Notice

is given that an ordinary meeting of the Audit and Risk Committee will be held

on:

MEMBERSHIP

|

Chairperson

|

Mr G McGlinn

|

|

|

Councillors

|

Deputy Mayor S Bryant

|

|

|

|

Councillor C Butler

|

|

|

|

Ms A Elstob

|

|

|

|

Mayor T King

|

|

|

|

Councillor C Mackenzie

|

|

|

|

Councillor T Walker

|

|

(Quorum 3 members)

Audit and Risk

Committee

Agenda – 03 October 2024

AGENDA

1 Opening, Welcome, KARAKIA

2 Apologies

and Leave of Absence

|

Recommendation

That apologies be accepted.

|

3 Declarations

of Interest

4 LATE

ITEMS

5 Confirmation

of minutes

|

That the minutes of

the Audit and Risk Committee meeting held on Wednesday, 10 July 2024, be

confirmed as a true and correct record of the meeting.

|

|

That the confidential

minutes of the Audit and Risk Committee meeting held on Wednesday, 10 July

2024, be confirmed as a true and correct record of the meeting.

|

6 Reports

6.1 2024-34

Long Term Plan Audit Report Update....................................................... 4

6.2 Risk

Appetite.......................................................................................................... 44

6.3 Audit

and Risk Committee Terms of Reference.................................................... 48

7 Confidential

Session

7.1 Procedural

motion to exclude the public............................................................... 55

7.2 Risk

and Audit Report............................................................................................ 55

7.3 Cybersecurity

Update............................................................................................ 55

7.4 Draft

Annual Report 2024...................................................................................... 55

7.5 Legal

Services Report........................................................................................... 56

8 CLOSING

KARAKIA

Audit and Risk

Committee

Agenda – 03 October 2024

6 Reports

6.1

2024-34 Long Term

Plan Audit Report Update

Information Only - No Decision

Required

|

Report

To:

|

Audit

and Risk Committee

|

|

Meeting

Date:

|

3

October 2024

|

|

Report

Author:

|

Matthew

McGlinchey, Financial Performance Manager; Alan Bywater, Team Leader - Community

Policy

|

|

Report

Authorisers:

|

John

Ridd, Group Manager - Service and Strategy

|

|

Report

Number:

|

RFNAU24-10-1

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 To table the

interim Audit Report on the Long-Term Plan (LTP) Consultation Document and final

Audit Report on the Long-Term Plan 2024-2034.

2. Recommendation/s

/ Ngā Tūtohunga

That the Audit and Risk

Committee

1. receives the 2024-34 Long Term Plan Audit Report Update report; and

2. notes Audit New Zealand’s feedback on the Long-Term Plan

2024-2034 process; and

3. notes that staff will organise a workshop to discuss how the Audit

and Risk Committee could best contribute to future Long-Term Plan and Annual

Plan processes.

3. Audit

Report on the LTP Consultation Document 2024-2034

3.1 On 12 April

2024, Audit New Zealand supplied its report on the audit the LTP 2024-2034

Consultation Document which is attached to this report (Attachment 1).

3.2 Audit New

Zealand made several recommendations to the Council around its findings. These

are listed below with Council’s response.

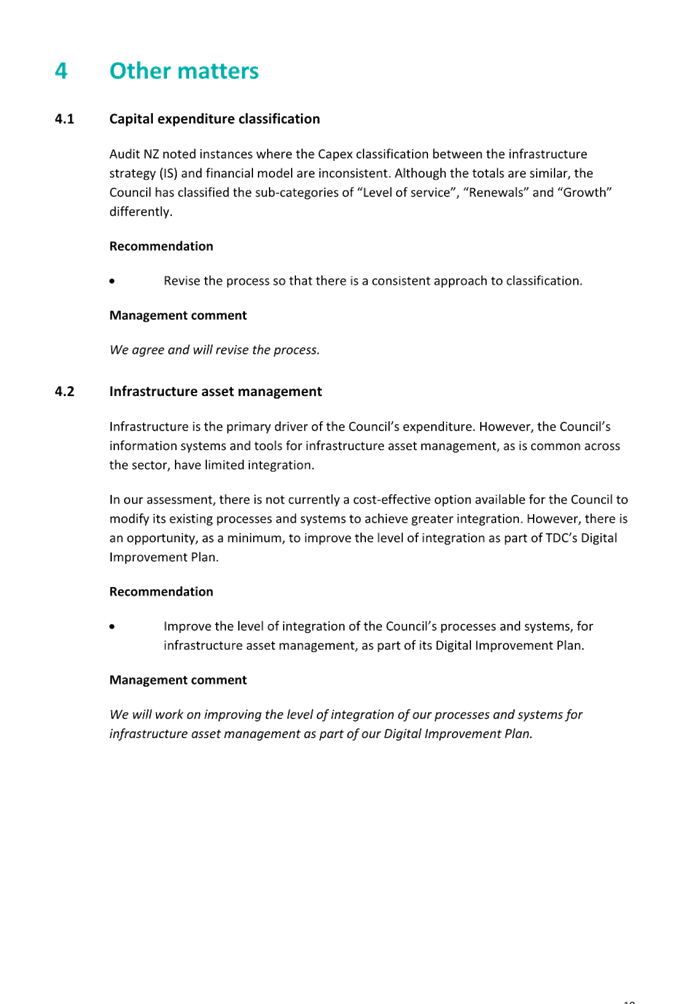

3.3 Capital expenditure

classification paragraph 4.1. Audit recommended that we revise the process

so that there is a consistent approach to classification in terms of growth,

renewal of levels of service capital projects. Council agreed to revise the

classifications going forward.

3.4 Infrastructure asset

management paragraph 4.2. Audit recommended that we improve the level of

integration of the Council’s processes and systems, for infrastructure

asset management, as part of its Digital Improvement Plan. Council agreed to

consider this.

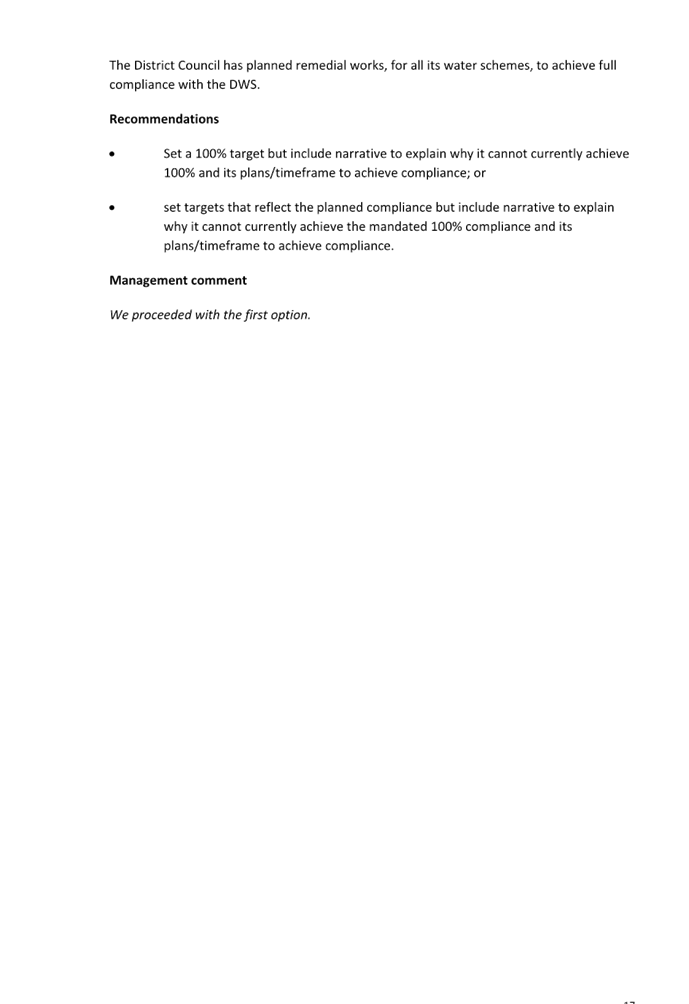

3.5 Levels of service for water

supply – paragraph 3.3.2. Audit recommended that we set a 100% target but include

narrative to explain why it cannot currently achieve 100% and its

plans/timeframe to achieve compliance; or set targets that reflect the planned

compliance but include narrative to explain why it cannot currently achieve the

mandated 100% compliance and its plans/timeframe to achieve compliance

3.6 Council will

look to set a 100% target but include narrative to explain why it cannot

currently achieve 100% and its plans/timeframe to achieve compliance over the coming LTP cycle.

3.7 Infrastructure Strategy (IS) paragraph

3.2. Audit recommended we clarify in the IS, that most overall levels of

service are unchanged and include examples of the reductions in services

planned. Council comment on this point was that statements on the key points of

focus around levels of service were included in sections for each activity

3.8 National policy Statement on

Urban Development (NPS-UD – paragraph 2.3.2. Audit New Zealand did

not make a recommendation, however the Council responded as follows to ensure

that Audit understood its position. A letter about the NPS-UD with the content

described above was sent to the Minister for the Environment on 1 July 2024. We

felt it was inappropriate to pre-empt the final form of the LTP until it was

adopted. The risk of development occurring over a longer period than expected

is disclosed on our forecasting assumptions. We have established a growth

governance board to closely monitor the level of development against our

estimates and to recommend changes to the programme of growth infrastructure

investment where necessary

4. Audit Report to Governors – Final LTP

2024-2034

4.1 The Audit Report

to Governors on the Final LTP, received in August 2024, (Attachment 2)

notes that Audit NZ issued an unmodified audit report with an emphasis of

matter over the New Zealand Transport Agency,

Waka Kotahi (NZTA) funding for roading programmes. The

emphasis of matter drew attention to the assumptions and judgements made by the

Council given the heightened level of uncertainty with this funding assistance.

4.2 We notified Audit NZ of a number of

budget changes totalling $8.3 million that we became aware of after the

consultation commenced. Audit NZ reviewed these changes and satisfied

themselves that the consequential impacts on various parts of the LTP were

clear and consistent. They determined that the conclusions reached

at the CD stage were still consistent with the conclusions reached at the final

LTP. However, the forecast opening balances for the LTP were reforecast

and consequential updates were made to the rates, revenue and expenses to address

the flow on impacts.

4.3 Audit NZ noted in the report that

the NZTA released its indicative allocations for continuous programmes on 6

June 2024. This is very late in the LTP process and we decided not to

make adjustments to the LTP. Audit NZ was satisfied that neither the

financial amount nor the consequential impact on service levels were material.

4.4 In paragraph 3.3, Audit indicated

that the Asset information and the first set of overall financials for the

Consultation Document were not delivered on time. TDC believes they were

delivered on time.

4.5 In paragraph 6.1, Audit NZ noted

that limited use was made of the knowledge and expertise of the Audit Committee

in the LTP process and Council’s deliberations. Audit NZ recommended we

review the LTP preparation process with the aim of maximising the knowledge and

expertise of the Audit Committee in the preparation and audit of the LTP.

4.6 We are conducting a review of the

overall LTP process. Part of that will involve a discussion with our

Independent Audit chair. We are also considering a workshop with the Audit and

Risk committee to better utilise the skill set it has. As always, the time

required to loop in the Audit and Risk committee is a challenge.

4.7 In August 2024, Audit NZ notified the

Council that it was commencing a process to confirm the costs of the LTP audit

process. In this letter Audit NZ indicated that the costs above the

$114,000 audit fee in the letter of engagement, it was looking to recover

$87,850 (or 77% more) for additional work carried out on the LTP. Audit

NZ specifically noted the following areas of additional work:

· Additional work auditing the impact the NZTA indicative funding

announcement.

· Reviewing two drafts plus and final version of the consultation

(compared with the two drafts anticipated) and ensuring that flow on impacts of

changes were addressed.

· Lack of alignment between the rates affordability and service levels

options in the Financial Sustainability key issue and uncertainty over the

prudence of the Financial Strategy in terms of headroom to enable funding of

future flooding events.

· Three matters in the performance framework relating to setting

realistic targets for roading, targets for the different water supplies

compliance with Drinking Water Standards and the measures and targets for

active transport.

· Additional work carried out by their asset management specialist.

· End of 2023/2024 forecast projections not being available until

after the consultation document was adopted requiring further Hot Review and

Opinion Review Committee meetings.

· Additional work on the climate change strategy development and

implementation.

· The approach to the community fundraising contributions towards the

new community facilities planned in the LTP.

· Ensuring adequate disclosures for financial prudence in the

Financial Strategy.

· Additional work on negative reserves.

4.8 Staff accept in some instances this

additional work and costs are valid. In other instances we do not agree

that there should have been additional work and/or that it was not included in

the work planned in the letter of engagement.

4.9 A process to resolve the level of

additional costs Council will pay is underway. A verbal update will be provided

at the meeting.

|

1.⇩

|

Report on

the Audit of the LTP Consultation Document 2024-2034

|

7

|

|

2.⇩

|

Draft

Governors' Audit Report - LTP stage

|

28

|

Audit and Risk

Committee

Agenda – 03 October 2024

Audit and Risk Committee Agenda – 03 October 2024

Audit and Risk Committee Agenda – 03 October 2024

6.2 Risk Appetite

Information Only - No Decision

Required

|

Report

To:

|

Audit

and Risk Committee

|

|

Meeting

Date:

|

3

October 2024

|

|

Report

Author:

|

Amy

Clarke, Risk & Assurance Advisor

|

|

Report

Authorisers:

|

Steve

Manners, Chief Operating Officer

|

|

Report

Number:

|

RFNAU24-10-3

|

1. Summary

/ Te Tuhinga Whakarāpoto

1.1 A Risk Appetite

Statement (Attachment 1) has been drafted based on information from

Councillors.

1.2 The Audit and Risk Committee is invited

to provide feedback before the Risk Appetite Statement is presented to the

Council for adoption.

2. Recommendation/s

/ Ngā Tūtohunga

That the Audit and Risk Committee

1. receives the Risk Appetite report RFNAU24-10-3; and

2. recommends to Council the adoption of the Risk Appetite Statement.

3. Risk

Appetite Statement

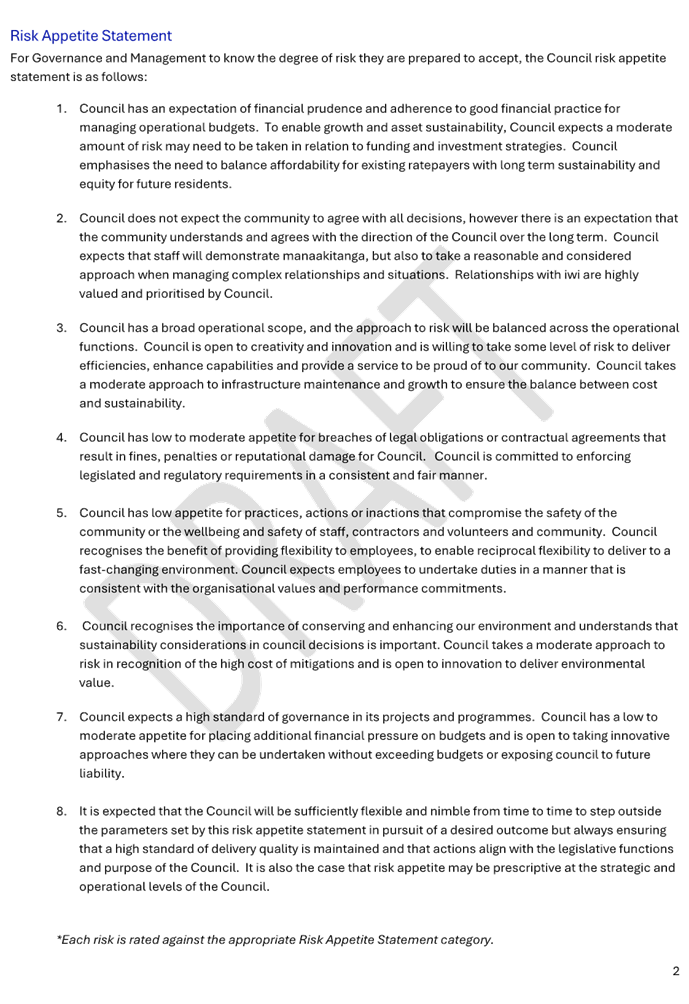

3.1 The Risk

Appetite Statement describes the amount and type of risk that Council is

willing to pursue or retain in the execution of its strategic and business

objectives.

3.2 The Risk

Appetite Statement is a guide from Council to staff. While the Risk

Appetite Statement provides a framework for staff to respond to in most

circumstances, there remains is an expectation that staff act with prudence,

good judgement and be open to pursuing opportunities outside of the risk

appetite where appropriate.

4. Developing the Risk Appetite Statement

4.1 Two workshops

were held with Councillors to develop the Risk Appetite Statement.

4.2 At the first

workshop, Councillors provided individual assessments of each risk type.

These individual assessments were consolidated into a draft risk appetite

statement.

4.3 At the second

workshop Councillors had the opportunity to discuss if the consolidation of the

risk appetite was a fair representation of the views of Council as a

whole. Feedback from this workshop has been incorporated into the draft

Risk Appetite Statement (attached).

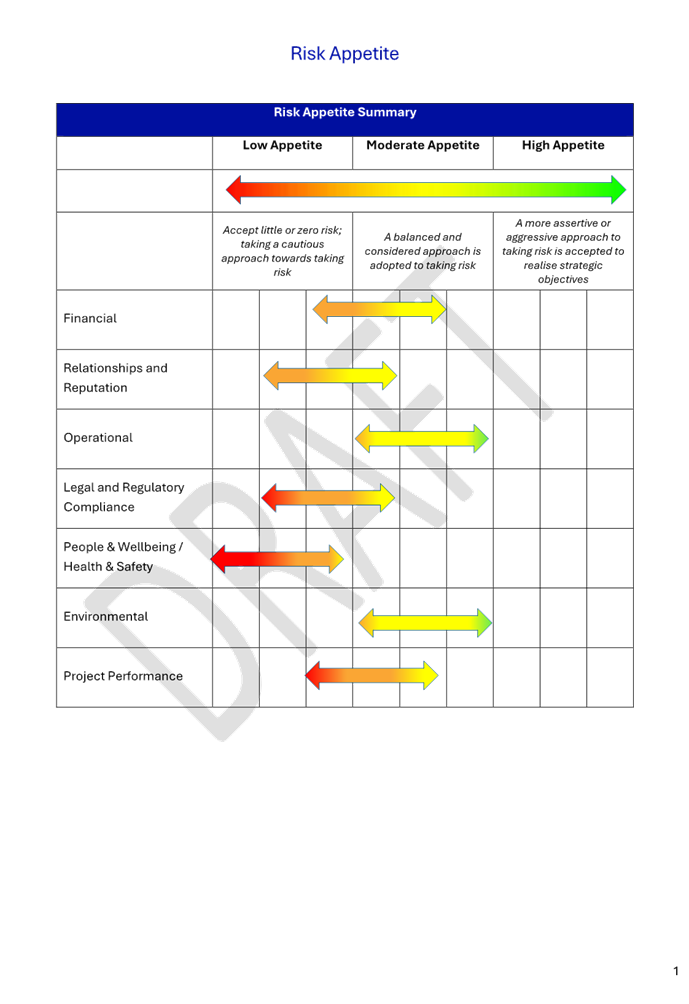

5. Risk Appetite Statement

5.1 The Risk

Appetite Statement covers the categories of risk as described in the Risk

Framework (Financial, Relationships and Reputations, Operational, Legal and

Regulatory Compliance, People & Wellbeing/ Health & Safety,

Environmental, Project Performance).

5.2 A pictorial

summary is provided as well as descriptions for each category.

|

1.⇩

|

DRAFT Risk

Appetite Statement

|

46

|

Audit and Risk

Committee

Agenda – 03 October 2024

Audit and Risk Committee Agenda – 03 October 2024

6.3 Audit and Risk Committee Terms of Reference

Information Only - No Decision

Required

|

Report

To:

|

Audit

and Risk Committee

|

|

Meeting

Date:

|

3

October 2024

|

|

Report

Author:

|

Amy

Clarke, Risk & Assurance Advisor

|

|

Report

Authorisers:

|

Steve

Manners, Chief Operating Officer

|

|

Report

Number:

|

RFNAU24-10-2

|

1. Summary

/ Te Tuhinga Whakarāpoto

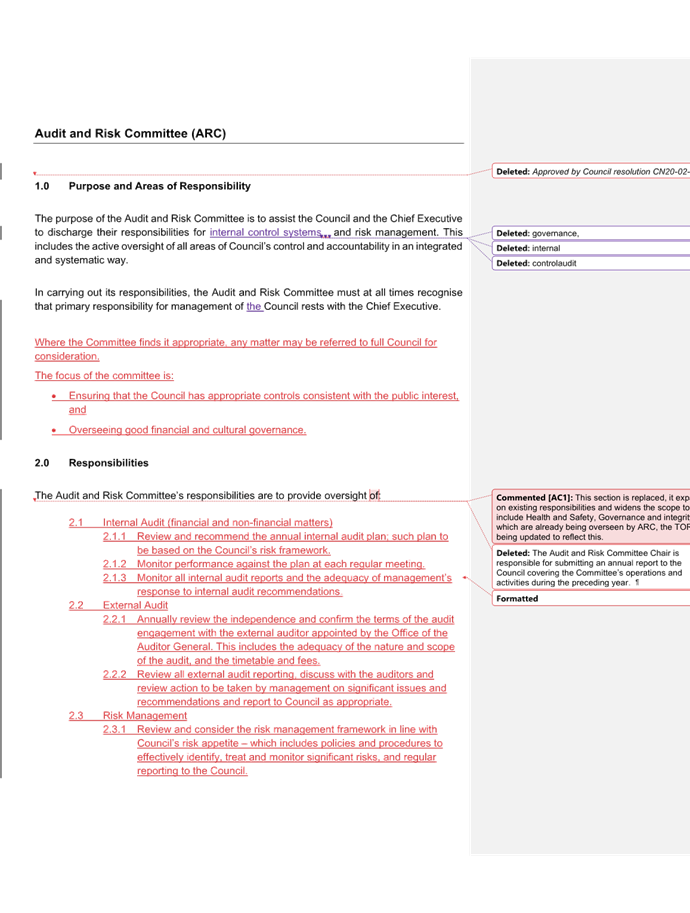

1.1 An amendment to

the Audit and Risk Committee (ARC) Terms of Reference (TOR) is proposed to

allow for continuity of membership in extraordinary circumstances.

1.2 The opportunity

has also been taken to consider the entirety of the TOR, and additional changes

are proposed to clarify the responsibilities of the committee and amend an

error in elected member numbers.

1.3 With ARC

endorsement, the TOR will be submitted to the Council for approval.

2. Recommendation/s

/ Ngā Tūtohunga

That the Audit and Risk Committee

1. receives the Audit and Risk Committee Terms of Reference report RFNAU24-10-2; and

2. recommends to Council the adoption of the revised Audit and Risk

Committee Terms of Reference.

3.1 It has been

identified that some flexibility in the membership of the committee would be

valuable to allow for more than two terms (or six years total) in extraordinary

circumstances. This would allow for elected or independent members to be

reappointed if required to provide continuity of support to Council.

Situations this might apply to include the need for a specific skill set,

significant change in the organisation (e.g. change of leadership), or a

significant event impacting Council or the region. The draft TOR (Attachment

1) includes the following:

3.1.1 “Any member of the committee, either elected or

independent, may serve no more than six years (the equivalent of two terms of

three years) on the committee. In extraordinary circumstances, Full Council may

approve an additional term for a member of an appropriate length to ensure the

committee is able to provide continuity of support to the Council.”

3.2 The opportunity has been taken to

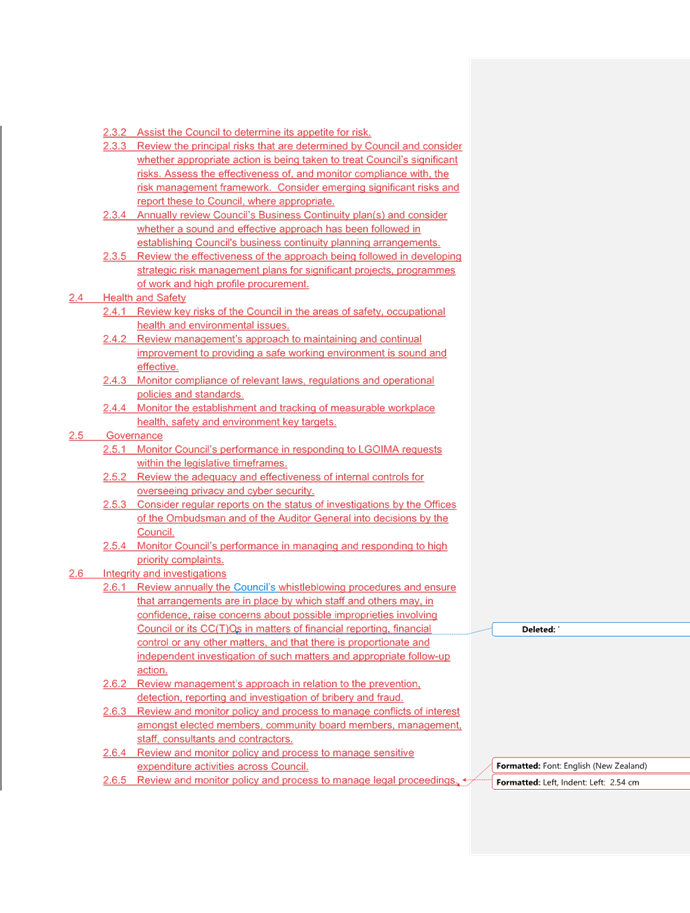

consider the entirety of the TOR and several amendments are recommended:

3.2.1 widening the scope of ARC to include Health and Safety,

Governance and Integrity. These areas are already included in principle,

but specific detail is not provided within the TOR.

3.2.2 providing more specific detail on the responsibilities

of ARC.

3.2.3 specifying what information should be included in the

Chair’s annual report to Council.

3.2.4 amending the number of elected members to reflect the

appointments.

3.3 Feedback and endorsement of the TOR (attached)

is sought from ARC prior to submission for Council approval.

|

1.⇩

|

ARC TOR

2024 DRAFT

|

50

|

Audit and Risk Committee Agenda – 03 October 2024

Audit and Risk Committee Agenda – 03 October 2024

7 CONFIDENTIAL SESSION

7.1 Procedural

motion to exclude the public

The following

motion is submitted for consideration:

That the

public be excluded from the following part(s) of the proceedings of this

meeting. The general subject of each matter to be considered while the public

is excluded, the reason for passing this resolution in relation to each matter,

and the specific grounds under section 48(1) of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution follows.

This resolution is made in reliance on section 48(1)(a) of the Local

Government Official Information and Meetings Act 1987 and the particular

interest or interests protected by section 6 or section 7 of that Act which

would be prejudiced by the holding of the whole or relevant part of the

proceedings of the meeting in public, as follows:

7.2 Risk and Audit Report

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(g) - The withholding of the

information is necessary to maintain legal professional privilege.

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

7.3 Cybersecurity Update

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

s7(2)(j) - The withholding of the

information is necessary to prevent the disclosure or use of official

information for improper gain or improper advantage.

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

7.4 Draft Annual Report 2024

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(b)(ii) - The withholding of the

information is necessary to protect information where the making available of

the information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject of the information.

In particular, financial information for

Waimea Water Ltd, and Infrastructure Holdings Ltd has not yet been made

publicly available. The attached Marsh Valuations report contains personnel

details

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

7.5 Legal Services Report

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(g) - The withholding of the

information is necessary to maintain legal professional privilege.

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|