Notice

is given that an ordinary meeting of the Tasman District Council will be held

on:

|

Date:

Time:

Meeting

Room:

Venue:

YouTube Link:

|

Thursday 7 May 2026

9.30am

Tasman Council Chamber

189 Queen Street, Richmond

Tasman District Council Meetings - YouTube

|

|

Tasman

District Council

Kaunihera

Katoa

AGENDA

|

MEMBERSHIP

|

Mayor

|

Mayor T King

|

|

|

Deputy Mayor

|

Deputy Mayor B Maru

|

|

|

Councillors

|

Councillor C Butler

|

Councillor M Kininmonth

|

|

|

Councillor J Ellis

|

Councillor K Maling

|

|

|

Councillor K Ferneyhough

|

Councillor D McNamara

|

|

|

Councillor M Greening

|

Councillor P Morgan

|

|

|

Councillor J Gully

|

Councillor T Neubauer

|

|

|

Councillor M Hume

|

Councillor T Walker

|

|

|

|

Councillor D Woods

|

(Quorum 8 members)

|

|

|

Contact Telephone: 03 543 8400

Email: tdc.governance@tasman.govt.nz

Website: www.tasman.govt.nz

|

Tasman District Council Agenda – 07 May 2026

AGENDA

1 Opening, Welcome, KARAKIA

2 Apologies

and Leave of Absence

|

Recommendation

That the apologies be accepted.

|

3 Public

Forum

Nil

4 Declarations

of Interest

5 LATE

ITEMS

6 Confirmation

of minutes

|

That the minutes of

the Tasman District Council meeting held on Thursday, 9 April 2026, be

confirmed as a true and correct record of the meeting.

|

7 Reports

7.1 Use of 79-81 Commercial Street Takaka as

the site for storage of the Anaweka Waka 4

7.2 Three Waters Maintenance Forecast Overspend

- 2025-2026............................ 17

7.3 Mayoral Update...................................................................................................... 28

8 Confidential

Session

8.1 Procedural

motion to exclude the public............................................................... 33

8.2 R26-16 International Cricket - Saxton Field

Outfield Renewal............................. 33

8.3 Iwi Representation Appointments 2025 - 2028

term............................................. 33

8.4 Cornwall Place, Tata Beach - Options.................................................................. 34

8.5 Fuel Price and Supply Impacts.............................................................................. 34

9 CLOSING

KARAKIA

Tasman District Council Agenda – 07 May 2026

7 Reports

7.1

Use of 79-81

Commercial Street Takaka as the site for storage of the Anaweka Waka

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

7

May 2026

|

|

Report

Author:

|

Leith

Townshend, General Counsel; Grant Reburn, Reserves and Facilities Manager

|

|

Report

Authorisers:

|

John

Ridd, Group Manager - Customer & Community; Leonie Rae, Chief Executive

Officer

|

|

Report

Number:

|

RCN26-05-4

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 The

purpose of this report is to provide information to the Council on the Anaweka

Waka project and seek their agreement to engage with the community on the

location and ownership of the facility being proposed to house the Anaweka

Waka.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 On

13 February 2025 the Council received a presentation from the Anaweka Waka

Working Group on the history of the Anaweka Waka and the proposal for a new

facility to accommodate the long-term storage and display of this Waka. The

feedback from the presentation from the Council was positive.

2.2 The

Working Group have previously identified the site next to the current Golden

Bay Museum (79-81 Commercial Street, Tākaka) as the preferred location for

a building to house the Waka.

2.3 Since

1990 this site location has been gazetted as Local Purpose Reserve (site for

museum). It is the opinion of the Working Group and Council staff that the

storage and display of the Anaweka Waka and other taonga is in keeping with

this purpose.

2.4 On

19 June 2025 (RCN25-06-10) the Council resolved the

following:

That the Tasman District

Council:

1. receives

the Use of 79-81 Commercial Street Tākaka

as the site for storage of the Anaweka Wakareport, 0.0; and

2. notes

that legal ownership of the Waka has not been determined by the Māori Land

Court but both claimants have jointly offered support for the approach below;

and

3. agrees

in principle, subject to future consultation, that 79-81 Commercial Street,

Tākaka is an appropriate location for the housing of the Anaweka Waka; and

4. notes

that consultation will be required under the Reserves Act and Local Government

Act to allow for any future use on this site; and

5. notes

that there are a number of options regarding ownership, operation and

governance of any facility built on the site and that these are being explored

by the Working Group before coming back to the Council for approval.

2.5 The

working group have presented to the Golden Bay Community Board on this

proposal, and Councillors have had the opportunity to view the Waka as part of

the induction process They will be attending to provide a presentation..

2.6 This

report now seeks Council approval to gather community feedback on the proposed

site of the Anaweka Waka facility.

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman District Council

1. Receives

the Use of 79-81 Commercial Street Takaka as the site for storage of the

Anaweka Waka RCN26-05-4; and

2. Agrees to engage with the community on the following

questions before the final decision is made by Council:

2.1 That 79-81 Commercial Street,

Tākaka is a suitable location for a facility to store and display the

Anaweka Waka,

2.2 Whether Council should agree to lease the land during

the construction of the facility,

2.3 Whether Council should enter into a long-term lease

for a facility and/or the ground under the facility depending on final

ownership decisions.

3. Notes that the engagement described above will meet

the requirements to consult under the Local Government Act 2002; and

4. Notes

that a Council decision on the use of the 79-81 Commercial

Street Takaka site is required to give Iwi enough certainty to

investigate and lodge the required consent applications;

5. Notes

that a decision on ultimate ownership of the Anaweka Waka storage facility has

not been made and that this decision will be made as part of the Long-Term Plan

considerations, and subject to further due diligence for all parties;

and

6. Notes that the feedback received during engagement on

the use of 79-81

Commercial Street Takaka will be

made available to Council and the working group once the enagagment period is

closed so that a decision can be made.

4.1 The Anaweka Waka was discovered on the

West Coast approximately 14 years ago and has since been undergoing a

conservation process in Golden Bay.

4.2 The Anaweka Waka is a hugely significant

find. The attached article sets out the scientific significance of this find

– An early sophisticated East Polynesian voyaging canoe discovered on

New Zealand's coast.

Left: The

waka held within the purpose-built drying facility. Right: Turtle emblem

carving.

Legal

ownership of the waka

4.3 As set out in the Protected Objects Act,

the waka (being taonga tūturu) is currently in the ownership of the Crown

and under the care of the Manatū Taonga (Ministry

of Culture and Heritage) until ownership is determined by the Māori Land

Court.

4.4 There are two claimants for the waka;

Manawhenua ki Mohua on behalf of Ngāti Rārua, Ngāti Tama and Te

Ātiawa, and Ngāti Kuia.

4.5 To settle the claim, the claimants will

need to prove they can care for and protect the integrity of the waka,

including certainty on where and how it will be stored. The claimants are all

represented within the working group and steering group and are collectively

working towards a solution.

4.6 The working group also includes

representation from the Golden Bay Museum and Tasman District Council.

4.7 Until legal ownership is determined, Manatū

Taonga will maintain interim ownership and ultimate

decision-making. However, as far as possible Manatū Taonga want to support

the aspirations of Iwi and support the current proposal. Attachment one is

a letter of support from Manatū Taonga.

4.8 Both potential claimants are involved in

the Anaweka Waka working group and are supportive of the approach to build a

new facility in Golden Bay.

Conservation

4.9 Staff from the Auckland War Memorial

Museum continue to support conservation efforts. This support has been

facilitated and funded by the Manatū Taonga. The

conservator team advise that the waka is dry, stable and being cleaned of any

final residue.

Activities of the Working Group

4.10 The focus of the Working Group is shifting towards

the design and construction of the building alongside the other decisions that

need to be made by Iwi and the Council – such as ownership of the

building and operating models.

4.11 They have also completed an RFP selecting a project

architect, Fineline Architecture, and are underway with design of the wharewaka

adjoined to the Golden Bay Museum. A pre concept design has been completed

which was previously shared with the Council.

4.12 The concept design is well developed and one of the

designs is below:

4.13 While there is still more work to do on the final

budget and design, including quantity survey, the working group has set a cap

of $5 million capital cost for the construction of the wharewaka inclusive of

the ātea space. Internal alterations required within the Golden Bay Museum

are out of scope of the wharewaka project and are being considered by the

Golden Bay Museum in conjunction with this project.

4.14 The intention is to fundraise externally to fund

this project. To date, the Department of Internal Affairs have funded the

design work through the Lotteries Environment and Heritage Fund and the working

group is preparing a funding application for stage 2 for 1 July 2026 to 30 June

2027 which will include the developed and detailed design; and building consent

application.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 Ultimately

the Council will need to make several decisions in relation to this project and

public consultation is required before those decisions can be made. These

decisions and the questions for consultation are outlined below.

The location of the facility to store

the Waka

5.2 Iwi

and the working group have previously explored several different options for

storing the waka. Their preferred site is 79-81 Commercial Street,

Tākaka.

5.3 The

reason that this site is preferred is its central location in Tākaka and

proximity to the Golden Bay Museum which creates efficiencies for the operation

of the facility and adds operational resilience to both the Golden Bay Museum

and the wharewaka.

5.4 Since 19 April 1990, this land

has been designated as a reserve meaning that it is subject to the Reserves Act

1977.

5.5 There are a number of different

‘types’ of reserve under the Reserves Act and this land has been

designated ‘Local Purpose (Site for a museum) Reserve’.

5.6 Staff view is that the storage

and display of the Waka and other taonga is consistent with this purpose.

Council previously decided in principle that the site would be a suitable

location for the waka.

5.7 There

is currently a pioneers memorial at the tip of this site, this has been there

for many years after being relocated there from another part of Tākaka. It

is anticipated that as part of the project the working group will work with the

Golden Bay Community Board to relocate the memorial. This may be within the

museum precinct or elsewhere.

5.8 There

are some large trees currently on the site which will need to be removed as

part of any development. This may need to be addressed in the resource consent

application. The removal of the trees is welcomed by the museum management team

as they create ongoing building maintenance issues for them.

5.9 The

community will be asked whether they consider this site to be suitable for a

facility to store the waka before the decision comes back to Council.

Use of land during the construction

period

5.10 During

the construction phase of this project the site will need to be closed to the

public to allow the construction company to meet their Health and Safety

obligations.

5.11 This

means that the Council will need to enter into a lease with the entity

constructing the facility and restrict public access.

5.12 During

consultation the public would be informed that notice will be given once the

Council has made its final decision. This would restrict access to the site

during the construction phase and going forward once the facility is built.

Ownership of the facility

5.13 Before

the construction begins a decision will need to be made on the ownership of the

building – i.e. whether it is owned by an Iwi entity or by Council, or

other alternatives.

5.14 This

decision will need to be made as part of the long-term plan process as taking

ownership for the building will have several ongoing operational costs for its

eventual owner. The working group considers that it is too premature to

consider this decision now, as further due diligence needs to be undertaken to

better inform all parties.

5.15 An

approval to access the land now will not predetermine or undermine an outcome

on this matter. The working group will not be able to proceed with leases or

construction until this matter is determined, which will happen in due course

when there is more confidence in the final building proposal and costs.

5.16 It

is also noted that depending on the eventual ownership model, the Council will

need to enter into either a ground lease or ground and improvement lease with

the entity managing the facility.

Consultation process

5.17 Once

approval is received staff will create consultation material onto Shape Tasman

and put an advertisement in the Golden Bay Weekly to advise people of the

proposal and let them know how to have their say. Staff will also look to

advertise on Newsline (depending on publishing deadlines).

5.18 The

Golden Bay Community Board and local Iwi representatives will also be

approached and asked to submit and publicise the on-going consultation.

5.19 Members

of the working group will also be encouraged to advertise and publish the

on-going consultation through their networks.

5.20 Depending

on engagement with the community there is an option for the consultation to be

extended to allow for a public meeting to discuss the proposal.

5.21 It

is proposed that the consultation be open for three weeks.

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

6.1 There

are minor budgetary implications for consultation which will be on Shape

Tasman, Newsline and advertised in the Golden Bay Weekly. It is anticipated

that these costs will be less than $200, not including staff time.

7.1 The options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Agree to consult with the community on

the waka project as a stand-alone consultation in the near future.

|

Community views sought on this project in

a timely manner.

|

Minor financial costs and staff time

associated with consultation (e.g. article/public notice in Golden Bay

Weekly).

|

|

2.

|

Agree to consult with the community by

including the proposal within the draft Golden Bay Ward Reserve Management

Plan (RMP), expected to be publicly notified in September 2026. The Local

Purpose Reserve land parcels where the waka is proposed to be housed will be

included within the RMP.

|

Community views on this project can be

captured as part of the wider Golden Bay Ward RMP review project.

|

Timing may not be ideal for the wharewaka

project. Under the Reserves Act, draft RMPs must be open for submissions for

two months, followed by hearings and deliberations. The final RMP will not be

adopted until February 2027 at the earliest.

The wharewaka project may be

‘lost’ among the range of other proposals being consulted on for

the draft RMP project.

|

|

3.

|

Decline to consult and take no further

steps to support the project.

|

No further cost or staff time will be

spent on this project.

|

Detrimental to the Council’s

relationship with its Iwi partners.

The wharewaka project will no longer be

feasible at this site and there will be considerable sunk costs.

The public may not have the opportunity

to see an important cultural artifact.

|

|

4.

|

Seek more information from the working

group.

|

Further information can be provided that

may better inform Council decision making.

|

Delays consultation and additional staff

time associated with producing a further report.

There may be risks to the timing of

funding tranches for the working group.

|

|

5.

|

Decline to consult and make the decision

on the use of site.

|

No consultation costs.

Certainty for the working group on the

way forward.

|

Risks community disengagement and

challenge if not consulted on.

|

7.2 Option one

is recommended.

8.1 Under the Local Government Act 2002 the

Council is required to consult or engage with the Community when making

decisions. The level of consultation required is set out in Council’s

significance and engagement policy. In this case the significance is considered

to be medium, so consultation is required under the Local Government Act 2002.

8.2 The Council is the administering body of

this site under the Reserves Act 1977. Under section 40 of the Reserves Act the

Council is charged with ensuring the use, enjoyment, development, maintenance,

protection, and preservation of the reserve for the purpose for which it is

classified. In this case the reserve has been classified local purpose (site of

a museum).

8.3 Under section 61 of the Reserves Act the

Council may do such things it considers necessary or desirable for the proper

and beneficial management, administration, and control of the reserve and for

the use of the reserve for the purpose specified in its classification.

8.4 Council may also lease the local purpose

reserve to any body or society under the following terms:

8.4.1 the lease shall be for a term not exceeding 33 years,

with or without a right of renewal, perpetual or otherwise; and

8.4.2 the lease shall include a condition that the land leased

shall be used solely for such purposes as are specified in the lease.

8.5 Council

staff’s view is that the use and lease of this site is consistent with

the purpose of the Reserves Act.

9. Iwi

Engagement / Whakawhitiwhiti ā-Hapori Māori

9.1 Iwi are fundamental to this project and

have been working with Council staff since its inception. Included in Attachment

two is a letter of support from the Iwi claimants.

9.2 Wider Iwi engagement will be sought

through consultation.

10. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

10.1 This is a decision to consult on a number of

matters. While this decision is of low significance the ultimate decision of

Council is likely to be high.

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Low

|

Decision to consult.

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Low

|

Decision to consult.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Low

|

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

No

|

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

No

|

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

No

|

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

No

|

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

No

|

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

No

|

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

No

|

|

11. Communication

/ Whakawhitiwhiti Kōrero

11.1 The

Anaweka Waka working group have engaged with the Golden Bay Community Board and

elected members have had an opportunity to view the waka.

11.2 The

next step will be wider consultation on Shape Tasman and, depending on the

level of interest, some public meetings could be held. Notification will also

be put in Newsline and potentially the local paper.

12.1 This

is a decision to consult so there are limited risks associated with this

decision. Once community feedback has been received a further paper will be

provided outlining any risks of the final decision.

13. Conclusion

/ Kupu Whakatepe

13.1 The

Anaweka Waka is a hugely significant cultural taonga that has particular

significance to Golden Bay and the local Iwi. This decision is the first step

to finding a permanent location to house and display the waka in Tasman.

14. Next

Steps and Timeline / Ngā Mahi Whai Ake

14.1 Consultation

materials will be put on Shape Tasman.

|

1.⇩

|

Attachment

one Letter of support from Manatū Taonga

|

14

|

|

2.⇩

|

Attachment

two - Letter of support from Anaweka Waka Steering Group

|

15

|

Tasman District Council Agenda – 07 May 2026

7.2 Three Waters Maintenance Forecast Overspend -

2025-2026

Decision Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

7

May 2026

|

|

Report

Author:

|

Mike

Schruer, Waters and Wastes Manager

|

|

Report

Authorisers:

|

Richard

Kirby, Group Manager - Three Waters

|

|

Report

Number:

|

RCN26-05-2

|

1. Purpose

of the Report / Te Take mō te Pūrongo

1.1 To

gain approval for unbudgeted forecast maintenance expenditure in the 2025/26

financial year which is forecast to be $75,000 for stormwater, $714,000 for

Wastewater and $1,065,000 for Water Supply.

2. Summary

/ Te Tuhinga Whakarāpoto

2.1 For

this financial year 2025/2026, the Three Waters Group forecast maintenance

over-expenditure of $75,000 for stormwater, $714,000 for Wastewater and

$1,065,000 for Water Supply. An increase in reactive maintenance costs is

the main driver of the forecasted expenditure overspend.

2.2 Funds

collected via targeted rates and/or fees and charges for one activity cannot be

used in another activity. The only exception is that Council can utilise

funding from the General Rate and the Uniform Annual General Charge (UAGC) for

any activity.

2.3 A process has been undertaken to find maintenance cost savings,

however, there is little room to reduce Three Waters maintenance costs without

impacting on compliance with quality assurance rules and resource consents.

This increased cost of maintenance has been incorporated into the draft Annual

Plan 2026/2027 process. At financial year end there may be other areas

of TDC that could help fund the overspend in this area.

2.4 Systematic

failure of a pipe in Fairfax St, Murchison has required immediate renewal to

retain the water supply service, reduce breakage and ongoing reactive repairs

costs. Funding has been transferred from the Waimea Plains Project for

2025/2026 as it won’t be spent entirely. It is intended that once

the Waimea Plains Project is scoped that should the funding need to be

increased it will be considered at that time.

3. Recommendation/s

/ Ngā Tūtohunga

That the Tasman

District Council

1. receives

the Three Waters Maintenance Forecast Overspend - 2025-2026 report, RCN26-05-2;

and

2. notes the forecast unbudgeted maintenance expenditure

in the following activities:

2.1 Stormwater – up to $75,000

2.2 Wastewater – up to $714,000

2.3 Water supply – up to $1,065,000; and

3. approves

the unbudgeted maintenance over-expenditure of up to:

3.1 $75,000

for stormwater,

3.2 $714,000

for Wastewater,

3.3 $1,065,000

for Water Supply; and

4. notes

that once the end of year accounts for each of the Three Waters activities are

finalised, that Council decide how the deficits, if any, are funded.

4.1 During the development of the 2025/2026

Annual Plan, the budgets for Three Waters Operations and Maintenance were

reduced by Council in the hope that reactive maintenance would reduce compared

to previous years. These reductions were made in the wider context of

reducing the overall increase in rate revenue for 2025/2026. Some routine

maintenance budgets were also reduced.

4.2 However, Council is now three quarters

of the way through the financial year and the reactive maintenance in the water

supply and wastewater activities is continuing to follow the trends of previous

years. Staff are forecasting unbudgeted overspend simply repairing,

maintaining or clearing blockages in our reticulation networks or treatment

plants in addition to the costs of responding to the July 2025 storm event.

4.3 A report on the Three Waters Operations

and Maintenance forecast was presented to the Council on 11 February 2026

advising of the likely unbudgeted over expenditure.

4.4 Much

of the reactive maintenance expenditure is a result of insufficient pipe

renewals undertaken over previous years and an ageing pipe network. The

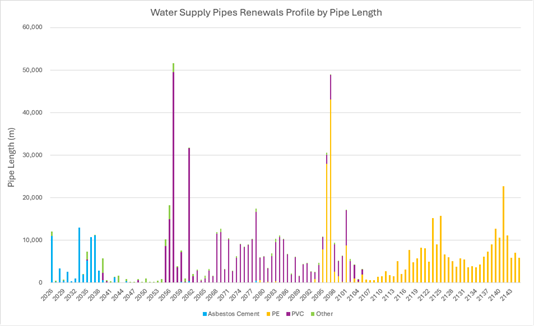

graphs Figures 1 and 2 indicate the level of deferred renewals in

2026 and looking forward there is a bow wave of renewals expenditure facing the

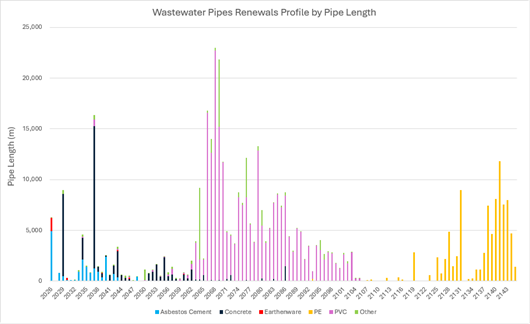

Council. These are mostly asbestos cement, concrete pipes, and a limited

amount of “Blue Brute” PVC and earthenware.

4.5 The inflow/infiltration budgets have been reduced in recent

years. The intention of these budgets was to identify locations of inflow

from private properties and low cross connections and infiltration through

structural defects allowing groundwater or stormwater into the wastewater

network. Failures do occur unexpectedly and come at significant cost.

This is due to out-of-hours work, disruption to routine work, consequential

damage and inconvenience to customers. Identification and scheduled

repair of these defects are considered cost effective as they minimise further

deterioration, reducing the risk of more significant failures.

Figure

1: Pipe Renewal Profile Graphs for Water Supply

(based on age)

Figure 2: Pipe Renewal Profile Graphs

for Wastewater (based on age)

4.6 The wastewater and stormwater reactive

maintenance is also strongly influenced by weather events, which are difficult

to predict. The two weather events in June/July 2025 are such an example.

4.7 The Total Outturn Cost (TOC) agreed with

the contractor is primarily based on meeting the Council’s levels of

service requirements and its compliance obligations. The TOCs related to

routine operations are slightly higher than budget but not as significant as

the reactive maintenance TOCs.

4.8 If overspends are expected to occur and

there is no offsetting underspend, then staff are required to obtain approval

from Council for unbudgeted expenditure. Noting that this approval is

required prior to the overspend occurring.

4.9 Staff expect the overspend of existing

annual budgets to start in late April 2026. Some reactive maintenance budgets

have already exceeded the budgets set for particular cost centres, such as

wastewater pump stations and Low Pressure Pump Station systems (LPPS) and water

supply reticulation, treatment plant and pump stations.

4.10 The

operations and maintenance forecast for each of the Three Waters compared to

the TOC and the budgets in the Annual Plan 2025/2026 are shown in Table 1 below.

The “other” category is for works undertaken by contractors other

than the Three Water O&M contractor and therefore does not have a TOC

budget. Much of this “other” work has been done by other

contractors also doing reactive maintenance work due to the main contractor not

having the resources due to the high level of reactive maintenance they have

been required to undertake.

4.11 The

detail related to specific over-expenditure is discussed further in section 5

below.

Table 1: Three Waters Maintenance Expenditure

Forecast

|

Activity

|

AP 2025/26

O&M

Budget

|

TOC

2025/26

|

Forecast

2025/26

|

Budget

less Forecast

|

|

Water Supply –

routine

|

$2,162,000

|

$2,216,000

|

$1,913,000

|

$250,000

|

|

Water Supply –

reactive

|

$2,157,000

|

$3,415,000

|

$3,299,000

|

-$1,142,000

|

|

Water Supply - other

|

$275,000

|

|

$448,000

|

-$173,000

|

|

Total Water

Supply

|

|

|

|

-$ 1.065,000

|

|

Wastewater –

routine

|

$1,311,000

|

$1,445,000

|

$ 1,077,000

|

$234,000

|

|

Wastewater –

reactive

|

$919,000

|

$1,147000

|

$ 1,778,000

|

-$859,000

|

|

Wastewater - other

|

$36,000

|

|

$125,000

|

-$89,000

|

|

Total

Wastewater

|

|

|

|

-$ 714,000

|

|

Stormwater –

routine

|

$285,000

|

$330,000

|

$346,000

|

-$61,000

|

|

Stormwater - reactive

|

$226,000

|

$222,000

|

$123,000

|

$102,000

|

|

Stormwater - other

|

$52,000

|

|

$168,000

|

-$116,000

|

|

Total

Stormwater

|

|

|

|

-$ 75,000

|

|

Totals

|

$7,423,000

|

|

$9,277,000

|

-$1,854,000

|

4.12 Staff have made every effort to try and mitigate

the forecast overspend. A process has been undertaken to review levels of

service and find maintenance cost savings. However, there is little room to

reduce Three Waters maintenance costs without impacting on compliance with

water quality assurance rules and conditions of resource consents.

4.13 This increased cost of maintenance has been

incorporated into the budgets in draft Annual Plan 2026/2027 and will be

further reviewed and incorporated in the budgets in the Water Services Strategy

2027/2037.

4.14 Despite

these measures, staff still expect there to be a deficit compared to what the

Long-Term Plan (LTP) predicted for 30 June 2026.

4.15 If

we combined all the revenue and all the expenditure across the three waters

then the overall impact is a net forecast deficit of circa $153,000.

5. Analysis

and Advice / Tātaritanga me ngā tohutohu

5.1 The next part of this report explains what the high-level drivers

are for the overspend at the account level.

5.2 We have excluded the rising cost of fuel and consequential cost

increases from this report as there is so much uncertainty. However,

based on current use, for every $1.00/litre rise in the price of diesel would

result in an additional cost for this financial year 2025/2026 to be around

$30,000 across all three waters.

Stormwater - forecast maintenance

deficit of $75,000

5.3 Although staff forecast a deficit in the

stormwater maintenance costs, this is offset by an underspend in the stormwater

operating expenditure. The operating expenditure is tracking to be

around $99,000 below budget. This is due to lower than budgeted spending

in other operational areas, largely driven by delays in modelling and the

development of catchment management plans.

5.4 Most routine

maintenance and other costs relate to storm clean up and vegetation maintenance

of waterways – with additional focus, they are trending lower than last

year, but still above budget. Reactive maintenance at present remains

below budget, although a significant rainfall event between now and the end of

the year could adversely impact this.

Wastewater - forecast maintenance

deficit of $714,000

5.5 The Wastewater activity maintenance

forecast over-expenditure is primarily due to the increased reactive

maintenance and storm response that has occurred. $236,000 of this is due

to Council’s share of the Nelson Regional Sewerage Business Unit

operational costs and has been included in the event rate that is proposed in

the Annual Plan 2026/2027.

5.6 There have been some cost savings in the

routine maintenance from efficiencies and streamlining of work. Most of

the savings were due to the respective resources being diverted to respond to

the July 2025 storm event. This diverted them away from being able to

carry out the programmed routine operational tasks.

5.7 Under the contract Council is only

funding one wastewater team. This team covers both routine and reactive

maintenance. The staffing capacity is based on having sufficient capacity

to carry out the routine maintenance whilst having some capacity for reactive

maintenance. However, despite this, the reactive maintenance was far

greater than anticipated. The reactive maintenance budget for the Total Outturn

Cost (TOC) had been based on the actual cost trends incurred from previous

years.

5.8 The reduction in routine maintenance

includes frequency or level of cleaning of some assets, such as air valves and

wet wells; detail of checks moving to more visual rather than full strip

down. None of these compromise the level of service nor breach compliance

requirements, but they are short-cuts in maintenance that will ultimately

require attention in the future.

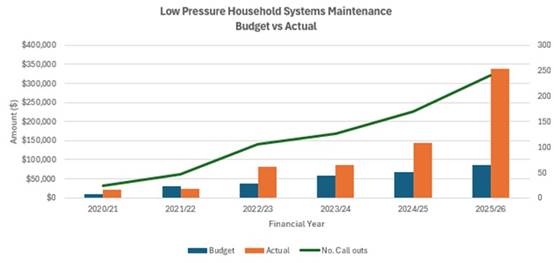

5.9 There has been an upward trend in the

number of low pressure pumpstation callouts as the number of installations have

increased over the years (refer Figure 3 below).

Figure 3: Low pressure pump

systems maintenance

5.10 For the larger wastewater pumpstations, there have

been several reasonably high-cost reactive fixes so far this year. Seven

responses have incurred an overall cost of $113,000. These responses included

replacing carbon for odour control, generator faults, damaged pumps and

replacement of damaged impellors, variable speed drives and biofilter fans.

Water Supply – forecast

maintenance deficit of $1,065,000

5.11 Higher reactive maintenance costs have been

incurred throughout the year. Around 93% of the forecast maintenance

expenditure is primarily because of the increased level of reactive

maintenance. To date, 82% of the reactive maintenance has been spent on

water reticulation.

5.12 However, it should be noted that as at 31 March

2026 the operating revenue for Water Supply is circa $1.3 million above

budgeted revenue. If this trend continues for the last three months of

the year, revenue could be $1.6 million above budget. That being the case

then this would cover the additional reactive maintenance expenditure, and

overall deficit would be covered.

5.13 The routine maintenance budget is underspent

primarily because some planned routine activities were assessed as not required

based on current asset condition. The most significant variance relates

to the Motueka Water Treatment Plant routine maintenance, with an estimated

saving of approximately $70,000. This was due to cartridge filters not

being required as expected. This is because the new product that was

trialled has performed better than anticipated. The remaining underspend reflects smaller savings across multiple

schemes, where works were either deemed unnecessary following inspection or

deferred to the next inspection cycle.

5.14 The reactive maintenance budget for the TOC is

based on the actual cost trends from previous years.

5.15 Ageing infrastructure, because of deferred pipe

renewals over the years (refer Figure 1), has led to an increased number

of pipe failures and water outages and consequent high levels of reactive

maintenance. Most of the reactive maintenance costs are related to pipe

failures.

Water Supply – Renewal Budget for

2026/27

5.16 Frequent failures over recent months in the Fairfax

Street water main, Murchison, meant that its renewal became a priority.

This water main was renewed. The ‘urban water account reticulation

renewals’ budget for 2025/2026 had already been spent on pipe

renewals. So, funding for the Fairfax Street water main renewal was

funded from the Waimea Plains capital project budget. This budget was

considered not likely to be fully spent by 30 June 2026 so was utilised to fund

this renewal.

5.17 Once the detailed scope for the various

sub-projects within the Waimea Plains Project has been completed, we can then

determine whether the remaining funding is still sufficient. If it is not

sufficient, either the scope will be revised to meet budget, or additional

funding will be requested of Council.

5.18 Council is currently up to 25-30 years behind where

it should be with our renewals programme and this is starting to have a

negative effect (increased costs) on our maintenance expenditure in our ongoing

aim to maintain our levels of service.

6. Financial

or Budgetary Implications / Ngā Ritenga ā-Pūtea

6.1 The maintenance expenditure is exceeding

approved budgets for all three water activities. At this stage staff

forecast maintenance expenditure at 30 June 2026 to exceed budget by up to

$75,000 for stormwater, up to $1,065,000 for Water Supply and up to

$714,000 for Wastewater.

6.2 In the interim, staff need Council

approval to spend overspend the current budgets to continue to undertake the

necessary reactive maintenance. It is intended that the impact of the

increase in unbudgeted maintenance expenditure be presented to Council at year

end once all the account balances for the year have been confirmed.

6.3 If there are deficits at year

end, Council could decide to implement what it decided last year which was to

fund any deficits over future years. It could also decide to increase

maintenance budgets in the Water Services Strategy to reduce the risk of

over-expenditure in future years.

6.4 At financial year end there may

be other areas of Council that could help fund the overspend in this area, but

Council will deliberate and make that decision after year end.

7.1 The options are outlined in the

following table:

|

Option

|

Advantage

|

Disadvantage

|

|

1.

|

Approve funding the ongoing unbudgeted

maintenance expenditure and once the end of year financials are completed

decide on how any overall account deficits should be funded.

|

Unbudgeted forecast maintenance

expenditure is approved until 30 June 2026.

Council will continue to deliver its

services to the customers and continue to comply with statutory requirements

and consent conditions.

|

This puts more pressure on future

maintenance budgets which may need to be increased to accommodate the

additional costs of maintenance.

|

|

2.

|

Decline to approve funding the forecast

maintenance expenditure in each of the Three Waters Activities. .

|

There are no advantages with this option.

.

|

This approach is not a realistic option

as Council cannot immediately cease maintenance to its essential services

without potential disruption to consumers and the risk of not meeting its

compliance requirements. This is not a practical option as staff do not

have delegation to spend beyond the approved budgets. At this stage of

the financial year, it would be impossible not to overspend whilst still

providing the required levels of service and still meeting ongoing compliance

requirements.

|

7.2 Option 1 is

recommended.

8.1 The Council has set budgets in the

Annual Plan 2025/2026, and this report highlights that due to the increased

reactive maintenance and the increased costs associated with the July 2025

event, those budgets will be exceeded.

8.2 At year’s end the Council will

need to consider the end of year balances for each of the Three Waters accounts

and determine then how they will be funded should that be required.

8.3 Staff cannot exceed the approved budgets

and need the assurance that funding for ongoing expenditure above current

budgets are approved.

8.4 This report ensures that the unbudgeted

maintenance expenditure is appropriately authorised, and funding approved.

9. Significance

and Engagement / Hiranga me te Whakawhitiwhiti ā-Hapori Whānui

9.1 Staff have assessed the significance of

most of the decisions proposed in this report. The significance of the combined

set of changes including the authorisation of additional unbudgeted expenditure

is considered to be medium.

9.2 No

formal engagement is proposed as the elected members can rely on their

knowledge of the views and preferences of their communities in making a

decision.

|

|

Issue

|

Level of

Significance

|

Explanation of

Assessment

|

|

1.

|

Is there a high level

of public interest, or is decision likely to be controversial?

|

Medium

|

Generally low but

some members of the community with a particular interest in Council finances

will have a higher interest.

|

|

2.

|

Are there impacts on

the social, economic, environmental or cultural aspects of well-being of the

community in the present or future?

|

Medium

|

The Annual Plan for

2026/27 and the following financial years will increase rates to recover the

rates overspend and additional interest payments.

|

|

3.

|

Is there a

significant impact arising from duration of the effects from the decision?

|

Low

|

The Annual Plan for

2026/27 and the following four financial years will increase rates to recover

the rates overspend and additional interest payments.

|

|

4.

|

Does the decision

relate to a strategic asset? (refer Significance and Engagement Policy for

list of strategic assets)

|

Low

|

|

|

5.

|

Does the decision

create a substantial change in the level of service provided by Council?

|

Low

|

|

|

6.

|

Does the proposal,

activity or decision substantially affect debt, rates or Council finances in

any one year or more of the LTP?

|

Medium

|

In the context of the

whole funding envelope for the Three Water activities, the impacts of

repaying the deficit over the following years will have a minor adverse

impact on future fees and charges for the three water activities.

|

|

7.

|

Does the decision

involve the sale of a substantial proportion or controlling interest in a CCO

or CCTO?

|

No

|

|

|

8.

|

Does the

proposal or decision involve entry into a private sector partnership or

contract to carry out the deliver on any Council group of activities?

|

No

|

|

|

9.

|

Does the proposal or

decision involve Council exiting from or entering into a group of

activities?

|

No

|

|

|

10.

|

Does the proposal

require particular consideration of the obligations of Te Mana O Te Wai

(TMOTW) relating to freshwater or particular consideration of current

legislation relating to water supply, wastewater and stormwater

infrastructure and services?

|

No

|

|

10. Communication

/ Whakawhitiwhiti Kōrero

10.1 The Council anticipates communicating this decision

to the community.

11.1 The key risk is that if approval to spend spending

unbudgeted maintenance expenditure is not given, there will be disruptions to

services and potentially major disruptions for longer periods of time until at

least more funding comes available in the Annual Plan 2026/2027 is approved.

11.2 This report has included comments on some routine

maintenance that have been deferred to reduce expenditure. This carries a

risk where the consequences of deferred maintenance may result in much greater

expenditure in the future to restore services. In effect we should still

undertake routine maintenance as “a stitch in time saves

nine”! If Council approves committing unbudgeted maintenance

expenditure, then we will include routine maintenance and no longer defer it.

12. Climate

Change Considerations / Whakaaro

Whakaaweawe Āhuarangi

12.1 The overall impact, if any, on climate resilience

and adaptation is likely to be minor.

13. Alignment

with Policy and Strategic Plans / Te Hangai ki ngā aupapa Here me ngā

Mahere Rautaki Tūraru

13.1 The Council is attempting to deliver on its vision Thriving

and Resilient Tasman Communities and the strategic priorities in the LTP

2024-2034. This approval will ensure it is very transparent around

approving over-expenditure and remain aligned with its Strategic Plans.

14. Conclusion

/ Kupu Whakatepe

14.1 The approved budgets in the Annual Plan 2025/2026

are insufficient to cover the increased costs of undertaking the maintenance

within each of the Three Waters activities. This report requests approval

to fund the forecast unbudgeted maintenance expenditure so that Council

continues delivering the Three Waters services by undertaking the necessary

level of maintenance through to the end of the financial year.

15. Next

Steps and Timeline / Ngā Mahi Whai Ake

15.1 To continue undertaking the necessary and routine

maintenance within each of the Three Waters activities through to the end of

the financial year June 2026.

Nil

7.3 Mayoral Update

Information Only - No Decision

Required

|

Report

To:

|

Tasman

District Council

|

|

Meeting

Date:

|

7

May 2026

|

|

Report

Author:

|

Tim

King, Mayor

|

|

Report

Number:

|

RCN26-05-7

|

1.1 The Middle East conflict remains

front of mind, the Chief Executive, Executive leadership team and Civil Defence

Emergency Management team are continuing to meet weekly to ensure readiness for

any potential business disruption.

1.1 The

Annual Plan consultation closed on Sunday with a strong level of engagement

already evident across the district. A significant number of submissions have

been received to date, alongside a wide range of conversations taking place

with community members.

1.2 This

engagement reflects the community’s interest in the Council’s

direction and priorities and provides valuable feedback to help inform

decision-making.

2. Recommendation/s

/ Ngā Tūtohunga

That the Tasman District Council

1. receives the Mayoral Update report RCN26-05-7.

3.1 Deputy

Mayor Maru stepped in for me at the opening for Calwell, Port Nelson’s

marine haul out and maintenance facility. This new facility represents an

important investment in regional infrastructure. While it strengthens Port

Nelson’s role as a key marine and economic hub, its benefits extend well

beyond the city boundary. Improved marine haul-out facilities will support

Tasman’s economy and help create employment and economic

resilience across both districts. This will also support and attract highly

skilled marine engineers within the Nelson-Tasman region.

3.2 Infrastructure

New Zealand held an event at the Trafalgar Centre, which I attended. The focus

was on regional resilience, with discussion centred on how resilience is

defined and maintained while recovery efforts are still in progress.

3.3 Motueka

councillors held a well-attended community drop-in event last Friday, with good

engagement and a genuine willingness from attendees to share their ideas. Feedback included requests for more rubbish bins and improved

library sound quality. There was positive support for the Motueka swimming

pool, concerns about additional liquor stores and vehicle hooning, and a

suggestion for covered seating in the CBD.

3.4 Representatives

of the local Marine Farming Association met with me on 17 April 2026 to provide

a sector update.

3.5 The latest Tim Time segment with Fresh FM, covered topics from the

recent issue of Newsline.

3.6 ANZAC

Day ceremonies were held across the Tasman District last Saturday, with strong

community participation and representation from elected members. I attended the

Lake Rotoiti service. Each service was conducted with dignity and respect,

incorporating traditional elements such as the laying of wreaths, the Last

Post, and moments of silence. Community groups, veterans, schools, and

residents all contributed to the success and atmosphere of the events.

Councillor Neubauer laying a wreath at the Brightwater

ceremony

3.7 A

learning exercise was held over two days at Civil Defence on 29 and 30 April

2026. I supported the exercise on the first day and would like to acknowledge

and thank the Emergency Management staff and staff of the Council for their

time and contribution to strengthening preparedness and response capability

within the region.

3.8 On

my way to the recent citizenship ceremony, I happened upon an ANZAC event at

Memorial Park on Cambridge Street in Richmond, where Richmond School was

performing songs and sharing stories. Following the performance, it was

heartening to see students and veterans mingling and talking together,

including conversations about medals and service, creating a meaningful

intergenerational connection.

3.9 Another

successful Citizenship Ceremony was held last Wednesday, where we proudly

welcomed 52 new citizens to the district. These new citizens represented more

than 15 different countries, reflecting the diversity and vibrancy of our

community.

3.10 Chief

Executive, Leonie Rae, Councillor Neubauer and I attended an event with Hon

Chris Hipkins. This was a useful opportunity to discuss current issues,

understand broader national perspectives, and strengthen connections between

local government, central government, and the business sector.

Nil

Tasman District Council Agenda – 07 May 2026

8 CONFIDENTIAL SESSION

8.1 Procedural

motion to exclude the public

The following

motion is submitted for consideration:

That the

public be excluded from the following part(s) of the proceedings of this

meeting. The general subject of each matter to be considered while the public

is excluded, the reason for passing this resolution in relation to each matter,

and the specific grounds under section 48(1) of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution follows.

This resolution is made in reliance on section 48(1)(a) of the Local

Government Official Information and Meetings Act 1987 and the particular

interest or interests protected by section 6 or section 7 of that Act which

would be prejudiced by the holding of the whole or relevant part of the

proceedings of the meeting in public, as follows:

8.2 R26-16 International Cricket - Saxton Field

Outfield Renewal

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(b)(ii) - The withholding of the

information is necessary to protect information where the making available of

the information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject of the information.

s7(2)(c)(ii) - The withholding of the

information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to damage the public interest.

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

8.3 Iwi

Representation Appointments 2025 - 2028 term

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(a) - The withholding of the

information is necessary to protect the privacy of natural persons, including

that of a deceased person.

The information contains personal details

about individuals considered for appointment as iwi representatives,

including their identities, background information, and evaluative material.

The decision will be made publicly available once the appointment process is

complete

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

8.4 29 Cornwall Place, Tata Beach - Disposal

Options

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(h) - The withholding of the

information is necessary to enable the local authority to carry out, without

prejudice or disadvantage, commercial activities.

s7(2)(i) - The withholding of the

information is necessary to enable the local authority to carry on, without

prejudice or disadvantage, negotiations (including commercial and industrial

negotiations).

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

8.5 Fuel Price and Supply Impacts

|

Reason for passing this resolution in

relation to each matter

|

Particular interest(s) protected (where

applicable)

|

Ground(s) under section 48(1) for the

passing of this resolution

|

|

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|

s7(2)(b)(ii) - The withholding of the

information is necessary to protect information where the making available of

the information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject of the information.

s7(2)(i) - The withholding of the

information is necessary to enable the local authority to carry on, without

prejudice or disadvantage, negotiations (including commercial and industrial

negotiations).

|

s48(1)(a)

The public conduct of the part of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding exists under section 7.

|