefit. Approval for this

unbudgeted expenditure is recommended to proceed with the project and enhance

the water supply system's integrity.

6.1 The options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Approve unbudgeted expenditure

|

Ensures a reliable water supply and

reduces the risk of water loss due to pipe failures, promoting efficient

water use.

Utilises existing reserve funds, avoiding

additional financial burden on community.

|

Utilises a significant portion of the

reserve funds, potentially limiting resources for future projects.

Construction activities may temporarily

disrupt the local environment.

|

|

2.

|

Defer pipe renewal project

|

Preserves the reserve funds for other

potential urgent needs or future projects.

Avoids immediate environmental disruption

from construction activities.

|

Increased risk of water supply

disruptions due to potential pipe failures, and continued risk of water loss

due to leaks in the aging pipeline.

Potential higher costs in the future if

the pipe condition worsens and emergency repairs are needed.

May erode community trust.

|

|

3.

|

Partial renewal of pipeline

|

Addresses the most critical sections of

the pipeline, reducing the risk of immediate failures.

Minimises immediate environmental

disruption by limiting the scope of construction.

|

Continued risk of water loss in sections

not renewed, as partial renewal may not fully resolve the reliability issues,

leading to potential future disruptions.

May result in higher overall costs if

multiple partial renewals are needed over time.

May lead to mixed perceptions within the

community regarding the adequacy of the solution.

|

6.2 Staff recommend Option 1, to approve the

unbudgeted expenditure.

7.1 There are no significant legal matters

arising from this decision. The Council can authorise unbudgeted expenditure

from reserve of funds.

8. Iwi

Engagement / Whakawhitiwhiti ā-Hapori Māori

8.1 No engagement with Iwi has been

initiated regarding the unbudgeted expenditure required for the pipe renewal

project.

9. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

9.1 We have considered the significance of

this decision to be Low and consider that there is no further engagement

or consultation required for the Council to make this decision.

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Low

|

The decision to use reserve funds for the pipe renewal project is unlikely to

generate high public interest or controversy, as it involves utilising

existing reserve funds without impacting the rates.

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Low

|

The project will have

positive social and environmental impacts by ensuring a reliable water supply

and reducing the risk of pipe failures.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Low

|

The impact of the

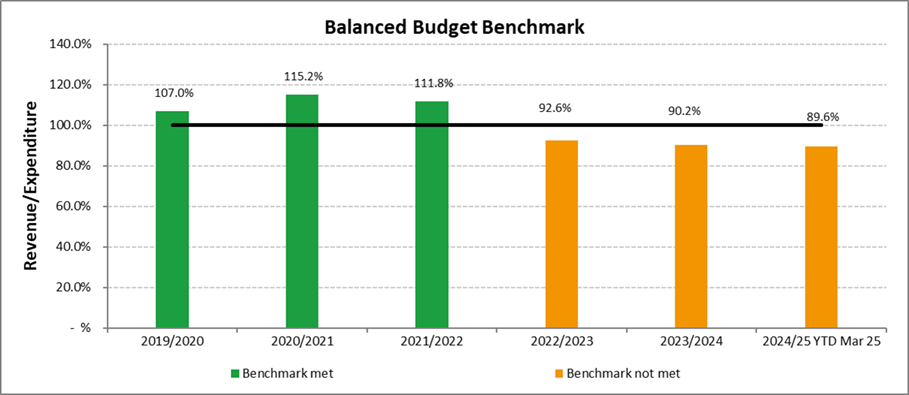

pipe renewal project is expected to be long-term, as it will enhance the

infrastructure and reliability of the water supply system.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

Low

|

The water supply

infrastructure is considered a strategic asset, essential for the community's

well-being and daily operations.

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

Low

|

The decision aims to

maintain and improve the existing service levels by addressing infrastructure

needs.

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

Low

|

The proposal utilises

reserve funds from the closed account managed by the Hamama

Committee.

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

N/A

|

The decision does not

involve the sale of any interest in a CCO or CCTO.

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

N/A

|

The proposal does not

involve entering a private sector partnership or contract for the delivery of

Council activities.

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

N/A

|

The decision does not

involve the Council exiting from or entering a new group of activities.

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

Low

|

This decision does

not require consideration of the obligations of Te Mana O Te Wai relating to

freshwater.

|

10. Communication

/ Whakawhitiwhiti Kōrero

10.1 The Hamama Water Supply Committee has approached

the Waters and Wastes Team regarding its proposal for the pipe renewal project,

emphasising the need for approval of unbudgeted expenditure amounting to

$20,000. This expenditure is to be funded from the existing closed account reserve

of $56,720, ensuring that there will be no immediate impact on the Hamama Water

Supply rates. The Committee has already agreed to proceed with the project and

now seeks the Council's formal approval to utilise the reserve funds for this

essential infrastructure upgrade.

11. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

11.1 There is an existing reserve which will fund the

$20,000. The reserve has been built up over several years. The build-up has

occurred because planned work was not required as expected and also because the

reserve balance gets interest revenue from the Councils internal treasury

function.

11.2 Using $20,000 for this project will deplete the

reserve but it is being spent on a project that has benefit across the scheme.

However, the spend is exactly what a reserve like this should be spent on.

12.1 Proceeding with proposal

12.1.1 Financial

risk is low as utilising $20,000 from reserve of $56,720.

12.1.2 Environmental

risk is medium due to temporary disruption to local environment.

12.1.3 Operational

risk is low due to temporary disruption to water supply during construction.

12.1.4 Reputational

risk is low as the Council does not manage the water supply, only collects the

rates for the scheme.

12.2 Not proceeding with proposal

12.2.1 Infrastructure

risk is high as the likelihood of failures increase due to aging pipes.

12.2.2 Financial

risk is medium as delaying the project may result in higher costs in the future

due to deterioration of pipes and emergency repairs.

12.2.3 Social risk

is high as water disruptions can negatively impact the community’s

quality of life.

12.2.4 Reputational

risk is high as failing to address the aging infrastructure may erode community

trust.

13. Climate

Change Considerations / Whakaaro

Whakaaweawe Āhuarangi

13.1 The proposal in this report was considered by staff

in accordance with the process set out in the Council’s ‘Climate

Change Consideration Guide’.

13.2 The pipe renewal project enhances the resilience of

the water supply system and reduces environmental impact by improving leak

prevention, thereby conserving water.

14. Alignment

with Policy and Strategic Plans / Te Hangai ki ngā aupapa Here me ngā

Mahere Rautaki Tūraru

14.1 This funding recommendation is generally in

accordance with the Council’s Policy and Strategic Plans.

15. Conclusion

/ Kupu Whakatepe

15.1 Staff recommend that the unbudgeted expenditure be

approved from the reserve funds to allow for better future resilience and

reliability of the Hamama Water Supply Scheme. This approval will ensure that

the necessary pipe renewal project can proceed without impacting the existing

budget or rates, thereby enhancing the infrastructure and securing a

sustainable water supply for the community.

16. Next

Steps and Timeline / Ngā Mahi Whai Ake

16.1 If this unbudgeted expenditure is approved, approved budgets will be

updated, and reserve funding will be used for the pipe renewal project.

Nil

Tasman District

Council

Agenda – 08 May 2025

7.5 Chlorination Exemption for Upper Tākaka

Water Supply

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

8

May 2025

|

|

Report

Author:

|

Evan

McKenzie, Team Leader - Water Quality & Safety; Mike Schruer, Waters and

Wastes Manager

|

|

Report

Authorisers:

|

Richard

Kirby, Group Manager - Community Infrastructure

|

|

Report

Number:

|

RCN25-05-6

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 To

inform the Council of our legal obligation under the Water Services Act to

either chlorinate Upper Tākaka Water Supply or seek an exemption from the

requirement to provide residual disinfection.

1.2 To

advise that the Water Services Authority – Taumata Arowai expects the

Council to inform them of how we will address the lack of a residual

disinfection by 9 May 2025.

1.3 To

seek approval from the Council to apply to the Water Services Authority for an

exemption.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 Section

31(j) of the Water Services Act requires water suppliers to provide for

residual disinfection within their water supply reticulation unless an

exemption from this requirement is obtained from the Water Services Regulator.

There are no viable alternatives to using chlorine as the residual

disinfectant.

2.2 The

Regulator wrote to Council staff on 31 March 2025 to request our plan of how we

will address the current lack of residual disinfection in the Upper Tākaka

supply. This plan is required by 9 May 2025 although the Regulator has advised

there is some flexibility with this date.

2.3 There

is significant cost to install permanent chlorination for a small population

however there does remain a low risk to public health in the absence of

chlorination.

2.4 Council

staff intend to apply for an exemption from the residual disinfection

requirement however there is a need seek the Council’s endorsement of

this approach.

2.5 If

an exemption is applied for, there is no guarantee that it will be granted and

if not, the Council will be required to install chlorination within a timeframe

that is acceptable to the Regulator.

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman

District Council

1. receives

the Chlorination Exemption for Upper Tākaka Water Supply report,

RCN25-05-6; and

2. approves the compliance approach of seeking an

exemption from the requirement to provide for residual disinfection of the

Upper Tākaka Water Supply.

4.1 District-wide

consultation was held in 2020 regarding the Council’s intention to

chlorinate all its water supplies and the feedback from a limited number of

Upper Tākaka residents was that they did not want chlorine. The Council

resolved to chlorinate all supplies however deferred this for Upper Tākaka

in anticipation of the new Water Services Act and associated rules.

4.2 The

Act confirmed that residual disinfection would be required for all water

supplies, regardless of population served and the Regulator is now requiring

the plan referred to in 2.2 above.

4.3 Council

staff are currently conducting an informal email survey of residents to

re-assess their appetite for permanent chlorination. Results are expected prior

to 8 May 2025.

4.4 The

estimated cost of installing permanent chlorination is $150,000 with ongoing

operational costs thereafter.

4.5 The

lack of residual disinfection does pose a risk of contamination and public

health harm, for example from pipe breaks, backflow and if the main UV and

filtration treatment system fails for any reason. However, because the

population served (35) is small and the pipe network short and substantial

storage is available in the event of a treatment malfunction, the risk is

likely to be low.

4.6 The exemption application process

involves an upfront fee of $5200 plus GST and any further costs that the

Regulator might incur in the course of its assessment.

4.7 The application itself must cover a

range of information that the Regulator specifies within its website guidance.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 The issue is that there is a legal

compulsion to permanently chlorinate the Upper Tākaka water supply but

this appears to be opposed by the majority of residents and comes at

significant cost.

5.2 Council staff are of the view that the

public health risk is currently adequately managed and that there is no

evidence that illness has been caused within the resident population because of

there being no residual disinfection.

5.3 In essence, the benefit for the

approximately 35 residents is likely to be outweighed by the costs associated

with installing and operating permanent chlorination.

5.4 If an exemption application is rejected,

staff accept that there will be no alternative to achieving compliance with the

Water Services Act 31(j) than to install chlorination.

5.5 If an exemption was successful, the

Council must re-apply for a continuation every five years.

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

6.1 The financial implications of both

approaches are below:

6.2 Seek exemption from chlorination

6.2.1 Application fees - upfront fee $5,200 and up to an estimated

$5,000 in additional costs passed on by the Regulator during their review

process.

6.2.2 Fees every five years to renew exemption – estimated

$5,000 - $10,000.

6.3 Put

chlorination in place for Upper Tākaka water

supply

6.3.1 The capital cost of chlorination equipment was estimated in

November 2024 at $150,000.

6.3.2 The ongoing cost to operate, test, and maintain the

chlorination equipment and processes is estimated at $10,000 p.a.

6.3.3 These capital and operational costs are not specifically

budgeted for but can be accommodated within the overall urban water club

capital budget.

6.3.4 The cost of servicing the loan on the capital cost will be

$8,000-13,000 p.a.

6.4 There is currently no budget allocated

for this cost.

7.1 The two options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Apply for an exemption to the requirement

to chlorinate.

|

If approved, the Council will be in

compliance with section 31(j) of the Act for at least a period of five years.

No extra capital or operational

expenditure associated with installation of chlorination.

|

If approved, low health risk due to lack

of residual disinfection barrier to contamination.

|

|

2.

|

Install chlorination

|

Adds a barrier to contamination in the

supply that doesn’t currently exist.

|

Low benefit to cost ratio.

Likely to be contrary to majority of

residents’ preferences.

|

7.2 Option 1 is recommended.

8.1 Water Services Act – section 31(j)

– Requirement to provide for residual disinfection;

8.2 Water Services Act – section 58

– Exemptions to residual disinfection

9. Iwi

Engagement / Whakawhitiwhiti ā-Hapori Māori

9.1 Iwi have not been engaged regarding the

proposed exemption application. Staff consider that this issue is confined to

the Upper Tākaka community of approximately 33 residents.

10. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

High

|

High level of

interest within Upper Tākaka community as measured by email survey

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Moderate

|

Unlikely to be

significant direct cultural/economic/environmental effects on community if an

exemption is not obtained and chlorination implemented.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Moderate

|

Unless an exemption

is obtained, chlorination will become permanent.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

No

|

Although the

Council’s water supplies are a strategic asset the Upper Tākaka

water treatment plant and reticulation system is a small component of the

Council’s water supply activity

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

Moderate

|

A decision to seek an

exemption from chlorination will not in itself change levels of service. A

decision not to seek an exemption will result in a definite requirement to

chlorinate and that would change the Level of Service for the Upper Takaka

water consumers.

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

Moderate

|

Estimated capital

cost of implementing chlorination $150,000 plus approximately $10,000 p.a.